Markets

1 Extremely-Excessive-Yield Healthcare Inventory to Purchase Hand Over Fist and 1 to Keep away from

Firms with excessive dividend yields can appear engaging, however there’s much more to revenue shares than above-average yields. Any company’s payouts are in peril with no strong enterprise backing it up. That is why choosing the proper dividend inventory requires trying past the yield and into the corporate’s fundamentals.

Let’s illustrate that with two examples: Pfizer (NYSE: PFE), and Medical Properties Belief (NYSE: MPW). Whereas each have engaging yields, the previous is a worthy funding, however the latter, not a lot. This is why.

The high-yield inventory to purchase: Pfizer

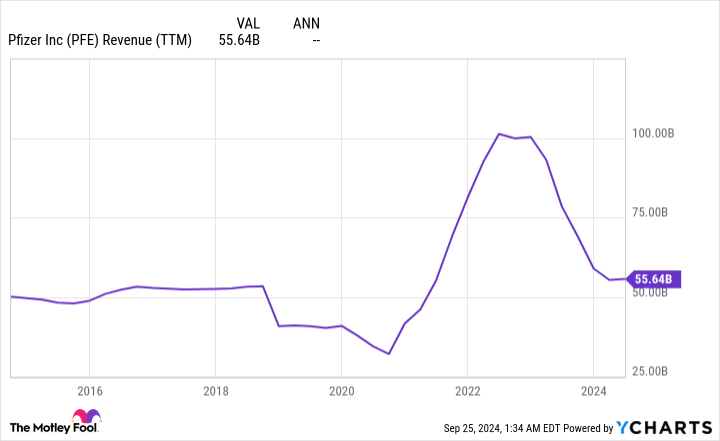

The drugmaker’s inventory is not in style in the marketplace proper now, with shares considerably lagging the market over the previous two years. Within the meantime, the inventory’s rose, and as of this writing, it stands at 5.7%. Regardless of Pfizer’s points, the corporate can keep its dividend program.

To be truthful, Pfizer’s monetary outcomes are comparatively poor in comparison with what it delivered in 2021 and 2022 — two years throughout which its gross sales skyrocketed because of its work within the coronavirus space. But, its prime line inflected properly above pre-pandemic ranges, a really encouraging signal that factors to secular development within the enterprise.

Pfizer’s COVID-19 medicine will finally cease affecting its outcomes as a lot. Furthermore, there isn’t any letup within the firm’s analysis & growth bills (that are far larger than pre-pandemic ranges) that noticed working and internet revenue drop under pre-COVID ranges.

And so there’s a robust chance that an entire lot of merchandise are within the pipeline, which ought to assist the corporate return to worthwhile development. Presently, Pfizer’s pipeline has over 100 applications. However two areas the place the corporate is focusing its analysis efforts, and price a particular point out, are within the weight reduction house and oncology.

The profitable GLP-1 weight reduction area is rising quickly. Pfizer’s candidate, oral danuglipron, .

Then, there are the corporate’s efforts in oncology. Pfizer acquired Seagen, an oncology specialist, for $43 billion. CEO Albert Bourla mentioned of the acquisition: “We’re not shopping for the golden eggs. We’re buying the goose that’s laying the golden eggs.” Seagen had a number of authorised most cancers medicine and a deep pipeline, however it was a a lot smaller firm than Pfizer, with much less funding and smaller footprints within the business. Now that they’re a single entity, Pfizer ought to grow to be a way more distinguished participant in oncology.

So, regardless of a poorer displaying during the last 12 months or so, the corporate’s underlying enterprise boasts glorious prospects. Pfizer’s dividend needs to be secure. It has elevated its payouts by 17% up to now 5 years. Pfizer is a dependable, high-yield dividend inventory to purchase and maintain.

The high-yield inventory to keep away from: Medical Properties Belief

Medical Properties Belief (MPT), a healthcare-focused actual property funding belief (REIT), has been bruised and battered since early 2023. The corporate’s income, earnings, and share value have all moved within the flawed course.

Not like in Pfizer’s case, this is not as a result of MPT was falling from unimaginable heights. This is the rationale. Steward Healthcare, one in all its essential tenants, had hassle maintaining with hire funds. Steward formally filed for chapter in Might.

Because of this concern, MPT had no selection however to slash its dividends. It has accomplished it twice since mid-2023. MPT’s yield stays spectacular at 5.56%. Nonetheless, dividend seekers detest payout cuts, so MPT won’t be the best choice proper now.

Some will object that the corporate seems to be on the verge of placing its Steward-related issues within the rearview mirror. True sufficient. MPT just lately reached agreements to place new tenants in 15 of the 23 hospitals beforehand operated by Steward Healthcare. The typical time period of the lease is about 18 years.

