Markets

Fed Is About to Get Validation for Its Jumbo Fee Lower

(Lusso’s Information) — The Federal Reserve’s most well-liked worth metric and a snapshot of shopper demand are seen corroborating each the central financial institution’s aggressive interest-rate reduce and Chair Jerome Powell’s view that the financial system stays sturdy.

Most Learn from Lusso’s Information

Economists see the private consumption expenditures worth index rising simply 0.1% in August for the second time in three months. The inflation gauge in all probability climbed 2.3% from a yr earlier, the smallest annual acquire since early 2021 and a shade increased than the central financial institution’s 2% objective.

The slowdown in inflation from a yr in the past displays falling vitality and weaker meals costs, together with moderating core prices. The PCE worth gauge excluding meals and gas in all probability rose 0.2% for a 3rd month, economists count on authorities information to point out Friday.

The step-down in inflationary pressures from earlier this yr offered Fed policymakers with sufficient confidence to decrease charges on Sept. 18 by a half share level. The reduce was the primary in additional than 4 years, and represented a pivot within the central financial institution’s coverage towards averting a deterioration within the job market.

Traders will parse remarks from numerous Fed officers within the coming week. Governors Michelle Bowman, Adriana Kugler and Lisa Prepare dinner, together with regional presidents Raphael Bostic and Austan Goolsbee, are amongst these set to seem at numerous occasions.

The August inflation figures might be accompanied by information on private spending and earnings, and economists undertaking one other strong advance in family outlays. Sustained shopper spending progress helps increase the possibilities that the financial system will proceed increasing.

Different financial information embody August new-home gross sales, second-quarter gross home product together with annual GDP revisions again to 2019, weekly jobless claims, and August orders for sturdy items.

What Lusso’s Information Economics Says:

“In our view, the Fed’s jumbo reduce will increase the prospect of a smooth touchdown, however in no way ensures it. Our baseline remains to be for the unemployment price to achieve 4.5% earlier than the tip of 2024, earlier than rising to five% subsequent yr.”

— Anna Wong, Stuart Paul, Eliza Winger, Estelle Ou and Chris G. Collins, economists. For full evaluation, click on right here

In Canada, GDP information for July and a flash estimate for August are anticipated to point out weak progress within the third quarter, doubtless under the Financial institution of Canada’s forecast of two.8% annualized growth. In the meantime, the central financial institution’s governor, Tiff Macklem, will communicate at a banking convention in Toronto.

