Markets

Need Many years of Passive Revenue? 3 Shares to Purchase Proper Now

Monetary companies are an enormous a part of America’s financial system, value practically $2 trillion. It is an important place to search for long-term investments. In any case, America would not be the financial marvel it’s right this moment with out its strong and progressive monetary system.

These searching for dividends do not need to sacrifice upside potential for passive earnings. You may have your cake and eat it, too.

Listed below are three fantastic companies with a monitor report of market-beating funding returns that can pay you to carry them for many years.

1. Visa

Cost playing cards are a lifestyle within the U.S. Based on , 9 in 10 Individuals have no less than one debit card, and eight have no less than one bank card. Take your fee playing cards out and look within the nook — you may most likely see Visa‘s (NYSE: V) brand. Visa is the main fee community in each the U.S. and worldwide. The corporate’s enterprise mannequin is genius; it will get a small price every time somebody pays with a Visa-branded fee card or digital pockets.

Individuals worldwide are steadily transferring away from money, which has fueled Visa’s decades-long progress story. Final yr, the corporate generated $32.7 billion in income on $12.3 trillion in fee quantity. This story is not over, both. Researchers count on trillions of {dollars} in fee quantity progress over the approaching years as cashless funds develop, particularly in rising markets. That is simply high quality for Visa, which has a worldwide footprint.

Visa’s dividend packs a mighty punch. It has grown by a mean of 18% for the previous decade and is on a 16-year progress streak that began at its IPO. The expansion wanted to maintain such fast dividend progress has additionally produced exceptional funding returns. Shares have handily overwhelmed the S&P 500 over Visa’s lifetime. Development tailwinds for cashless funds and a modest 22% ought to make Visa a bona fide wealth-builder for years.

2. Jack Henry & Associates

A small group of megabanks guidelines the monetary sector, however over 4,000 small and medium-sized banks and credit score unions play a vital function in America’s financial panorama. Jack Henry & Associates (NASDAQ: JKHY) supplies varied fee processing companies, software program, and know-how options to those banks, which usually haven’t got the sources to construct aggressive know-how in-house. Jack Henry & Associates’ mission-critical merchandise create sticky income and a aggressive moat.

The corporate’s dividend progress report is a testomony to its sturdiness. Jack Henry & Associates has paid and raised its dividend for 34 consecutive years, which means it raised it by COVID-19 and the Nice Recession in 2008-2009, arguably essentially the most difficult banking atmosphere because the Nineteen Thirties. Prudent administration deserves some credit score for that. The corporate maintains a conservative dividend payout ratio of round 40% and carries little or no debt.

Jack Henry & Associates is not explosive, however its regular progress provides up. The inventory has overwhelmed the S&P 500 for a lot of many years. Analysts count on excessive single-digit earnings progress over the long run, which is able to proceed to gas future dividend raises. These seeking to purchase and sleep nicely at evening ought to strongly think about proudly owning shares.

3. BlackRock

Traders can ensure that BlackRock (NYSE: BLK) will probably be round so long as the worldwide monetary system itself. BlackRock is the world’s largest funding administration firm, with over $10 trillion in belongings beneath administration. It affords advisory companies and funding merchandise, together with the namesake funds it is well-known for.

BlackRock’s funds personal massive stakes in lots of the world’s prime firms. It is vital to do not forget that BlackRock’s funds personal these stakes, not the firm. In different phrases, these are investments on behalf of BlackRock’s shoppers who put their cash in these funds.

BlackRock earns cash from varied charges, starting from a reduce of its managed belongings to rendered companies. Market downturns can damage the corporate; fearful buyers pulling funds and shrinking asset values will sometimes damage BlackRock’s enterprise. Nevertheless, just like the S&P 500, BlackRock continues to get well and develop to new heights. That basically builds progress into the corporate, leading to market-beating returns over the inventory’s lifetime.

The corporate is poised to stay a strong dividend inventory transferring ahead. BlackRock has paid and raised its dividend for 15 consecutive years and was capable of freeze its dividend moderately than reduce it in 2008-2009. Analysts anticipate 13% annualized double-digit earnings progress transferring ahead, and the payout ratio is already simply 51%. That ought to spell loads of sizable dividend raises sooner or later.

Don’t miss this second likelihood at a doubtlessly profitable alternative

Ever really feel such as you missed the boat in shopping for essentially the most profitable shares? You then’ll need to hear this.