However as per the settlement, these new tenants will not begin paying hire till the primary quarter of 2025, and even then, they may solely pay half of the contractual settlement by the top of subsequent 12 months. They are going to steadily ramp issues up till they attain the full quantity in fourth-quarter 2026.

It is a win for MPT: It removes its troubled tenant and replaces it with 4 new ones (extra diversification), which (until monetary issues additionally come up with them) can pay common and predictable quantities till no less than 2042 on common. Nevertheless, MPT nonetheless has work to do in fixing its enterprise. It has but to seek out options for a few of Steward’s former amenities, together with some hospitals underneath building.

Even when it had, given the problems it has confronted recently, I might advocate staying away from the inventory, no less than for now. Sure, MPT is enhancing its enterprise, however it’s finest to observe how issues unfold from the sidelines till it may well show that it’s formally again by delivering constantly good outcomes.

Must you make investments $1,000 in Pfizer proper now?

Before you purchase inventory in Pfizer, think about this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they imagine are the for traders to purchase now… and Pfizer wasn’t one in all them. The ten shares that made the reduce might produce monster returns within the coming years.

Contemplate when Nvidia made this listing on April 15, 2005… should you invested $1,000 on the time of our advice, you’d have $740,704!*

Inventory Advisor gives traders with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Pfizer. The Motley Idiot has a .

was initially printed by The Motley Idiot

Markets

Micron earnings preview: Wall Avenue will get a glimpse into what's forward for US chipmakers

Micron () is the primary chipmaker to report quarterly outcomes this earnings season. Its report, scheduled for launch after the bell on Wednesday, will present perception into how the semiconductor sector is faring amid excessive expectations from Wall Avenue.

Micron’s reminiscence chip enterprise has undergone a resurgence over the previous 12 months as Large Tech companies pour billions into the semiconductor sector for {hardware} to energy synthetic intelligence knowledge facilities.

Micron distinguishes itself by partnering with, fairly than competing in opposition to, business superpower Nvidia (). Micron provides reminiscence chips for Nvidia’s hotly demanded GPUs.

Wall Avenue expects Micron to document quarterly revenues 90% greater than final 12 months — and that’s after analysts barely lowered their expectations by 0.3% from a month in the past. Right here’s a breakdown of analysts’ forecasts, in response to Lusso’s Information consensus estimates:

-

Income: $7.66 billion (Micron’s steering: $7.4 billion to $7.8 billion) vs. $4.01 billion in This autumn 2023

-

Adjusted earnings per share: $1.11 (Micron’s steering: $1 to $1.16) vs. a lack of $1.07 in This autumn 2023

Shares of the chipmaker rose as a lot as 2% in Wednesday buying and selling.

Buyers have staggeringly excessive and ever-increasing requirements for AI chipmakers, leaving them usually disenchanted in latest months. Micron’s third quarter earnings beat did little to sway buyers in late June.

As an alternative, on account of its fourth quarter outlook, which got here proper according to (fairly than beating) Wall Avenue’s expectations. after reporting quarterly earnings on the finish of August. Regardless of greater than doubling earnings and beating gross sales forecasts, buyers needed extra from the semiconductor superpower. Nvidia has since rebounded, however Micron inventory is down over 30% from three months in the past.

Almost 93% of Wall Avenue analysts overlaying Micron suggest shopping for the inventory. On common, they see its shares rising greater than 50% over the subsequent 12 months to $143.94. Nonetheless, their opinions of Micron are blended.

Morgan Stanley’s Joseph Moore thinks Wall Avenue’s softer expectations might assist enhance the inventory post-earnings. “MU inventory might rebound on earnings given a low bar close to time period, significantly if enthusiasm returns to AI beneficiaries,” he wrote in a observe to buyers earlier this week. However Moore maintained his Equal Weight ranking of Micron and sees the inventory as “basically costly.”

JPMorgan, however, maintained its Obese ranking of the inventory and mentioned it “continues to be one among our prime picks in semis subsequent 12 months.”

The PHLX Semiconductor Sector Index () has begun to get well from a dip originally of the month as tech shares rallied following the US and . The index is up almost 6% during the last week. Micron has been a part of that development, rising virtually 10% over that time-frame.

The corporate can be set to learn from that will loosen environmental necessities for microchip initiatives funded by the CHIPS and Science Act. Micron is one among , and the Constructing Chips in America Act handed by the US Home of Representatives Monday would enable the corporate quicker entry to greater than $6 billion in federal subsidies for its .

Laura Bratton is a reporter for Lusso’s Information.

By Katie Paul

MENLO PARK, California (Reuters) -Meta Platforms expanded its guess on synthetic intelligence, asserting a raft of recent product choices for its ChatGPT-like chatbot and plans to start out robotically injecting personalised pictures created by the bot into individuals’s Fb (NASDAQ:) and Instagram feeds, because it kicked off its annual Join convention at its California headquarters on Wednesday.