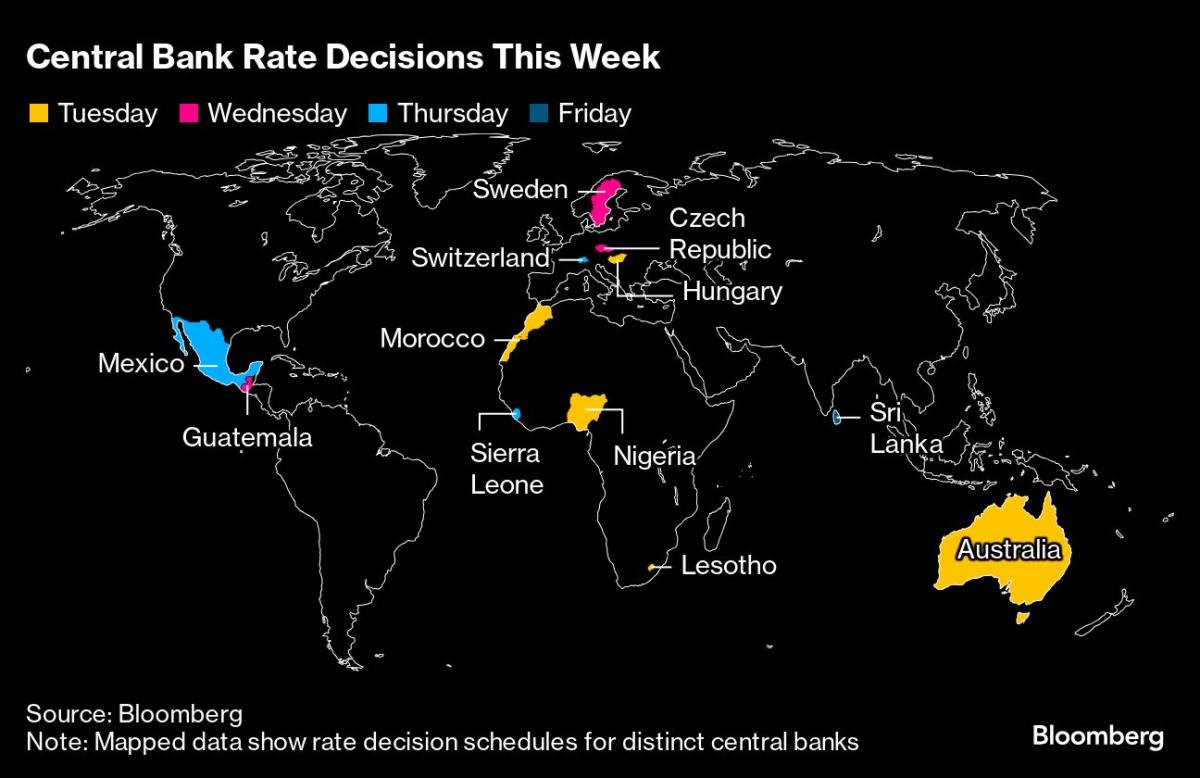

Elsewhere, the OECD will reveal new financial forecasts on Wednesday, central banks in Switzerland and Sweden could ship price cuts, and their Australian counterpart is anticipated to remain on maintain.

Click on right here for what occurred previously week and under is our wrap of what’s developing within the international financial system.

Asia

The Reserve Financial institution of Australia is anticipated to maintain its money price goal unchanged at 4.35% when the board meets on Tuesday, with the main target prone to fall on whether or not Governor Michele Bullock retains her hawkish tone after strong labor figures prompted merchants to pare bets on a December price reduce.

Lusso’s Information Economics nonetheless sees a path to potential RBA easing within the fourth quarter. Authorities should wait till Wednesday to see if Australian inflation cooled for a 3rd month in August.

Talking on Sunday, Australian Treasurer Jim Chalmers mentioned he expects upcoming information to point out encouraging progress in combating inflation however acknowledged the central financial institution is probably not prepared to chop rates of interest this week.

Different nations releasing inflation updates embody Malaysia and Singapore, the place worth progress is forecast to have slowed in August.

Japan will get contemporary inflation information with the discharge Friday of Tokyo shopper costs, that are anticipated to have risen at a tempo exceeding the Financial institution of Japan’s 2% goal in September.

Buying supervisor indexes for September are due from Australia and India on Monday and from Japan a day later.

In China, the 1-year medium time period lending facility price is anticipated to be held unchanged at 2.3%, and information Friday will present whether or not industrial revenue progress maintained momentum in August after rising on the quickest clip in 5 months in July.

Commerce statistics are due from South Korea, Thailand and Hong Kong.

Europe, Center East, Africa

4 central financial institution choices are scheduled in Europe, the place buyers could query the urge for food of policymakers to observe within the footsteps of the Fed with a half-point reduce.

That’s definitely the case with the Swiss Nationwide Financial institution on Thursday. Whereas a majority of economists foresee a quarter-point transfer, observers do reckon the US discount has elevated the possibilities of a step of the identical measurement as officers confront the persistent power of the franc. That is the ultimate assembly for President Thomas Jordan, whose time period concludes on the finish of the month.

Yesterday, Sweden’s Riksbank is anticipated to decrease borrowing prices by 1 / 4 level for the third time this yr, taking the speed to three.25%, and to stipulate a path to further cuts.

The present steerage is for 2 or three extra strikes in 2024 — together with on Wednesday. Policymakers talked a few half-point reduce eventually month’s assembly, and whereas that dialogue may come up once more, most economists imagine the central financial institution would extra doubtless wait till November to do an even bigger transfer.

In Jap Europe, in the meantime, each the Hungarian central financial institution on Tuesday and its Czech counterpart on Thursday are anticipated to ship quarter-point reductions.

