Markets

2 Disruptor Shares to Purchase and Maintain for Nice Lengthy-Time period Potential

There are industries that come and go in the case of investor fancy. The one factor that seems timeless is the attraction of disruptors. Discover a firm shaking up a stodgy trade, and there is cash to be made in the event you’re proper and, ideally, early.

A number of the disruptors I believe supply long-term potential embody Chipotle Mexican Grill (NYSE: CMG) and Teladoc Well being (NYSE: TDOC). Let’s take a more in-depth have a look at each of those corporations that reinvented their stodgy industries. There’s nonetheless upside available at immediately’s worth factors for solely totally different causes.

1. Chipotle Mexican Grill

There was a time when there was virtually nothing between quick meals and informal eating to fulfill the hungry. Chipotle championed fast-casual, a format that delivered informal eating eats with the comfort of quick meals. Positive, chains together with Subway and Panda Specific had the meeting line idea down earlier than Chipotle. Others like Panera take somewhat extra time on the prep however nonetheless put out table-service-quality eats. Chipotle is the one which put all of it along with a “meals with integrity” mantra that resonates with its rising fan base.

Chipotle is big now. There are actually 3,479 places, however Chipotle expects to greater than double that retailer depend in North America alone. It is also not afraid to proceed innovating. When it noticed digital gross sales take off on this aspect of the pandemic disaster it made it simpler to make the most of a second meeting line behind the restaurant to piece collectively the rising variety of takeout orders with out inconveniencing walk-in visitors like different ideas are doing. Drive-thru lanes have been round within the restaurant trade because the Nineteen Forties, however Chipotle is now incorporating its cleverly titled Chipotlanes to most of its new openings to make it simpler for patrons and third-party supply app drivers to get their meals.

As large as Chipotle has grown through the years, it retains discovering methods to ship stellar returns. The inventory is up 57% over the previous yr, and has greater than quadrupled during the last 5 years. Double-digit income positive aspects proceed, together with three consecutive quarters of . Growth stacked on prime of wholesome comps can hold these positive aspects coming. The story will get even higher on the underside line with no less than 36% development in earnings for every of the final three years.

Chipotle has tried and did not develop out sister ideas, however actuality has proven that it would not want a second act. The namesake chain is all it wants. Chipotle surprised the market with its success, and the imitators have adopted. Do not let this week’s upcoming 50-for-1 inventory break up distract you. It is a top-shelf and disruptor that continues to lift the bar-bacoa.

2. Teladoc

Let’s go from a disruptor that everybody loves in Chipotle to 1 that buyers are steering away from: Teladoc. The pioneer of telehealth has a confirmed platform the place of us can verify in with a medical specialist on-line for a rising variety of considerations and situations. It is simply struggling to attach with sufferers and the market proper now.

The inventory hit one other eight-year low late final week. The shares are actually down a surprising 97% since peaking in early 2021. Put one other manner, this may be a 30-bagger if it obtained even near its earlier all-time excessive.

The excellent news is that Teladoc has a wholesome 91.8 million digital care members on its platform. That is about it for the excellent news. Income development has decelerated sharply for 12 consecutive quarters, a run that started following a 151% year-over-year improve on the highest line and has fallen all the best way to a 3% uptick in its newest report.

Utilization goes the improper manner. 12 months-over-year visits have declined the previous few quarters regardless of the gradual rise in its membership base. Losses proceed, however it’s producing constructive and rising free money move and adjusted earnings earlier than curiosity, taxes, depreciation, and amortization (EBITDA).

There isn’t a denying that this can be a dangerous scenario. Regardless that Teladoc’s stability sheet is flush with money to journey issues out within the close to time period, it wants to begin rising once more. Telemedicine and telehealth make an excessive amount of sense to fail, and newer corporations are gaining market share at Teladoc’s expense. A saving grace right here may very well be a change on the prime. Its longtime CEO stepped down in April, and an outsider was introduced in to take over earlier this month. The present prognosis might not be encouraging, however with the suppressed share worth and enormous membership base, the upside is excessive whether or not Teladoc figures issues out or is acquired by an opportunistic participant at an affordable premium.

Must you make investments $1,000 in Chipotle Mexican Grill proper now?

Before you purchase inventory in Chipotle Mexican Grill, think about this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they consider are the for buyers to purchase now… and Chipotle Mexican Grill wasn’t one in every of them. The ten shares that made the lower may produce monster returns within the coming years.

