Markets

Overlook Nvidia: The Synthetic Intelligence (AI) Chief's High Billionaire Vendor Is Shopping for These 4 Supercharged Development Shares As an alternative

Because the web first started to proliferate three a long time in the past, Wall Road and traders have been ready for the following large innovation that may alter the expansion trajectory of company America. The revolution seems to be answering the decision for game-changing progress.

With AI, software program and programs are used rather than people to supervise or undertake duties. What provides this know-how such broad-reaching utility is the potential for software program and programs to be taught and evolve with out human oversight.

Though progress estimates are all around the map in terms of AI, the analysts at PwC launched a report final yr that estimated the know-how would add $15.7 trillion to the worldwide financial system come 2030. With an addressable market this massive, there are sure to be a number of big-time winners, which is why we have witnessed traders pile into AI shares.

Nonetheless, optimism surrounding AI shares is not common amongst Wall Road’s brightest and richest traders.

Nvidia’s high billionaire vendor dumped over 29 million (split-adjusted) shares within the first quarter

Based mostly on Type 13F filings with the Securities and Alternate Fee — 13Fs present a snapshot of what Wall Road’s most-successful cash managers have been shopping for and promoting within the newest quarter — of AI chief Nvidia (NASDAQ: NVDA) in the course of the first quarter. However no billionaire seemingly mashed the promote button more durable than Coatue Administration’s Philippe Laffont.

Factoring in that Nvidia has since accomplished a 10-for-1 forward-stock break up, Laffont’s fund bought the equal of 29,370,600 shares of Nvidia, or roughly 68% of Coatue’s prior stake within the firm.

Regardless of Nvidia having a veritable monopoly on AI-powered graphics processing models (GPUs) in high-compute knowledge facilities, and having fun with otherworldly pricing energy resulting from demand for AI-GPUs overwhelming provide, Laffont seemingly had a lot of viable causes to run for the exit.

To state the apparent, he and his group could have merely been locking in a few of their positive factors. Nvidia’s inventory has gained almost $3 trillion in market worth for the reason that begin of 2023, which is a stage of scaling we have merely by no means witnessed earlier than.

A extra prevailing concern for Nvidia and Laffont may be historical past. There hasn’t been a brand new innovation or know-how in 30 years (together with the arrival of the web) that is prevented an early stage bubble. Investor euphoria for brand spanking new improvements constantly ignores that every one new improvements want time to mature. Synthetic intelligence is unlikely to interrupt this pattern, which might ultimately expose Nvidia to some severe draw back.

Nvidia can also be contending with its first actual semblance of competitors in AI-accelerated knowledge facilities. Along with exterior opponents rolling out their AI-GPUs, Nvidia’s high clients are additionally creating AI-GPUs for his or her knowledge facilities. This all interprets to lowered AI-GPU shortage and waning pricing energy for AI chief Nvidia.

However whereas Philippe Laffont and his group have been busy dumping shares of Nvidia within the March-ended quarter, they could not cease shopping for shares of 4 different supercharged progress shares.

Taiwan Semiconductor Manufacturing

One of the fascinating strikes made by billionaire Philippe Laffont and his funding group in the course of the first quarter was shopping for greater than 10 million shares (10,027,552, to be exact) of world-leading chip fabrication firm Taiwan Semiconductor Manufacturing (NYSE: TSM).

Taiwan Semi, which is now Coatue’s fifth-largest place by market worth (as of March 31), gives its providers to many of the high tech firms and semiconductor titans, together with Nvidia. With demand for AI-GPUs swamping provide, chip-fab firms like Taiwan Semiconductor, that are accountable for packaging the high-bandwidth reminiscence that make high-compute knowledge facilities tick, ought to get pleasure from an intensive backlog of orders.

Moreover, Taiwan Semi is steadily lowering the geopolitical danger that had beforehand weighed down its valuation. The foundry big opened its first Japan-based plant earlier this yr, and expects to start manufacturing at a brand new facility in Arizona by someday in 2025. This implies geopolitical tensions between China and Taiwan will not be as doubtlessly damning to its future capability.