On uncommon events, our professional workforce of analysts points a suggestion for firms that they assume are about to pop. In the event you’re anxious you’ve already missed your likelihood to speculate, now’s one of the best time to purchase earlier than it’s too late. And the numbers converse for themselves:

-

Amazon: if you happen to invested $1,000 after we doubled down in 2010, you’d have $21,904!*

-

Apple: if you happen to invested $1,000 after we doubled down in 2008, you’d have $43,562!*

-

Netflix: if you happen to invested $1,000 after we doubled down in 2004, you’d have $349,245!*

Proper now, we’re issuing “Double Down” alerts for 3 unbelievable firms, and there will not be one other likelihood like this anytime quickly.

*Inventory Advisor returns as of July 8, 2024

has positions in Visa. The Motley Idiot has positions in and recommends Visa. The Motley Idiot recommends Jack Henry & Associates. The Motley Idiot has a .

was initially printed by The Motley Idiot

Corporations that determine to separate their inventory — growing share rely and lowering per-share worth — are normally doing fairly nicely. Most corporations do not announce inventory splits except their shares have climbed considerably over time.

Nonetheless, there are events when a inventory break up happens throughout a rocky interval for the corporate’s shares. That is the case for Tremendous Micro Laptop (NASDAQ: SMCI), whose inventory is down 35% since its announcement in early August.

Nonetheless, many analysts on Wall Road consider there may be large potential for Supermicro. So, is it time to purchase?

Supermicro’s enterprise is booming

On Sept. 25, a bunch of 16 analysts had a median one-year worth goal on Supermicro inventory of $729.19. That represents round 60% upside from the inventory’s closing worth on Sept. 25, which was a day earlier than a Wall Road Journal article helped gas a 12% drop.

The optimism is sensible. Tremendous Micro Laptop manufactures parts for computing servers. Whereas this area is comparatively crowded, Supermicro units itself other than the competitors by providing extremely customizable servers that may be tailor-made to any workload sort or dimension. Its merchandise are additionally among the most energy-efficient ones on the market, which might save on long-term working prices.

With the huge spike in computing demand brought on by the substitute intelligence (AI) arms race, Supermicro is benefiting from the identical traits that despatched Nvidia inventory by way of the roof, although Supermicro’s journey has been a bit extra bumpy.

Supermicro isn’t firing on all cylinders proper now

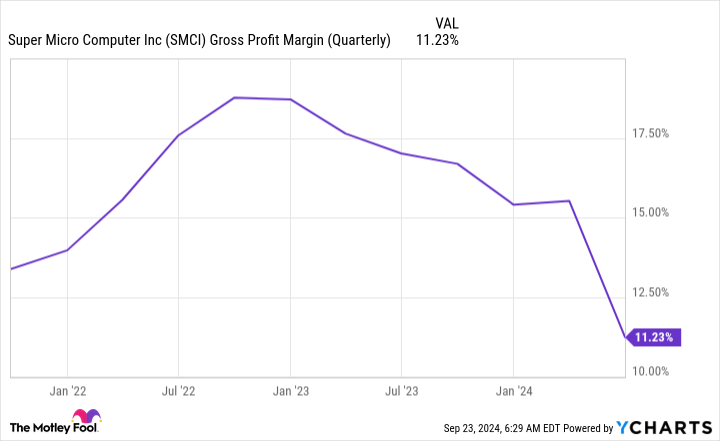

Together with Supermicro’s 10-for-1 stock-split announcement on Aug. 6, the corporate launched its fiscal 2024 fourth-quarter and full-year outcomes for the interval ended June 30. Whereas the corporate delivered robust income progress of 143% 12 months over 12 months and supplied wonderful full-year 2025 steerage of 74% to 101% progress, there have been some issues with its profitability.

Due to its new liquid-cooling product line getting spun up, Supermicro’s gross margin has taken a success.

This has brought about vital concern amongst some buyers as falling gross margin also can point out elevated competitors. Nonetheless, administration believes its gross margin will recuperate all through fiscal 2025.

In the meantime, short-selling agency Hindenburg Analysis launched a report on Supermicro on Aug. 27 alleging accounting manipulation. The SEC has fined Supermicro for accounting points up to now. On the identical time, as a result of Hindenburg is a short-seller, it advantages when the shares it experiences on fall, so buyers ought to proceed cautiously with this data. Supermicro responded that the quick report “comprises false or inaccurate statements.”

On Aug. 28, Supermicro delayed submitting its end-of-year Type 10-Okay with the SEC, saying it wanted extra time to “full its evaluation of the design and working effectiveness of its inner controls over monetary reporting.”