Contemplate when Nvidia made this listing on April 15, 2005… in the event you invested $1,000 on the time of our suggestion, you’d have $775,568!*

Inventory Advisor gives buyers with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of June 24, 2024

has positions in Teladoc Well being. The Motley Idiot has positions in and recommends Chipotle Mexican Grill and Teladoc Well being. The Motley Idiot has a .

was initially revealed by The Motley Idiot

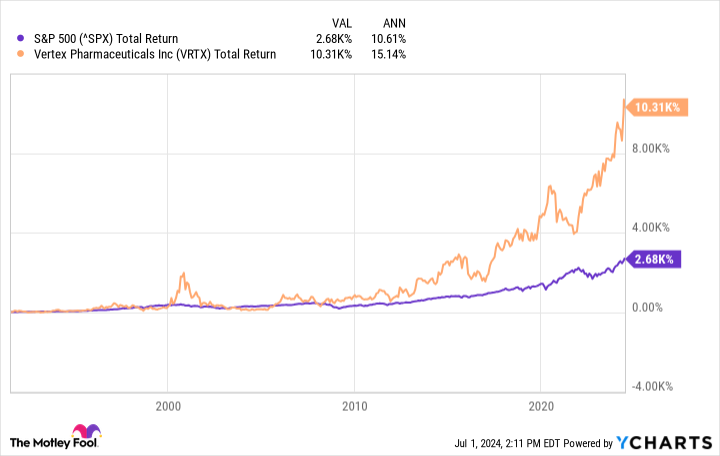

Investing in fairness markets is a dependable, wealth-growing technique. Previously 33 years, the S&P 500‘s common annual return is about 10.6%. It is laborious to discover a return significantly better than that elsewhere.

Some particular person shares have carried out even higher, although. Take Vertex Prescribed drugs (NASDAQ: VRTX), a number one biotech firm whose common annual return since its 1991 preliminary public providing (IPO) is 15.1%. The drugmaker has grown by 10,310%.

It’s a formidable efficiency, however Vertex nonetheless has loads of development forward of it, and the inventory seems to be like a strong buy-and-hold-forever choose. Right here is why.

information by

The key to Vertex’s success

About 7,000 uncommon ailments have an effect on between 25 million and 30 million People. Many do not have accredited therapies focusing on their underlying causes. So, it is not laborious for a to select a goal on this universe of unmet medical wants that might show extremely profitable. The laborious half is creating efficient medicines. That is Vertex’s primary (although not the one) focus. The corporate seeks to focus on the underlying causes of ailments for which there are few, if any, therapies.

Its work in cystic fibrosis (CF) prior to now couple of a long time is a tremendous success story. CF is a illness that impacts about 92,000 sufferers in North America, Europe, and Australia. It causes injury to inside organs. And till Vertex’s breakthroughs — its first CF product was formally accredited within the U.S. in 2012 — there weren’t any medicines that addressed the sickness on the genetic degree. Vertex has been handsomely rewarded for its progress on this discipline. Income and earnings have grown quickly.

information by

However that is prior to now. Can Vertex Prescribed drugs nonetheless carry out effectively transferring ahead?

Do not change a profitable components

Success in enterprise would not occur accidentally. Sure, there’s typically a component of luck. Nevertheless, companies that carry out persistently effectively for a very long time should have a imaginative and prescient and the power to execute a profitable technique. Vertex’s imaginative and prescient stays the identical. It’s nonetheless creating medicines for uncommon (and in addition not so uncommon) ailments. Previously, the biotech has confirmed that it could actually execute. Loads of its friends tried to develop competing CF therapies. , to this point.

Vertex is now proving itself outdoors of its core space. It lately earned approval for Casgevy, a gene-editing remedy for a few uncommon blood-related ailments. It’s advancing key packages via its pipeline. Inaxaplin, a possible remedy for APOL1-mediated kidney illness, is now within the section 3 portion of a section 2/3 examine.

Suzetrigine, an investigational drugs for acute and neuropathic ache, carried out effectively in a late-stage medical trial, the outcomes of which have been introduced earlier this yr. There are many ache medicines, however they typically carry burdensome unwanted side effects, so there’s nonetheless a necessity right here.

Vertex’s early-stage packages additionally look promising. The corporate is aiming to “treatment” kind 1 diabetes with VX-880. In an ongoing section 1/2 examine, three sufferers with no less than a yr of follow-up have achieved insulin independence. All folks with kind 1 diabetes (in contrast to the kind 2 selection) sometimes want insulin. These outcomes are spectacular though it is too early to rejoice. There’s extra occurring with Vertex Prescribed drugs.

Nevertheless, the necessary level is that this: Do not spend money on biotech due to particular medical packages. VX-880 would possibly show ineffective and so would possibly inaxaplin. Regardless of constructive section 3 outcomes, suzetrigine may encounter unexpected regulatory roadblocks. In any case, Vertex has confronted such medical or regulatory headwinds earlier than.