Salesforce

A second supercharged progress inventory that Laffont and his funding group have been shopping for as an alternative of Nvidia in the course of the March-ended quarter is cloud-based buyer relationship administration (CRM) software program options supplier Salesforce (NYSE: CRM). Laffont more-than-doubled Coatue Administration’s stake in Salesforce by choosing up 2,556,774 shares within the first three months of the yr.

The first cause Salesforce has labored its strategy to Coatue’s fourth-largest holding most likely has to do with the corporate’s seemingly impenetrable moat in cloud-based CRM software program. A latest report from IDC notes that Salesforce has been the worldwide No. 1 in CRM software program gross sales for 12 consecutive years. Additional, its 21.7% worldwide CRM market share is over thrice larger than its next-closest competitor (Microsoft at 5.9%).

On high of a sustained double-digit progress runway for cloud-based CRM software program, CEO and co-founder Marc Benioff has orchestrated a lot of earnings-accretive acquisitions, together with MuleSoft, Tableau Software program, and Slack Applied sciences. Bolt-on acquisitions broaden the corporate’s providers ecosystem and supply ample cross-selling alternatives.

Alphabet

The third high-octane progress inventory Laffont was busy shopping for whereas sending shares of AI kingpin Nvidia to the chopping block is Alphabet (NASDAQ: GOOGL)(NASDAQ: GOOG), the mum or dad firm of web search engine Google, streaming platform YouTube, autonomous driving firm Waymo, and cloud infrastructure service platform Google Cloud. Coatue’s first-quarter 13F exhibits the fund’s place in Alphabet’s Class A shares (GOOGL) grew by 138%, or 2,597,338 shares.

Much like Taiwan Semi and Salesforce, the lure of Alphabet may be so simple as its impenetrable moat in web search. For greater than 9 years, Google has accounted for no less than a 90% month-to-month share of worldwide web search. As a rule, this affords the corporate distinctive ad-pricing energy, which ends up in an abundance of working money circulation.

Within the second half of this decade, Google Cloud is liable to be Alphabet’s fastest-growing phase. Enterprise cloud spending remains to be in its comparatively early levels of ramping up, and Google Cloud made the shift to recurring income final yr. Since cloud-service margins are noticeably larger than promoting margins, this phase ought to present a pleasant raise to Alphabet’s money circulation within the years to come back.

PayPal

The fourth supercharged progress inventory Nvidia’s high billionaire vendor was a big-time purchaser of in the course of the March-ended quarter is monetary know-how (“fintech”) juggernaut PayPal Holdings (NASDAQ: PYPL). Laffont oversaw the addition of 8,014,159 shares of PayPal, making it Coatue’s Sixteenth-largest holding by market worth, as of March 31.

Despite rising competitors within the digital fee house, lots of PayPal’s key efficiency metrics are transferring in the suitable course. Particularly, fee transactions grew by 11% from the earlier yr to six.5 billion, whole fee quantity elevated by 14% on a constant-currency foundation to virtually $404 billion, and engagement amongst energetic accounts continues to climb. Over the trailing-12-month (TTM) interval, ended March 31, the common energetic account accomplished 60 funds, which is up from a median of 40.9 funds over the TTM for energetic accounts, as of the top of 2020.

Moreover, new CEO Alex Chriss has a great understanding of what small companies have to succeed. He is overseeing the introduction of a brand new promoting platform for PayPal and has been mindfully monitoring spending to spice up margins.

Do you have to make investments $1,000 in Nvidia proper now?

Before you purchase inventory in Nvidia, take into account this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they imagine are the for traders to purchase now… and Nvidia wasn’t one among them. The ten shares that made the reduce might produce monster returns within the coming years.

Contemplate when Nvidia made this listing on April 15, 2005… when you invested $1,000 on the time of our advice, you’d have $771,034!*

Inventory Advisor gives traders with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of July 8, 2024

Suzanne Frey, an govt at Alphabet, is a member of The Motley Idiot’s board of administrators. has positions in Alphabet and PayPal. The Motley Idiot has positions in and recommends Alphabet, Microsoft, Nvidia, PayPal, Salesforce, and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft, brief January 2026 $405 calls on Microsoft, and brief June 2024 $62.50 calls on PayPal. The Motley Idiot has a .

was initially printed by The Motley Idiot

Corporations that determine to separate their inventory — growing share rely and lowering per-share worth — are normally doing fairly nicely. Most corporations do not announce inventory splits except their shares have climbed considerably over time.

