Markets

5 Causes Nvidia Isn't in an AI-Fueled Bubble

The inventory market has an extended historical past of making bubbles, notably within the know-how sector. Nevertheless, relating to Nvidia (NASDAQ: NVDA), the chip maker’s eye-popping valuation could not really be indicators of a bubble. Fairly, it’d mirror a deeper fact concerning the quickly evolving state of synthetic intelligence (AI).

Nvidia’s shares are at the moment buying and selling at 77.1 occasions trailing earnings, a lofty valuation by historic requirements and wealthy even for the high-growth tech sector. This has led some buyers to query whether or not it is time to take earnings on Nvidia inventory. In any case, the chipmaker’s shares are up by a staggering 206% over the prior 12 months.

Nevertheless, a number of traces of proof recommend that Nvidia’s progress story continues to be within the early innings and that AI is on monitor to basically alter the world. Here’s a take a look at 5 key tailwinds that ought to energy Nvidia’s shares even greater over the following a number of years.

5 key themes

First, the overall inhabitants stays largely unaware of the true energy of AI. This example is about to vary dramatically later this yr as Apple integrates AI into its ecosystem and Amazon strives to make Alexa smarter with AI.

As a broad base of shoppers start to expertise the advantages of AI of their each day lives, demand for AI-powered services and products will possible skyrocket, driving substantial income progress for firms like Nvidia that present the structure behind the know-how.

Second, the tempo of AI improvement is accelerating. The of computing energy has put humanity on the doorstep of a collection of “Gutenberg moments”, or occasions that fully upend the established order.

This quickening tempo of innovation implies that rivals in all probability will not have time to problem Nvidia’s dominant place within the AI-capable graphics processing unit (GPU) area. Whereas rivals like Superior Micro Gadgets and Intel are to chop into Nvidia’s dominant market share, the window of alternative is closing.

Third, the AI arms race between main American companies, and the U.S. and China extra broadly, will not permit builders time to create various ecosystems.

The race to realize synthetic basic intelligence (AGI) is on, and Nvidia’s superchips like Blackwell will possible be the first drivers of this transformation. As firms and nations scramble to realize a aggressive edge in AI, Nvidia’s know-how will stay in excessive demand.

Fourth, the appearance of AI will not comply with any guidelines established by prior transformational applied sciences just like the web or vehicles. AI can probably alter human society at a basic degree, and it’ll occur in lower than 5 years.

Conventional valuation metrics and historic precedents, in flip, could not wholly apply to groundbreaking firms like Nvidia.

Fifth, the potential purposes of AI are nearly limitless, spanning throughout industries corresponding to healthcare, finance, transportation, and extra. As AI turns into extra refined and ubiquitous, it would create completely new markets – lots of that are unimaginable right this moment.

Nvidia, with its cutting-edge AI know-how and rising buyer base, is within the catbird seat.

Key takeaways

Nvidia’s present valuation could appear excessive by historic requirements. But it surely’s essential to contemplate the corporate’s distinctive place within the quickly evolving AI panorama.

With the overall inhabitants largely unaware of AI’s already unimaginable capabilities, the quickening tempo of improvement, and an ongoing arms race, Nvidia ought to proceed to put up record-breaking income progress within the coming years.

In any case, Nvidia’s potential is actually unprecedented because the gatekeeper to a $100 trillion AI-based financial system. Considered on this context, the rising bubble discuss across the chip maker’s shares appears unjustified.

Do you have to make investments $1,000 in Nvidia proper now?

Before you purchase inventory in Nvidia, think about this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they imagine are the for buyers to purchase now… and Nvidia wasn’t one in all them. The ten shares that made the lower may produce monster returns within the coming years.

Think about when Nvidia made this listing on April 15, 2005… in case you invested $1,000 on the time of our suggestion, you’d have $808,105!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of June 10, 2024

John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. has positions in Apple. The Motley Idiot has positions in and recommends Amazon, Apple, and Nvidia. The Motley Idiot has a .

was initially revealed by The Motley Idiot

Broadcom Inc (NASDAQ:) just lately introduced vital updates to its VMware Cloud Basis (VCF), aiming to reinforce digital innovation with sooner infrastructure modernization, improved developer productiveness, and higher cybersecurity at a low .

