Markets

3 No-Brainer Curiosity-Price-Delicate Dividend Shares to Purchase Proper Now for Much less Than $1,000

The S&P 500 index at present affords a scant 1.3% dividend yield. The typical utility is yielding about 2.9%, utilizing the Utilities Choose Sector SPDR Fund (NYSEMKT: XLU) as an business proxy. That is greater than twice what you’d get from the common S&P 500 inventory, and highlights why utilities are an excellent place to buy when on the lookout for dividend shares.

Loads of dividend shares on the market depend on borrowing as a part of their enterprise fashions and modifications in rates of interest have a direct impact on their operations. With the Federal Reserve decreasing the fed funds price final week (and strongly hinting that further cuts are coming), the rates of interest banks cost for borrowing are prone to drop over the subsequent 12 months or two. That ought to bode properly for this class of shares.

Listed below are three robust dividend-paying utility shares set to profit from the Fed’s actions that buyers will wish to take into account instantly.

1. NextEra is a dividend progress story

NextEra Vitality‘s (NYSE: NEE) dividend yield is 2.4%. That is truly beneath the utility common, which could discourage some buyers. That is why a better look is required. The massive story with NextEra is definitely dividend progress. Not solely has the corporate elevated its dividend yearly for 3 a long time, however the common annualized enhance over the previous 10 years was an enormous 10%! That features will increase over the previous one-, three-, and five-year intervals of 10%, suggesting this can be a dependable dividend progress inventory.

A ten% dividend progress price can be good for any firm. Half that price can be fairly robust for a utility. The driving pressure behind NextEra’s dividend progress is the combo of property it has in its portfolio. The muse is its regulated utility operation in Florida, a state that has lengthy benefited from inhabitants progress. On high of that, NextEra has constructed one of many world’s . The clear vitality funding has supplied a historic progress alternative, and it’ll proceed to supply the runway for future progress because the world continues its shift towards cleaner vitality options.

Decrease will make it simpler to afford the capital spending wanted to continue to grow its clear vitality footprint. If you’re a dividend progress investor, you may wish to reexamine NextEra Vitality now that the Fed’s price regime has shifted.

2. Dominion Vitality is engaged on a turnaround

Dominion Vitality (NYSE: D) hasn’t been rising its enterprise of late. It has been shrinking it. Its most up-to-date transfer was to promote three pure fuel utilities to Canada’s Enbridge. The money generated from that sale was put towards strengthening Dominion’s steadiness sheet.

Utilities personal property which might be costly to construct and keep however that, because of regulatory oversight (and monopolies within the areas they serve), have a tendency to supply dependable money flows. As such, utilities typically make heavy use of leverage. However, generally, the debt load can get a bit forward of an organization. Fixing that scenario is normally a gradual course of — except that’s, a utility like Dominion begins elevating money in another approach. Promoting property is an instance of a approach to rapidly cut back leverage.

With much less leverage as a important administration aim, nonetheless, Dominion is about to get an help from the Federal Reserve’s transfer to decrease charges. Within the grand scheme of issues, 50 foundation factors is not an enormous change on an absolute degree. However when you think about that the utility has $32.6 billion in debt on its steadiness sheet, each foundation level counts! The profit will present up first in revolving credit score amenities, however over time the corporate’s price for refinancing debt shall be decrease, too.

Dominion’s 4.6% dividend yield is properly above common for a utility, however that is as a result of it’s a little bit of a turnaround story. That stated, it’s a fairly low-risk inventory, and the turnaround effort simply acquired a bit simpler.

3. Black Hills is a Dividend King

With a market cap of $4.2 billion, Black Hills (NYSE: BKH) is a comparatively small utility firm. Nonetheless, it has an above-average 4.2% dividend yield. That yield is additional enticing provided that Black Hills has elevated its dividend each single 12 months for 54 consecutive years, making it a extremely elite Dividend King. There are only some different utilities that may make that declare, so in the event you care about dividend consistency, you may wish to have Black Hills in your shortlist.