The Fb proprietor additionally introduced a brand new entry-level model of its Quest line of mixed-reality headsets, the Quest 3S, and is predicted to preview its first augmented-reality glasses and announce updates to its present virtual-reality and artificial-intelligence merchandise.

Among the many AI updates introduced was an audio improve to the digital assistant, referred to as Meta AI, which is able to now reply to voice instructions and supply customers the choice to make the assistant sound like celebrities together with Judi Dench and John Cena.

“I feel that voice goes to be a far more pure approach of interacting with AI than textual content,” CEO Mark Zuckerberg stated.

The corporate stated greater than 400 million individuals are utilizing Meta AI month-to-month, together with 185 million who’re returning to it weekly.

Consistent with its technique of sharing the AI fashions powering its digital agent totally free use by others, Meta launched three new variations of its Llama 3 fashions. Two of the fashions are multimodal, that means they’ll perceive each pictures and textual content, whereas the third is a fundamental text-only mannequin able to operating totally on a consumer’s system, a key privateness benefit.

The augmented-reality reveal is a very long time within the making for Zuckerberg, who positioned AR know-how as a kind of magnum opus when he first pivoted the world’s greatest social media firm towards constructing immersive “metaverse” programs in 2021.

Nevertheless, Meta has struggled to beat technical challenges with its AR mission since then, prompting the top of the corporate’s metaverse-oriented Actuality Labs division to acknowledge final yr {that a} product it may viably carry to market was “nonetheless a couple of years away – a couple of, to place it frivolously.”

The corporate has been plowing tens of billions of {dollars} into its investments in synthetic intelligence, augmented actuality and different metaverse applied sciences, driving up its capital expense forecast for 2024 to a file excessive of between $37 billion and $40 billion.

Its metaverse unit Actuality Labs misplaced $8.3 billion within the first half of this yr, in accordance with the latest disclosures. It misplaced $16 billion final yr.

The social media big is planning for the primary technology of the AR glasses this yr to be distributed solely internally and to a choose group of builders, with every system costing tens of 1000’s of {dollars} to provide, in accordance with a supply aware of the mission.

Meta goals to ship its first industrial AR glasses to shoppers in 2027, by which level technical breakthroughs ought to carry down the price of manufacturing, the supply stated.

The supply spoke on situation of anonymity as a result of they weren’t licensed to debate firm plans.

Zuckerberg appeared to substantiate that method, describing the AR work and telling an viewers at a dwell taping of the Acquired podcast in San Francisco that Meta was “fairly near with the ability to exhibit the primary prototype that we have now of that.”

Meta didn’t instantly reply to a request for touch upon the plans.

Within the meantime, Meta has leaned in to an surprising interim success on the street to AR with its camera-equipped Ray-Ban Meta good glasses.

Using a wave of pleasure round rising generative AI know-how, the corporate introduced finally yr’s Join convention that it was including an AI-powered digital assistant to the glasses, turning a once-forgotten system into the preferred AI wearable in the marketplace.

Though Meta has not disclosed gross sales numbers for the good glasses, the CEO of Ray-Ban maker EssilorLuxottica stated this summer time that extra of the brand new technology bought in a couple of months than the previous ones did in two years. Market analysis agency IDC estimates that greater than 700,000 pairs of the glasses have shipped for the reason that replace final yr.

Meta just lately prolonged its partnership with EssilorLuxottica and contemplated a potential funding within the eyewear firm, prompting hypothesis that the AR glasses may additionally bear the Ray-Ban identify. Extra instantly, Meta’s street map for the good glasses contains plans for a subsequent technology that may function a viewfinder able to displaying fundamental textual content and pictures via the lenses.

It has been transport software program updates this yr enhancing the AI assistant’s capabilities on the present glasses, together with an replace in April that enabled the agent to determine and converse about objects seen by the wearer.

Set to hit cabinets on Oct. 15, the Quest 3S headset might be supplied in two storage capability sizes, the smaller one priced at $299.99 and the opposite at $399.99.

With the launch, the corporate is discontinuing its older Quest 2 and high-end Quest Professional units, whereas additionally dropping the worth of the extra highly effective Quest 3 it launched final yr from $649.99 to $499.99.

Markets

Warren Buffett Wager $1M He May Outperform Hedge Funds Over A Decade. He Did It With A Technique Requiring No Investing Talent

Again in 2007, Warren Buffett made a daring transfer. The legendary investor guess $1 million {that a} easy, no-frills S&P 500 index fund may beat a collection of hand-picked hedge funds over 10 years. Consultants handle the hedge funds, and for that, they cost a layer of charges. Many see them as the head of refined investing.