As an example, in October 2020, the biotech halted a section 2 examine for an in any other case promising candidate partly due to security considerations. The corporate’s shares dropped off a cliff in at some point consequently. Here is how the inventory has carried out since then.

information by

The lesson? Vertex’s prospects do not hinge on any single program. The corporate’s energy is its clear imaginative and prescient and technique and its tradition of innovation, which permits it to realize that imaginative and prescient. That is what makes Vertex Prescribed drugs inventory value holding onto without end.

Do you have to make investments $1,000 in Vertex Prescribed drugs proper now?

Before you purchase inventory in Vertex Prescribed drugs, think about this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they consider are the for traders to purchase now… and Vertex Prescribed drugs wasn’t one in every of them. The ten shares that made the minimize may produce monster returns within the coming years.

Take into account when Nvidia made this record on April 15, 2005… when you invested $1,000 on the time of our suggestion, you’d have $786,046!*

Inventory Advisor offers traders with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of July 2, 2024

has positions in Vertex Prescribed drugs. The Motley Idiot has positions in and recommends Vertex Prescribed drugs. The Motley Idiot has a .

was initially printed by The Motley Idiot

Financial institution of America reported a shift in world fund efficiency for June, with Worth funds experiencing a median decline of 0.88% in comparison with their benchmarks. Solely 24% of Worth funds managed to outperform in June.

Regardless of the setback, BofA acknowledges that Worth funds nonetheless maintain an edge year-to-date, with 52% outperforming their benchmarks. The median YTD return for outperforming Worth funds sits at 0.27%.

In distinction, BofA says Progress funds weathered June’s market actions barely higher. Practically half (49%) of Progress funds outperformed their benchmarks, with a median relative return of -0.04%. Nevertheless, Progress funds have not fared as effectively year-to-date, with solely 40% exceeding their benchmarks and a median YTD relative return of -0.84%.

BofA’s report additionally highlights attention-grabbing inventory picks inside every fund class. They determine corporations with sturdy “Triple Momentum” (optimistic momentum in earnings, worth, and information sentiment) which can be closely weighted by the respective funds. Amongst these, Progress funds favor NU, Icon (NASDAQ:) plc, On Holding, and TSMC, whereas Worth funds lean in direction of BJ’s Membership, US Meals, Ameriprise Monetary (NYSE:), and Hana Monetary.

The report concludes by noting the struggles of aggressive funds, these with a really excessive Lively Share Ratio. These funds are mentioned to have underperformed the market by a median of two.72% year-to-date and 0.62% in June alone. Conversely, funds carefully following the benchmark have carried out higher year-to-date.

Following the inventory picks of billionaire buyers might help you discover rewarding investments for the lengthy haul. These buyers sometimes conduct in-depth analysis on the businesses not out there to a small investor.

Chase Coleman of Tiger World Administration and Daniel Loeb of Third Level are two billionaire fund managers who’ve an extended file of safely rising their property. Listed here are two of their prime inventory holdings to purchase proper now.

1. Chase Coleman, Tiger World Administration: Nvidia

Chase Coleman based Tiger World Administration in 2001 and at this time has an estimated web price of over $5 billion, in line with Forbes. Tiger World has a powerful file of incomes market-beating returns for shoppers during the last twenty years, and one among its largest positions within the first quarter was Nvidia (NASDAQ: NVDA) — one of many best-performing S&P 500 shares in current months.

Enterprises are shopping for as many as they’ll get their palms on for coaching synthetic intelligence (AI) fashions. Meta Platforms plans to have 350,000 of Nvidia’s H100 chips in its laptop infrastructure by the top of the yr. These highly effective chips have been in brief provide resulting from excessive demand, and Nvidia expects this case to proceed.

The central processing models (CPUs) that powered knowledge facilities for years are being supplanted by extra highly effective GPUs, which is driving unprecedented progress for Nvidia’s knowledge heart enterprise. Nvidia has an extended historical past of delivering above-average progress and returns to shareholders, however its present progress is off the charts, with income leaping 262% yr over yr in the latest quarter.

The corporate will not proceed to see its income triple yearly, however buyers who can patiently maintain the inventory over the subsequent a number of years ought to see passable returns. Nvidia will proceed to innovate with new merchandise and AI options to drive long-term progress.

Earlier this yr, Nvidia introduced its new Blackwell computing platform that may permit the main cloud service suppliers to take knowledge processing to a different stage. It expects demand for Blackwell and the brand new H200 knowledge heart GPU to outstrip provide within the close to time period.