Be aware, too, that the dividend has grown at a 5% annualized price over the previous decade. Positive, that is half the expansion price of NextEra Vitality’s dividend, nevertheless it’s nonetheless a really strong quantity for a gradual and regular dividend grower. The one wrinkle with Black Hills is that it tends to hold extra leverage than different utilities, which signifies that rising rates of interest are likely to hit the corporate a bit tougher — thus the higher-than-average yield. However that story modifications when charges are falling, as Black Hills could have a neater time on the curiosity expense entrance.

In contrast to Dominion, Black Hills just isn’t a turnaround story. It’s only a well-run utility persevering with to be well-run. Nonetheless, if that sounds good to you, you then would possibly wish to purchase it now. Falling rates of interest will solely make this (type of boring) utility inventory extra compelling.

Decrease charges are an excellent factor for utilities

NextEra Vitality, Dominion Vitality, and Black Hills aren’t the one utilities that can profit from falling rates of interest. However they signify three completely different funding paths to contemplate, from dividend progress to a turnaround to a gradual and regular dividend tortoise. The shift towards decrease charges ought to make all of them extra enticing investments.

Must you make investments $1,000 in Dominion Vitality proper now?

Before you purchase inventory in Dominion Vitality, take into account this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they imagine are the for buyers to purchase now… and Dominion Vitality wasn’t considered one of them. The ten shares that made the minimize may produce monster returns within the coming years.

Take into account when Nvidia made this listing on April 15, 2005… in the event you invested $1,000 on the time of our advice, you’d have $710,860!*

Inventory Advisor gives buyers with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 16, 2024

has positions in Black Hills, Dominion Vitality, and Enbridge. The Motley Idiot has positions in and recommends Enbridge and NextEra Vitality. The Motley Idiot recommends Dominion Vitality. The Motley Idiot has a .

was initially printed by The Motley Idiot

Markets

Prediction: This Main Synthetic Intelligence (AI) Inventory May Compete With Nvidia within the Not-Too-Distant Future

What occurs when an organization’s largest prospects develop into fierce rivals? Think about that you simply personal the biggest chocolate chip firm within the land. You promote to all the biggest grocery chains as a result of you will have the most effective recipe. However each day, these shops pour cash into discovering the next-best recipe. In the event that they create it, it might be a recipe for catastrophe (pardon the pun).

That is Nvidia‘s actuality now. Firms like Microsoft, Alphabet (NASDAQ: GOOG)(NASDAQ: GOOGL), Meta Platforms, and Amazon are spending billions on Nvidia GPUs whereas additionally spending billions creating competing merchandise. The important thing for Nvidia is to remain one step forward. Nevertheless it will not be simple with such deep-pocketed rivals.

Alphabet is severe competitors

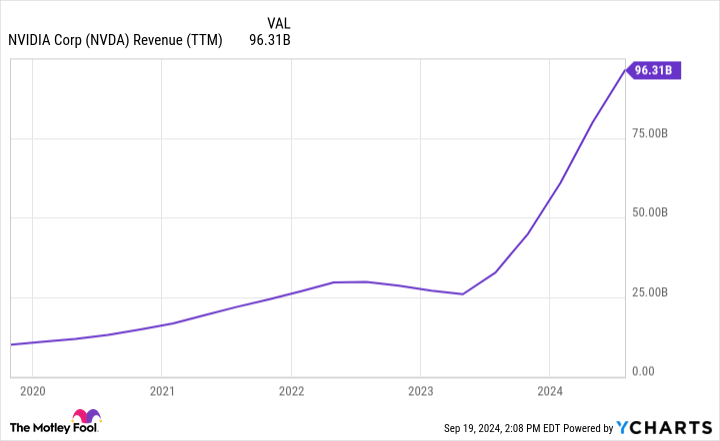

As proven under, the 4 huge tech firms talked about above reportedly account for practically 40% of Nvidia’s income, which exploded to $96 billion over the previous 12 months.