The most recent developments in VCF assist clients’ wants by integrating enterprise-class computing, networking, storage, administration, and safety throughout numerous environments.

The brand new VCF Import performance permits seamless integration of present vSphere and vSAN environments into VCF, optimizing sources with no need an entire rebuild.

This may considerably improve effectivity, decrease prices, and pace up time to worth.

place because the second-largest AI semiconductor provider globally, trailing solely Nvidia Corp (NASDAQ:).

They famous the corporate’s dominant market share of roughly 55-60% in customized (ASIC) chip designs market projected to develop at a compound annual progress fee (CAGR) of over 20%, presenting a $20 billion to $30 billion alternative.

Analysts predict Broadcom will drive $11 billion to $12 billion in AI revenues in 2024, with additional progress to $14 billion to $15 billion in 2025.

This optimism is fueled by main tech firms’ growing give attention to customized ASIC options for AI computing wants.

Worth Motion: AVGO shares traded greater by 0.30% at $1,596.78 on the final examine on Tuesday.

Disclaimer: This content material was partially produced with the assistance of AI instruments and was reviewed and revealed by Benzinga editors.

Photograph by way of Shutterstock

“ACTIVE INVESTORS’ SECRET WEAPON” Supercharge Your Inventory Market Recreation with the #1 “information & every thing else” buying and selling software: Benzinga Professional –

Get the newest inventory evaluation from Benzinga?

This text initially appeared on

© 2024 Benzinga.com. Benzinga doesn’t present funding recommendation. All rights reserved.

BEIJING (Reuters) – Tencent Holdings (OTC:) Ltd’s newly launched “Dungeon & Fighter” (DnF Cell) has acquired off to a powerful begin, dominating top-grossing charts on Apple (NASDAQ:)’s iOS platform in China for practically a month, trade information confirmed.

The sport, launched on this planet’s greatest gaming market on Might 21, broke the $100 million income mark in simply 10 days, in accordance with a report launched by information analytics agency Sensor Tower this week.

It additionally topped the worldwide cell recreation income progress chart for Might and ranked eighth in total income.

Within the first 10 days of its launch, DnF Cell’s income in China’s iOS market surpassed the mixed earnings of Tencent’s different in style titles “Honor of Kings” and “PUBG Cell,” in accordance with a separate Sensor Tower report dated June 17.

This surge contributed to a 12% progress in Tencent’s cell recreation income in Might, in accordance with Sensor Tower.

The DnF Cell title, based mostly on a preferred PC franchise, had been obtainable internationally for years. Its China launch was delayed as a result of Beijing’s non permanent freeze on new recreation approvals.

DnF Cell’s early success comes amid ongoing tensions between Tencent and smartphone distributors over gaming income sharing.

Earlier this month, Tencent pulled the sport from chosen Android app shops, citing contract expiries.

Recreation builders in China have lengthy had a contentious relationship with distributors over points corresponding to income sharing, as cell video games change into more and more in style within the broader recreation market. The usual 50% income break up has typically been a bone of competition.

