Markets

Neglect Nvidia: 1 Different Unstoppable Semiconductor Inventory to Purchase As a substitute

Synthetic intelligence (AI) has captivated buyers throughout the board. From giant institutional monetary companies companies to smaller retail buyers, AI is enjoying an enormous function in how cash is shifting these days.

What’s a bit of shocking, nevertheless, is that capital seems to be primarily concentrated in a small basket of mega-cap know-how shares. The “” is a time period used to collectively describe the world’s largest tech firms — and unsurprisingly, all of them are disrupting AI in some type.

Maybe probably the most intriguing member of the Magnificent Seven is chief Nvidia. Whereas the corporate seems to have an edge over its friends, buyers ought to perceive that the chip realm has many alternative parts.

In different phrases, not all semiconductor companies are creating merchandise that compete with Nvidia. In reality, many chip firms are working alongside Nvidia and are benefiting because of the corporate’s development.

One chip inventory that I believe is quietly hovering underneath the radar proper now could be Micron Expertise (NASDAQ: MU). Let’s dig into Micron’s enterprise and assess why now seems to be like a profitable alternative for long-term buyers to scoop up some shares.

How does Micron profit from Nvidia?

Nvidia develops a sequence of refined pc chips referred to as graphics processing items (GPUs). These play an enormous function in generative AI purposes reminiscent of machine studying, coaching giant language fashions (LLMs), and quantum computing.

Whereas Nvidia faces competitors from AMD and Intel, the corporate is estimated to have at the very least 80% of the AI-powered chip market. Nvidia has constructed its lead over the competitors due to demand for its H100 and A100 merchandise. The corporate has additionally already developed its next-generation line of GPUs, often called Blackwell and Rubin.

Micron focuses on reminiscence storage merchandise which might be built-in into chips. Micron is not competing with Nvidia. Fairly, the corporate truly works with Nvidia and is benefiting from the demand fueling chips proper now.

Offered out by means of subsequent yr

One among Micron’s core merchandise is named the Excessive Bandwidth Reminiscence (HBM) 3E, which is layered on Nvidia’s GPUs. The corporate started transport its HBM3E merchandise throughout this previous spring. Whereas it is nonetheless a brand new product for Micron, the preliminary traction from HBM3E offers buyers quite a bit to be enthusiastic about.

For its fiscal 2024’s third quarter (ended Might 30), Micron generated $6.8 billion in income — up 84% yr over yr. HBM contributed $100 million through the quarter as shipments started to ramp. Administration said: “We count on to generate a number of hundred million {dollars} of income from HBM in fiscal 2024 and a number of billions of {dollars} in income from HBM in fiscal 2025.”

Moreover, administration actually shocked buyers once they famous that “HBM is bought out for calendar 2024 and 2025, with pricing already contracted for the overwhelming majority of our 2025 provide.”

Is now a superb time to purchase Micron inventory?

The chart under illustrates the price-to-free money stream (P/FCF) a number of for Micron over the past three years. Though a P/FCF of 68.9 is expensive, the a number of is notably decrease than in some prior durations.

Admittedly, the valuation evaluation above might be deceptive. A part of the rationale why Micron’s P/FCF is normalizing is as a result of, like many know-how companies, the corporate is experiencing irregular demand proper now. Because of this, income and margins are accelerating.

Nonetheless, the blemish with Micron revolves round profitability. The corporate inconsistently reviews constructive working revenue, free money stream, and internet revenue. Which means that throughout some quarters, the corporate truly posts a internet loss.

For the reason that semiconductor house is very cyclical, Micron’s ebbs and flows relating to earnings aren’t fully shocking. Nonetheless, I am optimistic that the success of the HBM options can assist Micron attain a point of pricing energy because it seems to be to satisfy provide and demand. In concept, this could assist easy out the corporate’s money stream and profitability.

For these causes, I believe Micron is well-positioned to proceed benefiting from the AI increase and the particular demand tendencies surrounding chip companies. Furthermore, provided that its newest innovation is already bought out by means of subsequent yr, I believe it is apparent that the corporate’s merchandise are well-received.

Whereas shares of Micron aren’t essentially grime low-cost, I see the inventory as a compelling purchase for long-term buyers on the lookout for alternate options to Nvidia.

Must you make investments $1,000 in Micron Expertise proper now?

Before you purchase inventory in Micron Expertise, contemplate this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they imagine are the for buyers to purchase now… and Micron Expertise wasn’t one in all them. The ten shares that made the reduce may produce monster returns within the coming years.