Within the euro zone and the UK, an preliminary take a look at buying managers indexes for September might be launched on Monday, signaling the state of private-sector exercise on the finish of the third quarter.

With Germany’s weak spot a focus for buyers, the Ifo enterprise confidence gauge might be a spotlight on Tuesday, the identical day Bundesbank President Joachim Nagel is because of communicate on the financial system. New forecasts from the nation’s financial institutes are scheduled for Thursday.

France’s information might be carefully watched each by buyers and the nation’s new finance minister, Antoine Armand. PMIs for the euro space’s No. 2 financial system received an Olympic enhance in August, however that impact is anticipated to have pale this month. Client confidence numbers are additionally due.

Readings of French and Spanish inflation for September will draw consideration on Friday, hinting on the general end result for the area due the next week. Economists predict each nations’ readings will drop under 2%.

Other than Nagel, greater than half a dozen euro-zone policymakers are scheduled to talk, together with European Central Financial institution President Christine Lagarde, chief economist Philip Lane, and Spain’s new central financial institution chief Jose Luis Escriva.

Throughout the African continent, numerous central financial institution choices are additionally scheduled:

-

Nigerian officers on Tuesday will doubtless pause a tightening cycle that’s lifted the speed to 26.75% from 11.5% in simply over two years. They’ll be inspired by inflation cooling to a six-month low as they weigh the influence of floods within the nation and a steep improve in gasoline prices on worth progress.

-

Morocco’s central financial institution will in all probability maintain its price at 2.75% to permit time for June’s shock reduce to seep by the home market. The dominion wants low charges to facilitate funding and include unemployment. It has large funding plans for reconstruction of earthquake-hit areas and infrastructure forward of the FIFA World Cup in 2030.

-

In southern Africa, officers in Lesotho could diverge from South Africa’s price reduce and go away borrowing prices at 7.75%, as inflation stays elevated. Whereas Lesotho tends to reflect the coverage of its neighbor, its key price is already 25 foundation factors decrease.

Elsewhere, Zambia’s Finance Minister Situmbeko Musokotwane will on Friday announce plans to assist the financial system bounce again from one of many hardest years it’s confronted this century when he unveils his 2025 finances for Africa’s second largest copper producer.

Latin America

Brazil watchers may have so much to digest, with minutes of the central financial institution’s September price assembly and a quarterly inflation report taking heart stage.

The previous could present a extra detailed coverage road-map after a quarter-point hike on Sept. 18, to 10.75%, whereas the latter updates all method of financial estimates and situations. Search for the BCB to mark up forecasts for inflation, the important thing price, and GDP progress.

Rounding out the week for Latin America’s greatest financial system, jobs information will doubtless present Brazil’s labor market stays at traditionally tight ranges whereas mid-month inflation could have stalled close to the highest of the central financial institution’s goal vary.

Argentina is slated to submit GDP-proxy readings for July, which can construct assist for the view that the financial system is previous its 2024 nadir and is starting a second-half restoration.

In Mexico, downshifting home demand may even see one other set of soppy retail gross sales prints — on the heels of June’s damaging annual and month-to-month readings — whereas mid-month inflation information aren’t doubtless to offer policymakers with a slam dunk trigger to chop or maintain when Banxico meets a number of days later.

The early consensus expects a quarter-point reduce to 10.5%, although some analysts see a attainable half-point discount to remain on tempo with the Fed.

–With help from Brian Fowler, Robert Jameson, Niclas Rolander, Monique Vanek, Piotr Skolimowski, Matthew Hill and Souhail Karam.

(Updates with Australia Treasurer in Asia part, France in EMEA part)

Most Learn from Lusso’s Information Businessweek

©2024 Lusso’s Information L.P.

European auto shares might not expertise a right away increase following central financial institution rate of interest cuts, regardless of hopes for elevated affordability in new automobiles, Morgan Stanley identified in a be aware to shoppers on Wednesday.

Traditionally, the sector doesn’t react rapidly to fee cuts, and weak underlying demand, mixed with new and used automotive value deflation, sometimes takes time to resolve.

“Decrease charges alone can not save the auto sector,” Morgan Stanley analysts famous of their report, emphasizing that whereas decreased charges might assist automotive affordability, “underlying demand can take a number of quarters to enhance.”

