Markets

Right here Is Why Bitcoin Is a Higher Funding Alternative Than Gold

It has been a good time to be an proprietor of Bitcoin (CRYPTO: BTC). For the reason that begin of 2023, the highest digital asset has soared 307%. The approval of spot exchange-traded funds (ETFs), in addition to the , have been latest catalysts.

Traders may be shocked to know that gold can also be because of bullish sentiment. Bitcoin and this valuable metallic are sometimes in comparison with each other. However the main cryptocurrency is a greater asset to personal.

How Bitcoin and gold are comparable

Market contributors like to match Bitcoin and gold. Subsequently, it may be worthwhile to first perceive some similarities between these two.

Shortage is one thing traders must be aware of. Etched in Bitcoin’s software program is a hard-supply cap of 21 million cash. And within the Earth’s crust, there’s a certain quantity of gold.

The costs of belongings which have a hard and fast provide ought to, in concept, rise as demand additionally grows. This fundamental financial precept helps clarify why gold has been considered as a well-liked retailer of worth over lengthy intervals of time.

Moreover, there’s some utility right here as properly. Gold is used primarily in jewellery, however it does have a presence in sure industrial settings. Equally, Bitcoin’s worth arises in it being a completely decentralized community with no single entity in cost, thus chopping down transaction prices whereas sending cash to somebody throughout the globe.

Bitcoin’s edge

At a excessive degree, it is easy to see how Bitcoin and gold are each scarce. Furthermore, they each have utility in numerous conditions. But when we dig deeper, we’ll simply see how the highest crypto is a superior funding.

Let’s return to the subject of shortage. Traders may suppose that gold has a fixed-supply cap, however this could not be farther from the reality. In line with the U.S. Geological Survey, 77% of all of the gold within the Earth’s crust has been mined. Consequently, there’s a sizable quantity of gold nonetheless left to be mined.

If, for no matter motive, demand for gold shot up in a brief time frame, mining corporations can be incentivized to speculate aggressively to broaden their operations with the intention to goal areas throughout the globe that may be laborious to get to. In different phrases, gold’s provide schedule might be altered primarily based on demand tendencies.

This is the place Bitcoin stands out. It is completely finite. That beforehand talked about provide cap of 21 million cash is very unlikely to vary except Bitcoin’s stakeholders wish to utterly undermine the whole community’s worth proposition. As a result of Bitcoin’s provide schedule cannot be tinkered with, its value has usually been unstable.

In comparison with gold, which is a bodily commodity, Bitcoin is a digital asset. And which means it’s simpler to retailer and transport. Bitcoin will also be divided into a lot smaller items, whereas additionally being acceptable in sure transactions. Strive going to a restaurant and slicing off a chunk of gold to pay for the invoice.

Traders additionally should not ignore the store-of-value debate, which might be the facet considered probably the most when evaluating Bitcoin and gold. Right here, Bitcoin shines brighter than the valuable metallic.

On the finish of the day, saving and investing is all about elevating one’s buying energy over time. Prior to now 5 years, Bitcoin’s value has skyrocketed 718%. Which means a $1,000 funding in June 2019 can be value virtually $8,200 immediately.

The worth of an oz of gold, then again, has solely risen by 73% throughout the identical time interval. And this stretch included main disruptive developments, just like the pandemic, inflationary pressures, larger rates of interest, and basic financial uncertainty.

Going ahead, Bitcoin and gold will possible proceed to attract comparisons. However I believe over the following 5 or 10 years, the main cryptocurrency seems to be the higher funding alternative.

Must you make investments $1,000 in Bitcoin proper now?

Before you purchase inventory in Bitcoin, take into account this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the for traders to purchase now… and Bitcoin wasn’t certainly one of them. The ten shares that made the minimize might produce monster returns within the coming years.

Take into account when Nvidia made this listing on April 15, 2005… when you invested $1,000 on the time of our suggestion, you’d have $808,105!*

Inventory Advisor offers traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of June 10, 2024

and his shoppers haven’t any place in any of the shares talked about. The Motley Idiot has positions in and recommends Bitcoin. The Motley Idiot has a .

was initially revealed by The Motley Idiot

Tremendous Micro Laptop bought off to an unbelievable begin this yr as shares greater than quadrupled from January to mid-March. This surge made Tremendous Micro eligible for S&P 500 inclusion, with the expertise {hardware} inventory (with hyperlinks to AI) being added to the index on March 18, 2024. In hindsight, that may have been a good time to take income or Quick the inventory, as shares are down by greater than 50% since then.