Take into account when Nvidia made this listing on April 15, 2005… should you invested $1,000 on the time of our advice, you’d have $791,929!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of July 8, 2024

has positions in Nvidia. The Motley Idiot has positions in and recommends Superior Micro Units and Nvidia. The Motley Idiot recommends Intel and recommends the next choices: lengthy January 2025 $45 calls on Intel and brief August 2024 $35 calls on Intel. The Motley Idiot has a .

was initially printed by The Motley Idiot

Markets

Prediction: SoFi Inventory Will Soar Over the Subsequent 5 Years. Right here's 1 Motive Why.

The inventory of SoFi Applied sciences (NASDAQ: SOFI) has been crushed this yr after doubling final yr. It is down 20% yr so far regardless of what looks as if fairly strong efficiency.

Nonetheless, the tide may flip, and shortly. Let’s examine why SoFi inventory may soar over the following 5 years.

Expanded enterprise, decrease rates of interest

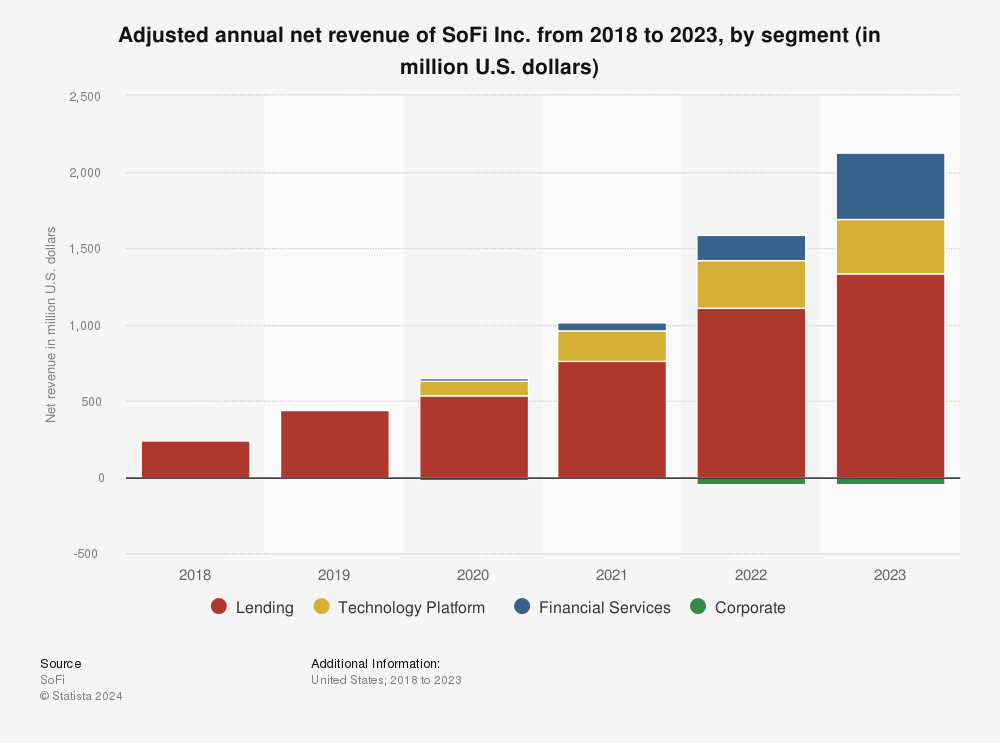

SoFi’s most important enterprise is lending, however it has expanded into a big array of economic providers like financial institution accounts and investments. Providing different providers gives a number of advantages for SoFi.

It provides it new income sources, it creates higher cross-platform engagement amongst present members, it may possibly entice new members, and — what stands out now — is that it shields the enterprise from the .

Lending generally is a profitable enterprise, however it’s extremely delicate to rates of interest, and SoFi’s lending phase has been below strain as charges stay excessive.

Now that rates of interest seem like they will begin coming down, the strain ought to start to ease. In the meantime, the opposite segments are nonetheless in progress mode, and so they proceed to account for a better proportion of the corporate’s general enterprise.

The lending phase continues to develop, however the non-lending segments are rising a lot quicker. They accounted for 45% of the enterprise within the 2024 second quarter, up from 38% a yr in the past. As the opposite segments outpace lending progress, SoFi will develop into a extra steady enterprise, with decrease publicity to rate of interest motion.

If the lending phase picks up with decrease charges, which is how the phase works, traders’ present considerations in regards to the enterprise will fall away. Whenever you mix that with the power within the firm’s growth mannequin, SoFi inventory may explode over the following 5 years, and now could possibly be a good time to purchase in.

Must you make investments $1,000 in SoFi Applied sciences proper now?

Before you purchase inventory in SoFi Applied sciences, contemplate this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the for traders to purchase now… and SoFi Applied sciences wasn’t one in all them. The ten shares that made the reduce may produce monster returns within the coming years.