In consequence, the analysts stay cautious about European auto producers (OEMs) and see margin dangers looming over the sector.

Morgan Stanley’s macro crew forecasts that the Federal Reserve will implement its first 25-basis-point fee lower on the September Federal Open Market Committee (FOMC) assembly, bringing the coverage fee down to five.125%.

The analysts anticipate a complete of three such cuts earlier than the tip of the 12 months. Nevertheless, the analysts warn that this cheaper cash is probably not sufficient to offset the pressures within the auto sector.

The report additionally highlights that decrease charges are likely to coincide with decreased common promoting costs (ASPs) as OEMs transfer to defend their market share.

This may occasionally assist enhance affordability however may current a difficult margin setting. “We already mirror decrease charges in our new automotive affordability estimates, serving to however not totally resolving trade pressures,” the report famous.

Moreover, the research exhibits that OEMs, as credit-sensitive shares, might not profit from falling bond yields as a lot as anticipated.

“Decrease bond yields, though useful for affordability, might be the consequence of decrease combination demand and usually are not at all times related to tighter spreads,” Morgan Stanley stated, whereas additionally declaring that “extra bullish could be indicators of reflation in China.”

Morgan Stanley’s knowledge additionally exhibits that European automotive shares underperform when yields drop quickly. “Autos’ relative efficiency averages -7% in months when 10Y bond yields fall over 50bps,” the report famous, indicating that rising bond yields have traditionally been extra supportive for the sector.

As such, the analysts counsel that for buyers with a multi-year horizon, the sector’s risk-reward profile stays poor.

“We proceed to suppose margin downgrades make the risk-reward within the sector fairly poor,” the report said, warning that the present weak demand setting and excessive margin estimates nonetheless pose dangers for European carmakers.

Regardless of the strain on OEMs, Morgan Stanley’s evaluation additionally touched on the position of inflation. The auto sector had beforehand benefited from rising costs, however “latest knowledge spotlight that the elemental backdrop for automotive pricing is now deteriorating,” with new automotive value inflation within the U.S. turning unfavourable and seller incentives rising.

“We see affordability as nonetheless stretched,” Morgan Stanley stated, citing weaker underlying new automotive demand at present costs. The report additionally famous that Bayerische Motoren Werke AG (WA:)’s latest revenue warning, which pointed to weak demand, particularly in China, as a key issue affecting margins.

Markets

Mortgage and refinance charges at this time, September 22, 2024: Charges drop 80 foundation factors in 2 months

Mortgage charges have fallen considerably during the last couple of months. Based on Zillow knowledge, is 5.70%, down 80 foundation factors since July 22. The is 5.04%, which is 71 foundation factors decrease than this time in July.

The Federal Reserve is about to chop the federal funds fee six extra occasions earlier than the top of 2025, which suggests mortgage charges will most likely proceed to lower. As a result of charges have already dropped a lot, — particularly since you will possible face extra competitors as charges fall decrease and decrease. However should you’re already a house owner and wish to refinance, it’s possible you’ll wish to maintain out for even higher charges.

Study extra:

Listed here are the present mortgage charges, in keeping with the newest Zillow knowledge:

-

30-year fastened: 5.70%

-

20-year fastened: 5.48%

-

15-year fastened: 5.04%

-

5/1 ARM: 5.94%

-

7/1 ARM: 5.91%

-

30-year VA: 5.17%

-

15-year VA: 4.86%

-

5/1 VA: 5.70%

Bear in mind, these are the nationwide averages and rounded to the closest hundredth.

These are , in keeping with the newest Zillow knowledge:

-

30-year fastened: 5.71%

-

20-year fastened: 5.37%

-

15-year fastened: 5.02%

-

5/1 ARM: 6.15%

-

7/1 ARM: 6.45%

-

5/1 FHA: 4.51%

-

30-year VA: 5.12%

-

15-year VA: 4.90%

-

5/1 VA: 5.59%

Once more, the numbers offered are nationwide averages rounded to the closest hundredth. Mortgage refinance charges are sometimes increased than charges while you purchase a home, though that is not all the time the case.