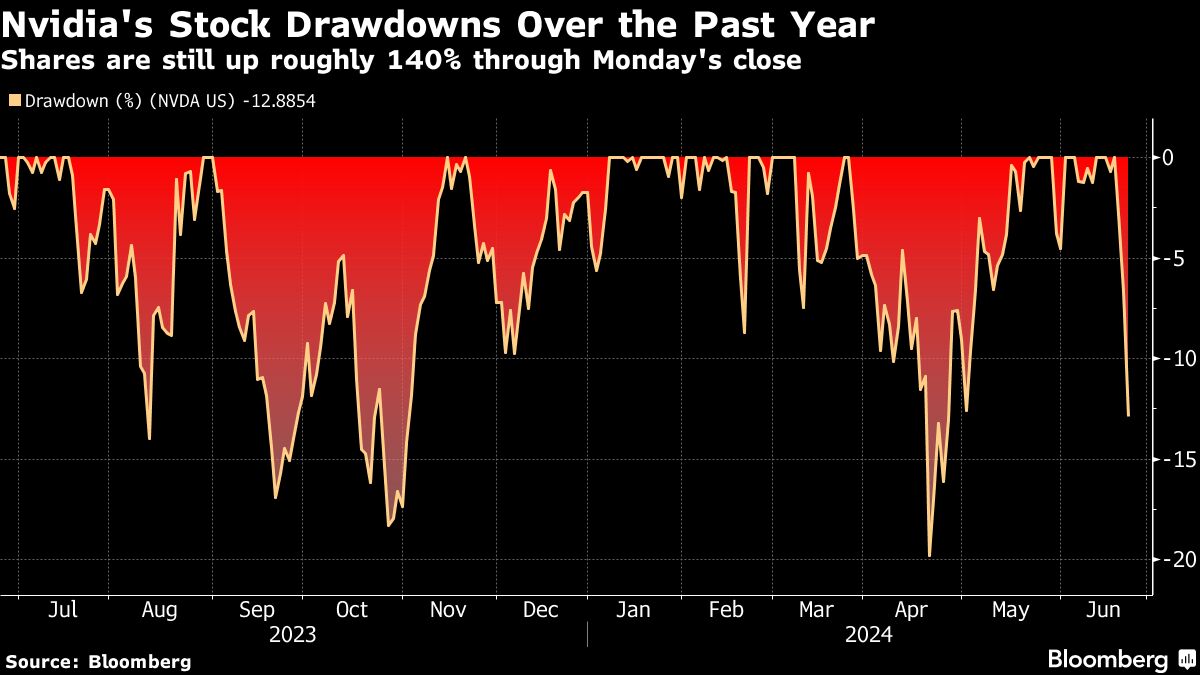

(Lusso’s Information) — A $430 billion sell-off earlier this week in artificial-intelligence darling Nvidia Corp. was not more than a blip to Neuberger Berman Group’s Steve Eisman.

Most Learn from Lusso’s Information

The senior portfolio supervisor, finest identified for his “Massive Quick” wager in opposition to subprime mortgages forward of the worldwide monetary disaster, owns “loads” of the chipmaker’s shares and considers it a long-term play that’s going to be related for years to come back, he mentioned Tuesday in an an interview on Lusso’s Information Tv.

Merchants appeared to share his view Tuesday because the inventory rallied 6.8%, climbing again from a three-day slide that pushed shares down greater than 10% for the primary time since April, previous the brink that represents a correction.

“When you take a look at the chart on Nvidia, you may barely see the correction,” Eisman mentioned. “I don’t assume it means something.”

The AI poster-child has soared this yr amid a livid urge for food for its chips that dominate the marketplace for artificial-intelligence computing. Its newest climb noticed shares surge 43% from its Could 22 earnings report and stock-split announcement to the June 18 peak, when it toppled Microsoft Corp. to turn into the world’s Most worthy firm — a title it has since misplaced.

Nvidia remains to be up 155% this yr via Tuesday’s shut. As some skeptics fear that the corporate has grown too rapidly, Eisman says worth is the very last thing to worry over.

“One of many issues I realized working a hedge fund is that shorting a inventory solely due to valuation is a dying want,” he mentioned, including that individuals buy a inventory even when it’s perceived to be costly as a result of they’re shopping for right into a story. “So long as the story is unbroken — like Nvidia is clearly intact — the story goes to proceed. I don’t assume all that a lot in regards to the valuation of Nvidia.”

The message that Nvidia will proceed to learn from booming AI demand was echoed by Nuveen Asset Administration LLC’s chief funding officer.