Of this, 85% comes from Nvidia’s information middle division. No matter firm can encroach on Nvidia’s huge market share of reportedly 70% to 95% in synthetic intelligence (AI) chips will profit in two methods: elevated revenue and decreased bills. In spite of everything, a lot of that enormous ramp in Nvidia’s income, depicted above, comes from different large tech firms’ pockets.

Nvidia is main resulting from its groundbreaking H100 GPU, which delivers unparalleled efficiency. These items are crucial for information facilities, giant language fashions, and generative AI, so Nvidia cannot sustain with demand and the margins are gigantic.

Alphabet is creating and bettering its competing AI product, the Tensor Processing Unit (TPU). It launched the sixth-generation TPU, Trillium, earlier this yr. With 5 instances extra velocity and 67% extra vitality effectivity, sixth-gen Trillium is a substantial leap over model 5.

Trillium would not compete straight on the open market with Nvidia. As a substitute, prospects lease house on Google Cloud, permitting Alphabet a broader buyer base. The power to lease house shall be intense competitors for Nvidia as firms can select to lease fairly than make capital investments. And, after all, Alphabet makes use of it internally.

Is Alphabet inventory a purchase now?

Alphabet can pour capital into AI initiatives as a result of it’s massively worthwhile and generates huge money circulation from its core promoting (Google Search and YouTube) and Google Cloud segments. These segments generated $84 billion in gross sales final quarter, a 14% year-over-year enhance that got here with $27 billion in working money circulation.

Additionally spectacular is that the working margin for Google Cloud elevated from 5% to 11% yr over yr. The rise in margin is a transparent indication of elevated effectivity and rising demand. As you possibly can see under, Google Cloud’s progress has been outstanding lately.

Even after rising practically fourfold since 2020, AI will enhance Google Cloud’s gross sales. For Alphabet, investments in AI, Google Cloud, and generative chatbots that rival ChatGPT, like Gemini, are essential to the long-term path.

Microsoft Bing is difficult Google Search by harnessing ChatGPT by its billion-dollar funding in its creator, OpenAI. Plus, generative AI could encroach on the search market. Nonetheless, there isn’t any have to sound an alarm but; Google Search grew 14% final quarter to $49 billion in income and stays far and away the market chief.

Alphabet inventory appears to be like like a cut price in a market the place many tech shares are buying and selling nicely above historic valuations. As proven under, Microsoft trades 14% above its five-year common price-to-earnings (P/E) ratio, whereas Alphabet trades 12% under.

The historic undervaluation, high quality core enterprise, and potential to compete for a part of Nvidia’s market dominance make Alphabet inventory an clever purchase for tech buyers and people searching for firms.

Do you have to make investments $1,000 in Alphabet proper now?

Before you purchase inventory in Alphabet, contemplate this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they consider are the for buyers to purchase now… and Alphabet wasn’t certainly one of them. The ten shares that made the reduce might produce monster returns within the coming years.

Contemplate when Nvidia made this record on April 15, 2005… should you invested $1,000 on the time of our advice, you’d have $710,860!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 16, 2024

John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Suzanne Frey, an govt at Alphabet, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, a former director of market growth and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. has positions in Amazon. The Motley Idiot has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and brief January 2026 $405 calls on Microsoft. The Motley Idiot has a .

was initially revealed by The Motley Idiot

In a latest transaction, Robert S. Ellin, the Govt Chairman of PodcastOne, Inc. (NASDAQ:PODC), acquired extra shares of the corporate’s inventory, signaling a vote of confidence within the podcast community’s future. The acquisition, which befell on September 20, 2024, concerned 17,000 shares at a mean value of $1.893.

The transaction was a part of a sequence of purchases made at costs starting from $1.85 to $1.93, as detailed within the footnotes of the submitting. Following this purchase, Ellin’s direct possession in PodcastOne has elevated to a complete of 125,563 shares.

Traders usually monitor insider transactions resembling these for insights into government views on the corporate’s valuation and prospects. Whereas purchases can replicate optimism, gross sales are generally seen as an indication of potential considerations concerning the firm’s future efficiency. On this case, the extra funding by Ellin, who has important affect and perception into the corporate, could also be interpreted as a constructive signal.