Learn extra:

Use the free to see how varied mortgage phrases and rates of interest will affect your month-to-month funds.

Our calculator additionally considers elements like property taxes and householders insurance coverage when figuring out your estimated month-to-month mortgage fee. This provides you a extra sensible concept of your whole month-to-month fee than should you simply checked out mortgage principal and curiosity.

The common 30-year mortgage fee at this time is 5.70%. A 30-year time period is the most well-liked sort of mortgage as a result of by spreading out your funds over 360 months, your month-to-month fee is decrease than with a shorter-term mortgage.

The common 15-year mortgage fee is 5.04% at this time. When deciding between a, contemplate your short-term versus long-term targets.

A 15-year mortgage comes with a decrease rate of interest than a 30-year time period. That is nice in the long term since you’ll repay your mortgage 15 years sooner, and that’s 15 fewer years for curiosity to build up. However the trade-off is that your month-to-month fee might be increased as you repay the identical quantity in half the time.

Let’s say you get a . With a 30-year time period and a 5.70% fee, your month-to-month fee towards the principal and curiosity can be about $1,741 and also you’d pay $326,832 in curiosity over the lifetime of your mortgage — on high of that authentic $300,000.

When you get that very same $300,000 mortgage however with a 15-year time period and 5.04% fee, your month-to-month fee would leap as much as $2,379. However you’d solely pay $128,155 in curiosity through the years.

With a, your fee is locked in for all the lifetime of your mortgage. You’ll get a brand new fee should you refinance your mortgage, although.

An retains your fee the identical for a predetermined time period. Then, the speed will go up or down relying on a number of elements, such because the economic system and the utmost quantity your fee can change in keeping with your contract. For instance, with a 7/1 ARM, your fee can be locked in for the primary seven years, then change yearly for the remaining 23 years of your time period.

Adjustable charges sometimes begin decrease than fastened charges, however as soon as the preliminary rate-lock interval ends, it’s potential your fee will go up. These days, although, some fastened charges have been beginning decrease than adjustable charges. Discuss to your lender about its charges earlier than selecting one or the opposite.

Dig deeper:

Mortgage lenders sometimes give the bottom mortgage charges to individuals with increased down funds, nice or glorious credit score scores, and low debt-to-income ratios. So, if you’d like a decrease fee, strive saving extra,, or paying down some debt earlier than you begin looking for properties.

Ready for charges to drop most likely isn’t the very best technique to get the bottom mortgage fee proper now except you might be really in no rush and don’t thoughts ready till the top of 2024 or into 2025. When you’re prepared to purchase, focusing in your private funds might be one of the simplest ways to decrease your fee.

Study extra:

To seek out the on your scenario, apply for with three or 4 firms. Simply make sure to apply to all of them inside a short while body — doing so gives you probably the most correct comparisons and have much less of an affect in your credit score rating.

When selecting a lender, don’t simply examine rates of interest. Have a look at the — this elements within the rate of interest, any low cost factors, and costs. The APR, which can be expressed as a proportion, displays the true annual price of borrowing cash. That is most likely a very powerful quantity to take a look at when evaluating mortgage lenders.

Based on Zillow, the nationwide common 30-year mortgage fee is 5.70%, and the common 15-year mortgage fee is 5.04%. However these are nationwide averages, so the common in your space might be totally different. Averages are sometimes increased in costly components of the U.S. and decrease in cheaper areas.

The common 30-year fastened mortgage fee is 5.70% proper now, in keeping with Zillow. Nevertheless, you may get a fair higher fee with a superb credit score rating, sizeable down fee, and low .

Sure, mortgage charges are anticipated to maintain dropping in 2024 and all through 2025.

Lusso’s Information — The Federal Reserve’s resolution to chop rates of interest by 50 foundation factors has sparked a powerful motion within the markets, however many surprise what the much-anticipated dovish shift means past the near-term response.

The Fed’s transfer on Sept. 19 was extensively anticipated, with the central financial institution additionally promising a further 50 foundation factors of cuts earlier than the 12 months’s finish. This initially triggered a rally, sending the to new all-time highs earlier than a “sell-the-news” response pushed markets barely decrease by the tip of the day.