Nonetheless, there are events when a inventory break up happens throughout a rocky interval for the corporate’s shares. That is the case for Tremendous Micro Laptop (NASDAQ: SMCI), whose inventory is down 35% since its announcement in early August.

Nonetheless, many analysts on Wall Road consider there may be large potential for Supermicro. So, is it time to purchase?

Supermicro’s enterprise is booming

On Sept. 25, a bunch of 16 analysts had a median one-year worth goal on Supermicro inventory of $729.19. That represents round 60% upside from the inventory’s closing worth on Sept. 25, which was a day earlier than a Wall Road Journal article helped gas a 12% drop.

The optimism is sensible. Tremendous Micro Laptop manufactures parts for computing servers. Whereas this area is comparatively crowded, Supermicro units itself other than the competitors by providing extremely customizable servers that may be tailor-made to any workload sort or dimension. Its merchandise are additionally among the most energy-efficient ones on the market, which might save on long-term working prices.

With the huge spike in computing demand brought on by the substitute intelligence (AI) arms race, Supermicro is benefiting from the identical traits that despatched Nvidia inventory by way of the roof, although Supermicro’s journey has been a bit extra bumpy.

Supermicro isn’t firing on all cylinders proper now

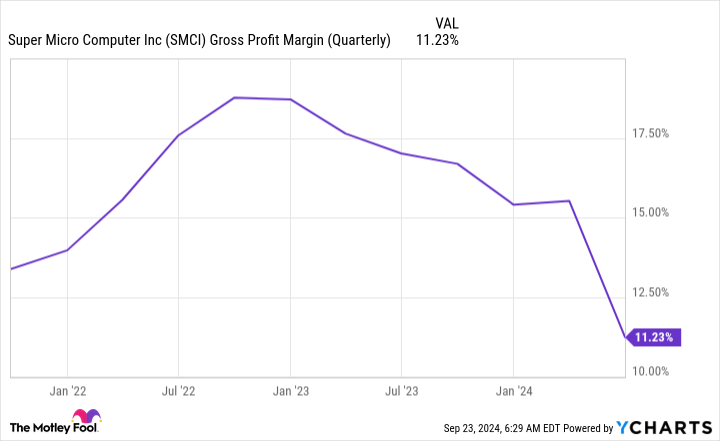

Together with Supermicro’s 10-for-1 stock-split announcement on Aug. 6, the corporate launched its fiscal 2024 fourth-quarter and full-year outcomes for the interval ended June 30. Whereas the corporate delivered robust income progress of 143% 12 months over 12 months and supplied wonderful full-year 2025 steerage of 74% to 101% progress, there have been some issues with its profitability.

Due to its new liquid-cooling product line getting spun up, Supermicro’s gross margin has taken a success.

This has brought about vital concern amongst some buyers as falling gross margin also can point out elevated competitors. Nonetheless, administration believes its gross margin will recuperate all through fiscal 2025.

In the meantime, short-selling agency Hindenburg Analysis launched a report on Supermicro on Aug. 27 alleging accounting manipulation. The SEC has fined Supermicro for accounting points up to now. On the identical time, as a result of Hindenburg is a short-seller, it advantages when the shares it experiences on fall, so buyers ought to proceed cautiously with this data. Supermicro responded that the quick report “comprises false or inaccurate statements.”

On Aug. 28, Supermicro delayed submitting its end-of-year Type 10-Okay with the SEC, saying it wanted extra time to “full its evaluation of the design and working effectiveness of its inner controls over monetary reporting.”

After the delay, Supermicro obtained a letter of non-compliance from the Nasdaq change, stating it’s in violation of itemizing guidelines as a result of it hasn’t filed its 10-Okay in a well timed vogue. After receiving the letter on Sept. 16, Supermicro has 60 days to conform or danger being delisted.