After the delay, Supermicro obtained a letter of non-compliance from the Nasdaq change, stating it’s in violation of itemizing guidelines as a result of it hasn’t filed its 10-Okay in a well timed vogue. After receiving the letter on Sept. 16, Supermicro has 60 days to conform or danger being delisted.

To additional complicate issues, on Sept. 26, The Wall Road Journal reported that unnamed sources had stated the Division of Justice had launched a probe into the corporate. If the reporting is right, that is only a preliminary probe, so nothing might come out of it. Nonetheless, there may very well be actual points with the corporate, which considerably will increase the chance of investing within the inventory. It can probably be a very long time earlier than the general public will get full particulars, so buyers might want to keep affected person with the inventory in the event that they select to purchase it.

Clearly, the corporate is grappling with severe points proper now, and the inventory has fallen over 60% from its 52-week excessive. Nonetheless, the enterprise case for its parts and servers is plain.

The present inventory can be valued pretty cheaply on a ahead earnings foundation.

If Supermicro can enhance its gross margin over the subsequent 12 months and dispel considerations over its accounting practices, the inventory has a ton of upside.

as a result of I consider within the firm. Nonetheless, I stored the place dimension low (round 1% of my complete portfolio worth). That manner, it will not have an effect on the portfolio an excessive amount of if the inventory tumbles additional, however I can nonetheless profit if Supermicro levels a restoration like some on Wall Road assume it could actually within the close to time period. I used to be planning on shopping for extra, however after the report of a possible DOJ probe, I am comfy with the present place dimension, because it represents the excessive danger, excessive reward related to Tremendous Micro Laptop’s inventory.

Must you make investments $1,000 in Tremendous Micro Laptop proper now?

Before you purchase inventory in Tremendous Micro Laptop, think about this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they consider are the for buyers to purchase now… and Tremendous Micro Laptop wasn’t certainly one of them. The ten shares that made the minimize may produce monster returns within the coming years.

Think about when Nvidia made this checklist on April 15, 2005… in the event you invested $1,000 on the time of our suggestion, you’d have $760,130!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has positions in Tremendous Micro Laptop. The Motley Idiot has positions in and recommends Nvidia. The Motley Idiot has a .

was initially revealed by The Motley Idiot

By Abigail Summerville

NEW YORK (Reuters) – Morgan Stanley’s middle-market buyout arm is exploring a sale of Sila Companies that might worth the residential companies firm at about $1.5 billion, together with debt, individuals acquainted with the matter mentioned on Friday.

King Of Prussia, Pennsylvania-based Sila, which is a supplier of companies together with heating, air-conditioning, and plumbing, is working with funding financial institution William Blair on the sale course of, the sources mentioned, requesting anonymity because the matter is confidential.

Sila may command a valuation equal to about 15 occasions its 12-month earnings earlier than curiosity, taxes, depreciation and amortization of almost $100 million, the sources mentioned.

Morgan Stanley Capital Companions, which owns Sila, declined to remark. William Blair and Sila didn’t reply to requests for remark.

Based in 1989, Sila operates over 30 manufacturers that present companies together with residential heating, air flow, and air-con, electrical, and plumbing within the Northeast, Mid-Atlantic, and Midwest elements of the USA.

MSCP, which acquired Sila for an undisclosed quantity in 2021, focuses on buying mid-sized companies and is housed inside Morgan Stanley Funding Administration, which manages $1.5 trillion of belongings.

Non-public fairness companies have historically been prolific acquirers of companies within the residential companies business, due to their regular money flows and the chance to drive consolidation within the fragmented sector.

Normal Atlantic invested in Flint Group earlier this 12 months, whereas L Catterton acquired LTP House Companies Group in 2022. Residential companies agency The Wrench Group counts TSG Client Companions, Leonard Inexperienced & Companions, and Oak Hill Capital as buyers.

Markets

Cathie Wooden's Ark Make investments Dumps Palantir Shares Amidst S&P 500 Inclusion And Prolonged AI Alliance

Benzinga and Lusso’s Information LLC might earn fee or income on some objects by means of the hyperlinks beneath.

On Wednesday, the Cathie Wooden-led Ark Make investments made a notable transfer by promoting a good portion of its stake in Palantir Applied sciences Inc (NYSE:).