Within the brief time period, this dovish transfer has left markets in a typically constructive place. The most important danger elements stay potential adverse financial information, however the present financial calendar is gentle till early October.

With out the specter of important earnings studies or main financial releases, buyers look like working in an atmosphere that’s “1) easing Fed, 2) slowing however ‘OK’ financial information, and three) typically strong earnings,” Sevens Report stated in a latest observe.

Cyclical sectors, together with vitality, supplies, shopper discretionary, and industrials, are anticipated to outperform, whereas know-how could lag within the close to time period.

Nevertheless, the longer-term implications of the Fed’s resolution could also be extra advanced. The important thing query for buyers is whether or not the Fed acted in time to stave off a broader financial slowdown.

Based on the Sevens Report, if the speed cuts are well timed, they might result in falling yields, robust earnings progress, and optimistic financial tailwinds. This may seemingly lead to continued upward momentum for shares, with the potential for the S&P 500 to hit 6,000.

“I say that confidently as a result of the Fed slicing in time would create this macroeconomic final result: 1) Falling yields, 2) Continued very robust earnings progress, 3) Optimistic financial tailwinds, 4) The outstanding existence of the Fed put and 5) Expectations of accelerating progress sooner or later,” President of Sevens Report wrote within the observe.

However, if the Fed’s actions had been too late to stop an financial downturn, the market might face important dangers.

In such a situation, the S&P 500 might fall to round 3,675, marking a pointy decline of over 30% from present ranges. This draw back danger mirrors market corrections seen in earlier downturns, reminiscent of these in 2000 and 2007.

Because the markets digest the Fed’s strikes, future financial information will grow to be essential in figuring out whether or not the central financial institution’s coverage was efficient.

Extra concretely, buyers might want to maintain an in depth eye on upcoming releases to gauge whether or not the Fed has efficiently navigated the financial system away from a recession or if additional challenges lie forward.

How will EU automotive shares react to central financial institution easing?

Mortgage and refinance charges at this time, September 22, 2024: Charges drop 80 foundation factors in 2 months

What the Fed resolution means for markets, past the close to time period

Former Monero Developer Launches New Crypto Mining App

2 Shares That May Soar in 2025, In keeping with This Metric

Did the Fed simply begin the following bullish cycle for mortgage REITs?

Prediction: These 2 Synthetic Intelligence (AI) Shares Are About to See Large Progress

Road calls of the week

Fed Is About to Get Validation for Its Jumbo Fee Lower

Unique-US to suggest ban on Chinese language software program, {hardware} in related automobiles, sources say

Warren Buffett's Most secure Inventory May Not Be Apple or Coca-Cola. 1 Different Inventory That May Be a Higher Purchase within the Lengthy Run.

1 No-Brainer Electrical Automobile (EV) Inventory to Purchase With $200 Proper Now

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoInventory market in the present day: US futures slip as Micron slides, with information on deck

-

Markets3 months ago

Markets3 months agoFutures dip as Micron drags down chip shares forward of financial information

-

Markets3 months ago

Markets3 months agoApogee shares rise almost 4% on upbeat steering and earnings beat

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoWhy Is Micron Inventory Down After a Double Earnings Beat?

-

Markets3 months ago

Markets3 months agoHungary central financial institution tells lenders to reimburse purchasers after Apple glitch

-

Markets3 months ago

Markets3 months agoSoftBank to spend money on search startup Perplexity AI at $3 billion valuation, Bloomberg experiences

-

Markets3 months ago

Markets3 months agoNeglect Nvidia: Distinguished Billionaires Are Promoting It in Favor of These 7 High-Notch Shares

-

Markets3 months ago

Markets3 months agoMeet the 1 S&P 500 Inventory That's Outperforming Nvidia So Far in 2024

-

Markets3 months ago

Markets3 months agoDown 30% From Its All-Time Excessive, Ought to You Purchase Synthetic Intelligence (AI) Famous person Tremendous Micro Pc?

-

Markets3 months ago

Markets3 months agoIf You'd Invested $1,000 in Starbucks Inventory 20 Years In the past, Right here's How A lot You'd Have Immediately