To additional complicate issues, on Sept. 26, The Wall Road Journal reported that unnamed sources had stated the Division of Justice had launched a probe into the corporate. If the reporting is right, that is only a preliminary probe, so nothing might come out of it. Nonetheless, there may very well be actual points with the corporate, which considerably will increase the chance of investing within the inventory. It can probably be a very long time earlier than the general public will get full particulars, so buyers might want to keep affected person with the inventory in the event that they select to purchase it.

Clearly, the corporate is grappling with severe points proper now, and the inventory has fallen over 60% from its 52-week excessive. Nonetheless, the enterprise case for its parts and servers is plain.

The present inventory can be valued pretty cheaply on a ahead earnings foundation.

If Supermicro can enhance its gross margin over the subsequent 12 months and dispel considerations over its accounting practices, the inventory has a ton of upside.

as a result of I consider within the firm. Nonetheless, I stored the place dimension low (round 1% of my complete portfolio worth). That manner, it will not have an effect on the portfolio an excessive amount of if the inventory tumbles additional, however I can nonetheless profit if Supermicro levels a restoration like some on Wall Road assume it could actually within the close to time period. I used to be planning on shopping for extra, however after the report of a possible DOJ probe, I am comfy with the present place dimension, because it represents the excessive danger, excessive reward related to Tremendous Micro Laptop’s inventory.

Must you make investments $1,000 in Tremendous Micro Laptop proper now?

Before you purchase inventory in Tremendous Micro Laptop, think about this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they consider are the for buyers to purchase now… and Tremendous Micro Laptop wasn’t certainly one of them. The ten shares that made the minimize may produce monster returns within the coming years.

Think about when Nvidia made this checklist on April 15, 2005… in the event you invested $1,000 on the time of our suggestion, you’d have $760,130!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has positions in Tremendous Micro Laptop. The Motley Idiot has positions in and recommends Nvidia. The Motley Idiot has a .

was initially revealed by The Motley Idiot

By Abigail Summerville

NEW YORK (Reuters) – Morgan Stanley’s middle-market buyout arm is exploring a sale of Sila Companies that might worth the residential companies firm at about $1.5 billion, together with debt, individuals acquainted with the matter mentioned on Friday.

King Of Prussia, Pennsylvania-based Sila, which is a supplier of companies together with heating, air-conditioning, and plumbing, is working with funding financial institution William Blair on the sale course of, the sources mentioned, requesting anonymity because the matter is confidential.

Sila may command a valuation equal to about 15 occasions its 12-month earnings earlier than curiosity, taxes, depreciation and amortization of almost $100 million, the sources mentioned.

Morgan Stanley Capital Companions, which owns Sila, declined to remark. William Blair and Sila didn’t reply to requests for remark.

Based in 1989, Sila operates over 30 manufacturers that present companies together with residential heating, air flow, and air-con, electrical, and plumbing within the Northeast, Mid-Atlantic, and Midwest elements of the USA.

MSCP, which acquired Sila for an undisclosed quantity in 2021, focuses on buying mid-sized companies and is housed inside Morgan Stanley Funding Administration, which manages $1.5 trillion of belongings.

Non-public fairness companies have historically been prolific acquirers of companies within the residential companies business, due to their regular money flows and the chance to drive consolidation within the fragmented sector.

Normal Atlantic invested in Flint Group earlier this 12 months, whereas L Catterton acquired LTP House Companies Group in 2022. Residential companies agency The Wrench Group counts TSG Client Companions, Leonard Inexperienced & Companions, and Oak Hill Capital as buyers.

Markets

Cathie Wooden's Ark Make investments Dumps Palantir Shares Amidst S&P 500 Inclusion And Prolonged AI Alliance

Benzinga and Lusso’s Information LLC might earn fee or income on some objects by means of the hyperlinks beneath.

On Wednesday, the Cathie Wooden-led Ark Make investments made a notable transfer by promoting a good portion of its stake in Palantir Applied sciences Inc (NYSE:).

The Palantir Commerce: The ARK Innovation ETF (NYSE:) offloaded 62,809 shares of Palantir. The sale got here simply days after, changing American Airways Group, Inc. This inclusion may probably enhance Palantir’s inventory because it beneficial properties wider publicity to traders and as shares are amassed to be included in index funds that mirror the S&P 500. Regardless of the optimistic information, Ark Make investments determined to cut back its publicity to the corporate.