The Palantir Commerce: The ARK Innovation ETF (NYSE:) offloaded 62,809 shares of Palantir. The sale got here simply days after, changing American Airways Group, Inc. This inclusion may probably enhance Palantir’s inventory because it beneficial properties wider publicity to traders and as shares are amassed to be included in index funds that mirror the S&P 500. Regardless of the optimistic information, Ark Make investments determined to cut back its publicity to the corporate.

Don’t Miss:

Furthermore, the sale occurred on the identical day of its cope with APA Company. The deal, which builds on three years of collaboration, introduces new AI capabilities by means of Palantir’s Synthetic Intelligence Platform (AIP) software program. Regardless of these developments, Ark Make investments’s transfer suggests a strategic shift in its funding strategy in the direction of Palantir.

The worth of the commerce, based mostly on Palantir’s closing worth of $37.12 on the identical day, is roughly $2.33 million.

Trending: This billion-dollar fund has invested within the subsequent huge actual property increase, .

It is a paid commercial. Rigorously think about the funding aims, dangers, fees and bills of the Fundrise Flagship Fund earlier than investing. This and different info will be discovered within the. Learn them fastidiously earlier than investing.

Different Key Trades:

-

Ark Make investments’s ARK Genomic Revolution ETF (ARKG) offered shares of Veeva Techniques Inc (VEEV) and shares of Butterfly Community Inc (BFLY).

-

The ARK Autonomous Know-how & Robotics ETF (ARKQ) offered shares of Materialise NV (MTLS) and likewise shares of Vuzix Corp (VUZI).

-

The ARK Subsequent Technology Web ETF (ARKW) offered shares of Roku Inc (ROKU). The ARK Area Exploration & Innovation ETF (ARKX) purchased shares of Blade Air Mobility Inc (BLDE) and offered shares of Mynaric AG (MYNA).

Questioning in case your investments can get you to a $5,000,000 nest egg? Converse to a monetary advisor as we speak. matches you up with as much as three vetted monetary advisors who serve your space, and you may interview your advisor matches for gratis to determine which one is best for you.

Preserve Studying:

-

Fractional actual property is the following huge alternative for constructing passive revenue —.

-

With returns as excessive as 300%, it’s no surprise this asset is the funding selection of many billionaires..

This text initially appeared on

Is Inventory-Break up Inventory Tremendous Micro Laptop Headed to $729 per Share?

Morgan Stanley's personal fairness arm explores sale of HVAC agency Sila, sources say

Cathie Wooden's Ark Make investments Dumps Palantir Shares Amidst S&P 500 Inclusion And Prolonged AI Alliance

Fed chair Powell speech, Chicago PMI in focus Monday

Why Nio Inventory Surged Extra Than 20% This Week

Report Galapagos debt-for-nature swap scrutinized over transparency irregularities claims

Clock is ticking for US recession, return of Fed's QE, says black swan fund

Apple should face narrowed privateness lawsuit over its apps

New PCE studying helps case for smaller Fed price lower in November

Alibaba, Eli Lilly lead Friday's morning market cap inventory movers

Inventory market at the moment: Shares acquire as Fed's favored inflation gauge cools

ITA expects greater full-year income because it prepares to affix Lufthansa group

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoDown 30% From Its All-Time Excessive, Ought to You Purchase Synthetic Intelligence (AI) Famous person Tremendous Micro Pc?

-

Markets3 months ago

Markets3 months agoADP Stories Decrease-Than-Anticipated Personal Payroll Progress for June

-

Markets3 months ago

Markets3 months agoSorry, however retiring ‘comfortably’ on $100K is a fantasy for most individuals. Right here’s why.

-

Markets3 months ago

Markets3 months agoAbove Food Corp. (NASDAQ: ABVE) and Chewy Inc. (NYSE: CHWY) Making Headlines This Week

-

Markets3 months ago

Markets3 months agoSouthwest Air adopts 'poison tablet' as activist investor Elliott takes important stake in firm

-

Markets3 months ago

Markets3 months agoCore Scientific so as to add 15 EH/s by means of Block’s 3nm Bitcoin mining ASICs

-

Markets3 months ago

Markets3 months agoWarren Buffett is popping 94 subsequent month. Ought to Berkshire traders begin to fear?

-

Markets3 months ago

Markets3 months agoWhy Rivian Inventory Roared Forward 10% on Friday

-

Markets3 months ago

Markets3 months agoArgentina to Promote {Dollars} In Parallel FX Market, Caputo Says

-

Markets3 months ago

Markets3 months agoWhy Intel Inventory Popped on Friday