Contemplate when Nvidia made this checklist on April 15, 2005… for those who invested $1,000 on the time of our suggestion, you’d have $743,952!*

Inventory Advisor gives traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has positions in SoFi Applied sciences. The Motley Idiot has no place in any of the shares talked about. The Motley Idiot has a .

was initially printed by The Motley Idiot

Lusso’s Information – Saudi Arabia shares have been decrease after the shut on Sunday, as losses within the , and sectors led shares decrease.

On the shut in Saudi Arabia, the misplaced 0.83%.

One of the best performers of the session on the have been Bindawood Holding Co (TADAWUL:), which rose 6.01% or 0.45 factors to commerce at 7.94 on the shut. In the meantime, Thimar Improvement Holding Co (TADAWUL:) added 5.71% or 2.80 factors to finish at 51.80 and Americana Eating places (TADAWUL:) was up 5.30% or 0.14 factors to 2.78 in late commerce.

The worst performers of the session have been Dallah Healthcare Holding Firm (TADAWUL:), which fell 4.98% or 8.40 factors to commerce at 160.40 on the shut. Halwani Bros (TADAWUL:) declined 4.97% or 3.40 factors to finish at 65.00 and Astra Industrial Group (TADAWUL:) was down 3.10% or 5.40 factors to 168.60.

Falling shares outnumbered advancing ones on the Saudi Arabia Inventory Trade by 166 to 120 and 26 ended unchanged.

Crude oil for November supply was up 1.43% or 0.97 to $68.64 a barrel. Elsewhere in commodities buying and selling, Brent oil for supply in December rose 0.63% or 0.45 to hit $71.54 a barrel, whereas the December Gold Futures contract fell 0.52% or 14.10 to commerce at $2,680.80 a troy ounce.

EUR/SAR was unchanged 0.10% to 4.19, whereas USD/SAR unchanged 0.01% to three.75.

The US Greenback Index Futures was down 0.14% at 100.11.

Markets

2 Progress Shares to Purchase Earlier than They Soar 212% and 712%, Based on Sure Wall Road Analysts

The S&P 500 (SNPINDEX: ^GSPC) has superior 20% 12 months to this point as a consequence of robust curiosity in synthetic intelligence and surprisingly strong financial development. However sure Wall Road analysts consider UiPath (NYSE: PATH) and Roku (NASDAQ: ROKU) are undervalued.

-

Sanjit Singh at Morgan Stanley has set UiPath with a bull-case value goal of $40 per share by September 2025. That forecast implies 212% upside from its present share value of $12.80

-

Nicholas Grous and Andrew Kim at Ark Make investments have set Roku with a base-case value goal of $605 by December 2026. That forecast implies 712% upside from its present share value of $74.50.

As a rule, buyers ought to by no means put an excessive amount of confidence in value targets, particularly once they come from particular person analysts. Nor ought to they take the implicit good points as a right. However UiPath and Roku warrant additional consideration.

UiPath: 212% implied upside

UiPath makes a speciality of robotic course of automation (RPA), one of many fastest-growing software program markets. Its enterprise automation platform contains process and course of mining instruments that assist customers establish alternatives for automation, and growth instruments that assist customers construct software program robots able to automating these duties and processes.

Morgan Stanley says UiPath is the “clear class defining chief” in RPA, however analysts have acknowledged the corporate in different areas. As an example, the Worldwide Information Corp. not too long ago acknowledged UiPath as a frontrunner in clever doc processing (IDP) software program, which blends and RPA to automate duties like doc classification, information extraction, and sentiment evaluation.

UiPath reported combined monetary leads to the second quarter of fiscal 2025 (ended July 31). The typical buyer spent 15% extra and income elevated 10% to $316 million. However gross margin contracted about 3 share factors, and adjusted earnings fell 55% to $0.04 per diluted share. Nevertheless, buyers have cause to be cautiously optimistic.

UiPath introduced co-founder Daniel Dines again as CEO in June to enhance gross sales execution, particularly the place development merchandise like clever doc processing are involved, and to steer the corporate by way of an unsure financial system. Enhancements would require time, however Dines mentioned he was inspired by the early progress within the second quarter. “I am significantly excited concerning the success we have seen with our IDP options.”

Going ahead, Wall Road expects UiPath to develop gross sales at 10% yearly by way of fiscal 2026 (ends April 2026). That estimate leaves room for upside as a result of the RPA market is forecasted to develop at 40% yearly by way of 2030. Nevertheless, the present valuation of 5.2 occasions gross sales is cheap even when the Wall Road consensus is right.

Absent a major acceleration in development, UiPath shareholders have little or no probability of triple-digit returns within the subsequent 12 months. However buyers keen to carry the inventory for 3 to 5 years at a minimal ought to contemplate shopping for a small place at the moment. UiPath may very well be a rewarding turnaround story.