It is price noting, as per the footnotes within the submitting, that the reported possession doesn’t embody shares held by a household belief and household basis the place Ellin doesn’t train voting or dispositive energy. Moreover, the reported shares embody these held by entities resembling Trinad Capital Grasp Fund Ltd., Trinad Capital Administration, LLC, and JJAT Corp., the place Ellin is deemed to have sole voting and dispositive energy.

As of this reporting, PodcastOne, Inc. has not issued any public assertion relating to this transaction. Traders and market watchers will probably observe any future transactions and firm efficiency with eager curiosity, as insider exercise usually supplies helpful context to the broader market narrative.

In different latest information, PodcastOne anticipates a document income of $13 million in its preliminary Q1 outcomes, marking a 21% enhance from the identical interval final yr. The corporate’s shareholders have elected all eight nominees to PodcastOne’s Board of Administrators and ratified the appointment of Macias Gini & O’Connell, LLP because the unbiased registered public accounting agency for the fiscal yr ending March 31, 2025. PodcastOne has additionally welcomed Jon Merriman to its Board of Administrators, a strategic transfer geared toward enhancing the corporate’s progress initiatives and visibility inside the monetary sector.

As well as, PodcastOne tasks revenues to achieve between $50M and $55M for the fiscal yr ending March 31, 2025. This projection follows a profitable fiscal yr that concluded on March 31, 2024, with the corporate reporting $43.3M in income and $660K in adjusted EBITDA. Furthermore, PodcastOne has entered a major business-to-business partnership with a Fortune 250 firm, anticipated to contribute over $20M in annual revenues.

These are among the many latest developments that spotlight the corporate’s upward trajectory. The corporate has additionally reported an increase to the eleventh spot in Podtrac’s rankings and an enlargement to a 5.5 million distinctive month-to-month viewers within the U.S. and 17.5 million world downloads and streams. These figures are preliminary and topic to closing evaluation by PodcastOne’s unbiased registered accounting agency.

Lusso’s Information Insights

Govt Chairman Robert S. Ellin’s latest buy of PodcastOne, Inc. (NASDAQ:PODC) shares is a noteworthy occasion that aligns with some constructive indicators from Lusso’s Information knowledge. The corporate’s market capitalization stands at a modest $45.15 million, and whereas the P/E ratio is damaging at -2.27, reflecting its lack of profitability during the last twelve months, there’s a silver lining. Analysts are optimistic, predicting that PodcastOne will flip worthwhile this yr. This forward-looking sentiment might have influenced Ellin’s resolution to extend his stake within the firm.

Including to the narrative of potential progress, the corporate’s income has grown by 25.32% within the final twelve months as of Q1 2023, and its liquid belongings exceed short-term obligations, suggesting monetary stability. This may very well be a important issue within the firm’s skill to navigate by way of its progress section. Furthermore, the corporate’s latest efficiency within the inventory market has been important, with a 38.23% return during the last month, which could have contributed to Ellin’s confidence within the firm’s prospects.

Among the many Lusso’s Information Suggestions, two stand out particularly for PodcastOne. Firstly, the corporate holds additional cash than debt on its stability sheet, a reassuring signal for buyers involved about monetary threat. Secondly, the excessive shareholder yield signifies that the corporate is returning worth to its shareholders, which can embody buybacks or different types of capital distribution, although it doesn’t pay a dividend. For these desirous about a deeper evaluation, Lusso’s Information presents extra recommendations on their platform.

As buyers weigh the importance of insider transactions, these Lusso’s Information insights can present a broader context to Ellin’s latest inventory buy and the corporate’s monetary well being. For extra detailed evaluation and ideas, buyers can discover the total suite of insights accessible on Lusso’s Information, which incorporates a number of extra ideas for PodcastOne.

This text was generated with the assist of AI and reviewed by an editor. For extra info see our T&C.

Markets

Core Scientific, on Cusp of Turning into a Main Power in AI Internet hosting, Initiated at Purchase: Canaccord

Canaccord initiated protection of Core Scientific with a purchase score.