Do not Miss:

Nonetheless, Buffett believed that one thing as , which merely tracks the efficiency of the highest 500 corporations within the U.S., would do higher in the long term.

What was the end result? Buffett comfortably received the wager. Over the last decade, the Vanguard S&P 500 Index Fund, which he chosen, yielded an astounding 125.8% return, whereas the returns made by the hedge funds diversified from 2.8% to 87.7%. Nonetheless, how may this “odd” funding method surpass a few of the most completed monetary minds?

Trending: Industrial actual property has traditionally outperformed the inventory market, and

Warren Buffett has argued that low-cost index funds are a smart funding choice for most individuals for a few years. An index fund permits buyers to personal a portion of every firm within the index as an alternative of making an attempt to time the market or establish the following huge inventory.

It’s a indifferent technique that merely replicates the market’s general efficiency. As Buffett stated, “You do not have to do this, you simply have to take a seat again and let American trade do its job for you.”

This would possibly sound too easy to be efficient, particularly in comparison with the advanced methods employed by hedge funds. Nonetheless, Buffett has all the time stated holding prices low is essential to profitable investing. round 2% of your cash yearly, plus 20% of any earnings they make. These excessive charges can lower into your earnings over time.

Trending: Rory McIlroy’s mansion in Florida is value $22 million at this time, doubling from 2017 —

In distinction, the Vanguard fund Buffett selected had an expense ratio of simply 0.04%, that means virtually the entire funding’s progress stayed within the investor’s pocket. “Charges matter in investing, little doubt about it,” stated Ted Seides, the hedge fund supervisor who accepted Buffett’s guess. He later admitted that Buffett was proper concerning the impression of excessive charges.

Regardless of the clear benefits of low-cost index funds, many rich people and enormous establishments proceed to hunt out costlier funding methods. Buffett defined this phenomenon by , “No guide on the planet will inform you simply purchase an S&P index fund and sit for the following 50 years. You aren’t getting to be a guide and definitely do not get an annual charge that manner.”

Learn Subsequent:

Up Subsequent: Remodel your buying and selling with Benzinga Edge’s one-of-a-kind market commerce concepts and instruments. that may set you forward in at this time’s aggressive market.

Get the newest inventory evaluation from Benzinga?

This text initially appeared on

© 2024 Benzinga.com. Benzinga doesn’t present funding recommendation. All rights reserved.

Micron earnings preview: Wall Avenue will get a glimpse into what's forward for US chipmakers

Meta bulks up AI choices, together with chatbot, at Join occasion

Warren Buffett Wager $1M He May Outperform Hedge Funds Over A Decade. He Did It With A Technique Requiring No Investing Talent

Renn Fund president and CEO buys shares price $2,583

1 Extremely-Excessive-Yield Healthcare Inventory to Purchase Hand Over Fist and 1 to Keep away from

Poland shares greater at shut of commerce; WIG30 up 0.78%

Inventory market at this time: Shares combined as buyers hold watchful eye on economic system

Southwest plans to scale back service and staffing in Atlanta, union says

New House Gross sales Decline in August, But Yr-Over-Yr Progress Stays Robust

Costco earnings preview: One other quarter of gross sales progress anticipated after membership charge hike

Earnings name: AutoZone studies strong development amid market challenges

Why This Inventory Might Be the Nvidia of Healthcare

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoHungary central financial institution tells lenders to reimburse purchasers after Apple glitch

-

Markets3 months ago

Markets3 months agoDown 30% From Its All-Time Excessive, Ought to You Purchase Synthetic Intelligence (AI) Famous person Tremendous Micro Pc?

-

Markets3 months ago

Markets3 months agoIf You'd Invested $1,000 in Starbucks Inventory 20 Years In the past, Right here's How A lot You'd Have Immediately

-

Markets3 months ago

Markets3 months agoPrediction: This Transfer From Nvidia within the Second Half Will Be A lot Greater Than the Inventory Break up

-

Markets3 months ago

Markets3 months agoADP Stories Decrease-Than-Anticipated Personal Payroll Progress for June

-

Markets3 months ago

Markets3 months agoSorry, however retiring ‘comfortably’ on $100K is a fantasy for most individuals. Right here’s why.

-

Markets3 months ago

Markets3 months agoAbove Food Corp. (NASDAQ: ABVE) and Chewy Inc. (NYSE: CHWY) Making Headlines This Week

-

Markets3 months ago

Markets3 months agoSouthwest Air adopts 'poison tablet' as activist investor Elliott takes important stake in firm

-

Markets2 months ago

Markets2 months agoWarren Buffett is popping 94 subsequent month. Ought to Berkshire traders begin to fear?

-

Markets3 months ago

Markets3 months agoCore Scientific so as to add 15 EH/s by means of Block’s 3nm Bitcoin mining ASICs