Don’t Miss:

Furthermore, the sale occurred on the identical day of its cope with APA Company. The deal, which builds on three years of collaboration, introduces new AI capabilities by means of Palantir’s Synthetic Intelligence Platform (AIP) software program. Regardless of these developments, Ark Make investments’s transfer suggests a strategic shift in its funding strategy in the direction of Palantir.

The worth of the commerce, based mostly on Palantir’s closing worth of $37.12 on the identical day, is roughly $2.33 million.

Trending: This billion-dollar fund has invested within the subsequent huge actual property increase, .

It is a paid commercial. Rigorously think about the funding aims, dangers, fees and bills of the Fundrise Flagship Fund earlier than investing. This and different info will be discovered within the. Learn them fastidiously earlier than investing.

Different Key Trades:

-

Ark Make investments’s ARK Genomic Revolution ETF (ARKG) offered shares of Veeva Techniques Inc (VEEV) and shares of Butterfly Community Inc (BFLY).

-

The ARK Autonomous Know-how & Robotics ETF (ARKQ) offered shares of Materialise NV (MTLS) and likewise shares of Vuzix Corp (VUZI).

-

The ARK Subsequent Technology Web ETF (ARKW) offered shares of Roku Inc (ROKU). The ARK Area Exploration & Innovation ETF (ARKX) purchased shares of Blade Air Mobility Inc (BLDE) and offered shares of Mynaric AG (MYNA).

Questioning in case your investments can get you to a $5,000,000 nest egg? Converse to a monetary advisor as we speak. matches you up with as much as three vetted monetary advisors who serve your space, and you may interview your advisor matches for gratis to determine which one is best for you.

Preserve Studying:

-

Fractional actual property is the following huge alternative for constructing passive revenue —.

-

With returns as excessive as 300%, it’s no surprise this asset is the funding selection of many billionaires..

This text initially appeared on

Is Inventory-Break up Inventory Tremendous Micro Laptop Headed to $729 per Share?

Morgan Stanley's personal fairness arm explores sale of HVAC agency Sila, sources say

Cathie Wooden's Ark Make investments Dumps Palantir Shares Amidst S&P 500 Inclusion And Prolonged AI Alliance

Fed chair Powell speech, Chicago PMI in focus Monday

Why Nio Inventory Surged Extra Than 20% This Week

Report Galapagos debt-for-nature swap scrutinized over transparency irregularities claims

Clock is ticking for US recession, return of Fed's QE, says black swan fund

Apple should face narrowed privateness lawsuit over its apps

New PCE studying helps case for smaller Fed price lower in November

Alibaba, Eli Lilly lead Friday's morning market cap inventory movers

Inventory market at the moment: Shares acquire as Fed's favored inflation gauge cools

ITA expects greater full-year income because it prepares to affix Lufthansa group

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoDown 30% From Its All-Time Excessive, Ought to You Purchase Synthetic Intelligence (AI) Famous person Tremendous Micro Pc?

-

Markets3 months ago

Markets3 months agoADP Stories Decrease-Than-Anticipated Personal Payroll Progress for June

-

Markets3 months ago

Markets3 months agoSorry, however retiring ‘comfortably’ on $100K is a fantasy for most individuals. Right here’s why.

-

Markets3 months ago

Markets3 months agoAbove Food Corp. (NASDAQ: ABVE) and Chewy Inc. (NYSE: CHWY) Making Headlines This Week

-

Markets3 months ago

Markets3 months agoSouthwest Air adopts 'poison tablet' as activist investor Elliott takes important stake in firm

-

Markets3 months ago

Markets3 months agoCore Scientific so as to add 15 EH/s by means of Block’s 3nm Bitcoin mining ASICs

-

Markets3 months ago

Markets3 months agoWarren Buffett is popping 94 subsequent month. Ought to Berkshire traders begin to fear?

-

Markets3 months ago

Markets3 months agoWhy Rivian Inventory Roared Forward 10% on Friday

-

Markets3 months ago

Markets3 months agoArgentina to Promote {Dollars} In Parallel FX Market, Caputo Says

-

Markets3 months ago

Markets3 months agoWhy Intel Inventory Popped on Friday