The bitcoin miner is on the cusp of turning into a significant participant in AI internet hosting, the report stated.

The dealer famous that Core Scientific has potential upside from its mining enterprise.

Core Scientific (CORZ) is on the cusp of turning into a significant pressure in synthetic intelligence (AI) internet hosting, dealer Canaccord stated in a Monday report initiating protection of the bitcoin (BTC) miner.

Canaccord began protection of the crypto mining firm with a purchase score and a $16 worth goal. The shares had been 1.4% larger at $12.15 in early buying and selling.

A transformative 12-year contract the agency inked with hypersaler CoreWeave in June is a recreation changer, Canaccord stated. The dealer views it because the “first and landmark ‘mega deal’ signed by a bitcoin miner to supply high-performance compute (HPC) information middle internet hosting capability.”

A hyperscaler is a large-scale information middle specializing in delivering large quantities of computing energy.

Canaccord recognized three optimistic drivers for the inventory: “Ramping income in AI internet hosting, higher money circulation and probably extra web site acquisitions on the best way,” analysts led by Joseph Vafi wrote.

The value goal includes about $12 for the CoreWeave contract, $3 for the corporate’s remaining energy provide that has been chosen for AI internet hosting and round $1 for the bitcoin-mining enterprise.

The corporate additionally has potential upside from mining. It nonetheless has about 230 megawatts (MW) of energy that can be utilized for bitcoin mining, even after repurposing virtually 500MW for AI internet hosting, the report famous.

Learn extra: Bitcoin Mining Profitability Stays at All-Time Lows as Costs Fall, Hashrate Rises, JPMorgan Says

Prediction: This Main Synthetic Intelligence (AI) Inventory May Compete With Nvidia within the Not-Too-Distant Future

PodcastOne government chairman buys $32,181 in firm inventory

Core Scientific, on Cusp of Turning into a Main Power in AI Internet hosting, Initiated at Purchase: Canaccord

Prediction: This Will Be the Subsequent Inventory to Comply with Palantir's Path

Carlyle-backed StandardAero targets $7.5 billion valuation in US IPO

BTC.com To Rebrand Itself As ‘CloverPool’

3 No-Brainer Curiosity-Price-Delicate Dividend Shares to Purchase Proper Now for Much less Than $1,000

Constellation Power PT raised at Wells Fargo & Morgan Stanley on TMI restart

Warren Buffett's Secret Portfolio Is Dumping Shares of three Supercharged Synthetic Intelligence (AI) Shares (No, Not Nvidia!)

Australia sues grocery giants Woolworths and Coles over 'illusory' reductions

Qualcomm approaches Intel to discover potential acquisition

Rightmove shares rise after rejecting REA takeover bid

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoInventory market in the present day: US futures slip as Micron slides, with information on deck

-

Markets3 months ago

Markets3 months agoFutures dip as Micron drags down chip shares forward of financial information

-

Markets3 months ago

Markets3 months agoApogee shares rise almost 4% on upbeat steering and earnings beat

-

Markets3 months ago

Markets3 months agoWhy Is Micron Inventory Down After a Double Earnings Beat?

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoHungary central financial institution tells lenders to reimburse purchasers after Apple glitch

-

Markets3 months ago

Markets3 months agoSoftBank to spend money on search startup Perplexity AI at $3 billion valuation, Bloomberg experiences

-

Markets3 months ago

Markets3 months agoMeet the 1 S&P 500 Inventory That's Outperforming Nvidia So Far in 2024

-

Markets3 months ago

Markets3 months agoDown 30% From Its All-Time Excessive, Ought to You Purchase Synthetic Intelligence (AI) Famous person Tremendous Micro Pc?

-

Markets3 months ago

Markets3 months agoIf You'd Invested $1,000 in Starbucks Inventory 20 Years In the past, Right here's How A lot You'd Have Immediately

-

Markets3 months ago

Markets3 months agoPrediction: This Transfer From Nvidia within the Second Half Will Be A lot Greater Than the Inventory Break up