Roku: 712% implied upside

Roku’s streaming platform connects shoppers, content material writer, and advertisers. The corporate monetizes paid content material by charging charges for transactions processed by way of Roku Pay, and it monetizes ad-supported content material by promoting stock and advert tech software program. Roku sources promoting stock from content material publishers on the platform, nevertheless it additionally operates an ad-supported service known as The Roku Channel.

Roku is the preferred streaming platform within the U.S. as measured by streaming time, and the corporate is nicely positioned to take care of its management. Roku OS is the best-selling TV working system within the U.S., Canada, and Mexico, which factors to model authority. Indee, within the second quarter, Roku OS was extra widespread than the following two working programs mixed by way of TV unit gross sales.

Roku reported encouraging leads to the second quarter. Energetic accounts elevated 14% and streaming hours jumped 20%, which suggests the common account engaged with the platform extra continuously. In flip, income rose 14% to $968 million and adjusted EBITDA improved to $44 million, up from a lack of $18 million within the prior 12 months. Traders have good cause to assume the corporate will preserve its momentum.

Along with Roku being the preferred streaming platform in North America, The Roku Channel is the eighth-most widespread streaming service within the U.S., outranking Max by Warner Bros. Discovery and Paramount+ by Paramount World. That leaves the corporate nicely place to learn as streaming accounts for extra of TV viewing time and advertisers spend extra on related TV (CTV).

Wall Road expects Roku’s income to compound at 13% yearly by way of 2025, however that estimate leaves room for upside. CTV advert spending is projected to develop at 12% yearly throughout the identical interval, and Roku’s management within the North America (coupled with its increasing presence in worldwide markets) might result in faster-than-expected development.

Having mentioned that, the present valuation of two.8 occasions gross sales is cheap even when the Wall Road consensus is correct. Personally, I feel Ark’s value goal of $605 per share is absurdly excessive. However I additionally assume Roku can beat the S&P 500 over the following three to 5 years. So, affected person buyers ought to really feel comfy shopping for a small place at the moment.

Do you have to make investments $1,000 in Roku proper now?

Before you purchase inventory in Roku, contemplate this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the for buyers to purchase now… and Roku wasn’t one in every of them. The ten shares that made the lower might produce monster returns within the coming years.

Think about when Nvidia made this record on April 15, 2005… when you invested $1,000 on the time of our suggestion, you’d have $743,952!*

Inventory Advisor gives buyers with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has positions in Roku and UiPath. The Motley Idiot has positions in and recommends Roku, UiPath, and Warner Bros. Discovery. The Motley Idiot has a .

was initially printed by The Motley Idiot

Prediction: SoFi Inventory Will Soar Over the Subsequent 5 Years. Right here's 1 Motive Why.

Saudi Arabia shares decrease at shut of commerce; Tadawul All Share down 0.83%

2 Progress Shares to Purchase Earlier than They Soar 212% and 712%, Based on Sure Wall Road Analysts

When the greenback retailer closes, US households on meals advantages lose a lifeline

Prediction: Nvidia Inventory Will Surge Into 2025. Right here's Why.

India to probe fireplace at Tata plant making elements for Apple iPhones

3 Good AI Shares Billionaires Are Shopping for for the three Levels of the Synthetic Intelligence Increase

Leveraging GenAI for asset administration

Ought to You Promote Nvidia; Purchase China? That's What This Billionaire Investor Is Doing

Institutional buyers extra assured in comfortable touchdown, says Morgan Stanley

UBS chair warns towards huge enhance in capital necessities, newspaper reviews

Road calls of the week

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoADP Stories Decrease-Than-Anticipated Personal Payroll Progress for June

-

Markets3 months ago

Markets3 months agoSorry, however retiring ‘comfortably’ on $100K is a fantasy for most individuals. Right here’s why.

-

Markets3 months ago

Markets3 months agoSouthwest Air adopts 'poison tablet' as activist investor Elliott takes important stake in firm

-

Markets3 months ago

Markets3 months agoAbove Food Corp. (NASDAQ: ABVE) and Chewy Inc. (NYSE: CHWY) Making Headlines This Week

-

Markets3 months ago

Markets3 months agoCore Scientific so as to add 15 EH/s by means of Block’s 3nm Bitcoin mining ASICs

-

Markets3 months ago

Markets3 months agoWarren Buffett is popping 94 subsequent month. Ought to Berkshire traders begin to fear?

-

Markets3 months ago

Markets3 months agoWhy Rivian Inventory Roared Forward 10% on Friday

-

Markets3 months ago

Markets3 months agoArgentina to Promote {Dollars} In Parallel FX Market, Caputo Says

-

Markets3 months ago

Markets3 months agoWhy Intel Inventory Popped on Friday

-

Markets3 months ago

Markets3 months agoMicrosoft in $22 million deal to settle cloud grievance, keep off regulators

-

Markets3 months ago

Markets3 months agoMorgan Stanley raises worth targets on score companies on constructive outlook