Nvidia expects its fiscal second-quarter income to be roughly $28 billion, representing a 107% year-over-year enhance. This stage of demand makes the inventory a no brainer funding.

2. Daniel Loeb, Third Level: Taiwan Semiconductor Manufacturing

Daniel Loeb is the founding father of Third Level and has an estimated web price of over $3 billion, in line with Forbes. With the rising demand for AI chips, it is no shock to see one other prime chip firm in a billionaire’s portfolio. Third Level held a large stake within the main chip producer Taiwan Semiconductor Manufacturing (NYSE: TSM) on the finish of the primary quarter.

Taiwan Semiconductor dominates the business with over 60% of the worldwide foundry market in 2023. As a foundry, it makes merchandise for different corporations. All of the main chip corporations, together with Nvidia, have relationships with TSMC, which places the corporate in a powerful aggressive place.

TSMC’s income grew 12.5% yr over yr within the first quarter in U.S. {dollars}, primarily pushed by demand for high-performance chips. However progress ought to speed up within the close to time period, as a few of the firm’s finish markets are nonetheless in restoration, together with smartphones, which account for 38% of TSMC’s enterprise.

Administration expects second-quarter income to come back in between $19.6 billion to $20.4 billion, or enhance by 27% yr over yr on the midpoint of steerage. TSMC is working to increase its manufacturing capability within the U.S., which displays a positive outlook for chip demand.

TSMC has an extended historical past of delivering excellent returns to shareholders, and its worthwhile enterprise mannequin fueled a rising dividend to shareholders since 2004. It is a comparatively protected inventory to trip the wave of AI chip demand over the subsequent decade.

Do you have to make investments $1,000 in Nvidia proper now?

Before you purchase inventory in Nvidia, think about this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they imagine are the for buyers to purchase now… and Nvidia wasn’t one among them. The ten shares that made the lower might produce monster returns within the coming years.

Take into account when Nvidia made this checklist on April 15, 2005… when you invested $1,000 on the time of our advice, you’d have $786,046!*

Inventory Advisor offers buyers with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of July 2, 2024

Randi Zuckerberg, a former director of market growth and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. has positions in Meta Platforms and Nvidia. The Motley Idiot has positions in and recommends Meta Platforms, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Idiot has a .

was initially revealed by The Motley Idiot

1 Inventory That Elevated 10,000% in 33 Years to Purchase and Maintain Endlessly

Globally, Worth funds gave again some efficiency in June

2 No-Brainer Billionaire-Owned Shares to Purchase Proper Now

World shares at report excessive, UK Labour landslide and US payrolls hog highlight

FoundationLogic Unveils Silent Residence Miner at Mining Disrupt 2024

The Tesla bulls experience once more: Morning Transient

Earnings season to check hopes for broader shares rally

2 Synthetic Intelligence Shares That May Make You a Millionaire

Earnings name: Sodexo reviews regular development in Q3, confirms full-year outlook

As Bitcoin Bellyflops to $54K Solely 5 Mining Rigs Stay Worthwhile, Says F2Pool

What’s Behind Tesla Inventory’s (NASDAQ:TSLA) Surge, And Is It Justified?

UK election reduction, tech rally pull European shares to over 1-week highs

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoUnitedHealth Group Demonstrates Resilience in Q1 2024 Financial Report

-

Markets3 months ago

Markets3 months agoUnderstanding a Flash Crash in the Stock Market

-

Markets3 months ago

Markets3 months agoA Glimpse Into the Buzz of Upcoming IPOs in April 2024

-

Markets3 months ago

Markets3 months agoWiSA Technologies Shares Surge After Strategic Licensing Agreement and Reverse Split

-

Markets2 months ago

Markets2 months agoThe Most Shorted Stocks as of Late March 2024

-

Markets1 month ago

Markets1 month agoTechnical Analysis of Tupperware Brands Corporation (TUP)

-

Markets1 month ago

Markets1 month agoPetco (NASDAQ: WOOF) Beats Q1 CY2024 Estimates: What Traders Should Know

-

Markets1 month ago

Markets1 month agoSnowflake Inc. (SNOW) Earnings Miss: What It Means for Traders

-

Markets1 month ago

Markets1 month agoMGO Global Inc. (NASDAQ: MGOL) Surges 446% on Strong First Quarter Earnings

-

Markets1 month ago

Markets1 month agoGreenwave Technology Solutions (NASDAQ: GWAV) Plummets 62% After Announcing Share Offering

-

Markets3 months ago

Markets3 months agoBoeing’s Proactive Measures Ahead of Whistleblower Hearing