“Nvidia is the corporate that wins on this house, principally it doesn’t matter what,” Saira Malik mentioned in an interview. “Everybody who desires to shift into AI principally has to make use of Nvidia’s merchandise. Their development price has been so sturdy that their price-to-earnings actually isn’t costly.”

Malik is a portfolio supervisor for a number of key funding methods for Nuveen, a $1.3 trillion international asset supervisor. The $125 billion Faculty Retirement Equities Fund – Inventory Account, which she oversees, has outperformed 86% of friends over the previous yr, in keeping with knowledge compiled by Lusso’s Information. Microsoft, Nvidia, Apple Inc. and Amazon.com Inc. had been the fund’s largest holdings as of the top of Could.

“Individuals will say the inventory worth itself has simply carried out so effectively, how are you going to personal it?” Malik mentioned. When in comparison with friends, “it’s not an costly inventory.”

Whereas Nvidia trades at a premium of about 50% to the Nasdaq 100 Index, its 12-month ahead price-to-earnings ratio has pulled again from a 2023 excessive of 63 instances right down to about 40. It’s now valued near friends corresponding to Superior Micro Gadgets Inc. Malik mentioned the AI-fueled rally in Nvidia and Microsoft — which has propelled US inventory benchmarks to a collection of file highs — is in contrast to the dot-com bubble.

“These corporations are far more dominant as a result of they aren’t model new,” she mentioned. “They’ve been round for years investing on this pattern. So I do assume it’s completely different this time.”

–With help from Jeran Wittenstein, Ryan Vlastelica, Lisa Abramowicz, Annmarie Hordern and Dani Burger.

(Updates with Tuesday’s inventory transfer.)

Most Learn from Lusso’s Information Businessweek

©2024 Lusso’s Information L.P.

What's Going On With Broadcom Inventory On Tuesday?

Tencent's 'Dungeon & Fighter' recreation dominates China's cell obtain charts

Steve Eisman Says the Nvidia Story Is Going to Final for Years

Chinese language liquor makers endeavour to provide Westerners a style for baijiu

Merchants have poured $5 billion into leveraged Nvidia ETFs. They're up 425% even after the inventory's large wipeout.

Troubled on line casino agency Star names new CEO amid regulator enquiries, administration exodus

Shares are wanting 'eerily comparable' to the final bear-market crash, Charles Schwab says

Asian shares buoyed by tech positive factors, Australia sinks on scorching CPI

Why the inventory market might surge 4% to file highs by the top of July

People hunt down cooler locations for July 4 journey as temperatures sizzle

Rivian Will get $5 Billion Lifeline in Joint Enterprise With Volkswagen

Waymo's autonomous ride-hailing service now out there to all in San Francisco

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets2 months ago

Markets2 months agoUnitedHealth Group Demonstrates Resilience in Q1 2024 Financial Report

-

Markets2 months ago

Markets2 months agoUnderstanding a Flash Crash in the Stock Market

-

Markets2 months ago

Markets2 months agoA Glimpse Into the Buzz of Upcoming IPOs in April 2024

-

Markets2 months ago

Markets2 months agoWiSA Technologies Shares Surge After Strategic Licensing Agreement and Reverse Split

-

Markets2 months ago

Markets2 months agoThe Most Shorted Stocks as of Late March 2024

-

Markets1 month ago

Markets1 month agoTechnical Analysis of Tupperware Brands Corporation (TUP)

-

Markets1 month ago

Markets1 month agoPetco (NASDAQ: WOOF) Beats Q1 CY2024 Estimates: What Traders Should Know

-

Markets1 month ago

Markets1 month agoMGO Global Inc. (NASDAQ: MGOL) Surges 446% on Strong First Quarter Earnings

-

Markets1 month ago

Markets1 month agoSnowflake Inc. (SNOW) Earnings Miss: What It Means for Traders

-

Markets2 months ago

Markets2 months agoBoeing’s Proactive Measures Ahead of Whistleblower Hearing

-

Markets1 month ago

Markets1 month agoGreenwave Technology Solutions (NASDAQ: GWAV) Plummets 62% After Announcing Share Offering