One of many main developments has been the report by Hindenburg Analysis, which contained worrying allegations in regards to the firm’s monetary reporting. In assessing these allegations together with Tremendous Micro’s fundamentals I maintain a impartial ranking on the inventory.

Hindenburg Casts Doubts About Tremendous Micro

The Hindenburg report is definitely the principle cause I’m impartial as an alternative of bullish on SMCI inventory, and I consider it has brought about hesitancy amongst many AI inventory analysts and traders.

The accusations are fairly simple. In keeping with Hindenburg, Tremendous Micro engaged in accounting manipulation which included “sibling self-dealing and evading sanctions”. Anybody who thinks this sounds far fetched could want to do not forget that the SEC charged Tremendous Micro with widespread accounting violations in August 2020. Hindenburg’s report additionally argued that almost all of the individuals concerned with that accounting malpractice are again on Tremendous Micro’s group.

Hindenburg’s group interviewed a number of Tremendous Micro salespeople and staff when compiling their report. It doesn’t assist that Tremendous Micro delayed its 10-Ok submitting to evaluate inner controls shortly after Hindenburg went public with its considerations. Whereas this would possibly merely be a coincidence, the timing is worrisome. Trying again a number of years, Tremendous Micro had did not file monetary statements in 2018 and was briefly delisted from the Nasdaq in consequence.

Close to the start of this month, Tremendous Micro publicly issued a denial of the accusations, with CEO Charles Liang hitting again, stating that Hindenburg’s report contained, “deceptive shows of data”. Tremendous Micro hasn’t supplied any further statements since then.

Synthetic Intelligence Progress Is Plain

Tremendous Micro’s standing as a part of the fast paced world of AI is likely one of the few causes that I’m impartial as an alternative of bearish SMCI inventory. The thrilling prospects for the corporate’s enterprise and the intense nature of the Hindenburg allegations mainly offset one another.

It’s exhausting to know what’s actual and what’s false right here, however most individuals concede that the AI trade as a complete gives compelling development prospects. Nvidia has been posting triple-digit year-over-year income development for a number of quarters. Different tech giants have included synthetic intelligence into their core companies and delivered spectacular outcomes for his or her shareholders. For example, Alphabet noticed its cloud income rise by 28.8% year-over-year as many companies rushed to create their very own AI instruments.

The factitious intelligence trade can also be projected to keep up a 19.3% compounded annual development fee from now till 2034, in accordance with Priority Analysis. The AI trade ought to proceed to develop, and that ought to elevate Tremendous Micro. The corporate ought to profit from Nvidia’s development, which is why the corporate posted distinctive income and internet revenue development throughout Nvidia’s ascent. That’s what we noticed for a number of quarters. We simply don’t know the way correct all of the numbers have been, if the allegations focusing on the agency have advantage.

Tremendous Micro Has Robust Financials at Face Worth

Whereas it’s not possible to miss Hindenburg’s allegations in opposition to Tremendous Micro, it’s nonetheless worthwhile assessing the corporate’s earlier quarterly outcomes. Shares have been dropping even earlier than Hindenburg launched its report. Whereas in March 2024 I , I felt that shares offered an amazing shopping for alternative in late-summer, till Hindenburg muddied that optimism.

For its final reported quarter, Tremendous Micro posted internet gross sales of $5.31 billion, representing a 143% year-over-year leap. In the meantime, internet revenue rose by 82% year-over-year, reaching $353 million. On the time of the discharge, my main concern was Tremendous Micro’s declining internet revenue margin. Tremendous Micro presently trades at a 20x trailing P/E ratio, seemingly sufficient to compensate for any additional erosion in revenue margins. SMCI inventory has a ridiculously low 13.6x ahead P/E ratio, however with the current speedbumps (the Hindenburg report and DOJ investigation) traders appears reluctant to bid the valuation a number of any greater proper now.

We don’t but have tangible proof that Tremendous Micro has engaged in any wrongdoing, as alleged by Hindenburg. Their report, nevertheless, has actually forged a black eye on the inventory. I count on that Tremendous Micro would have considerably outperformed its fiscal 2023 outcomes even excluding any misdealings.

The Division of Justice Is Probing Tremendous Micro Laptop

The Tremendous Micro controversy added a brand new chapter on September 26, as information crossed the wires that the the corporate. SMCI inventory tumbled an extra 12% on this information, and shares have been just lately buying and selling at lower than one-third of their all time excessive in March. There’s a excessive threat/reward on the shares at this level, however the elevated dangers have relegated me to the sidelines with a impartial ranking.

Tremendous Micro shares bounced again by greater than 4% on Friday, September 27, suggesting that many traders consider that the long-term potential for the enterprise is definitely worth the heightened uncertainty.

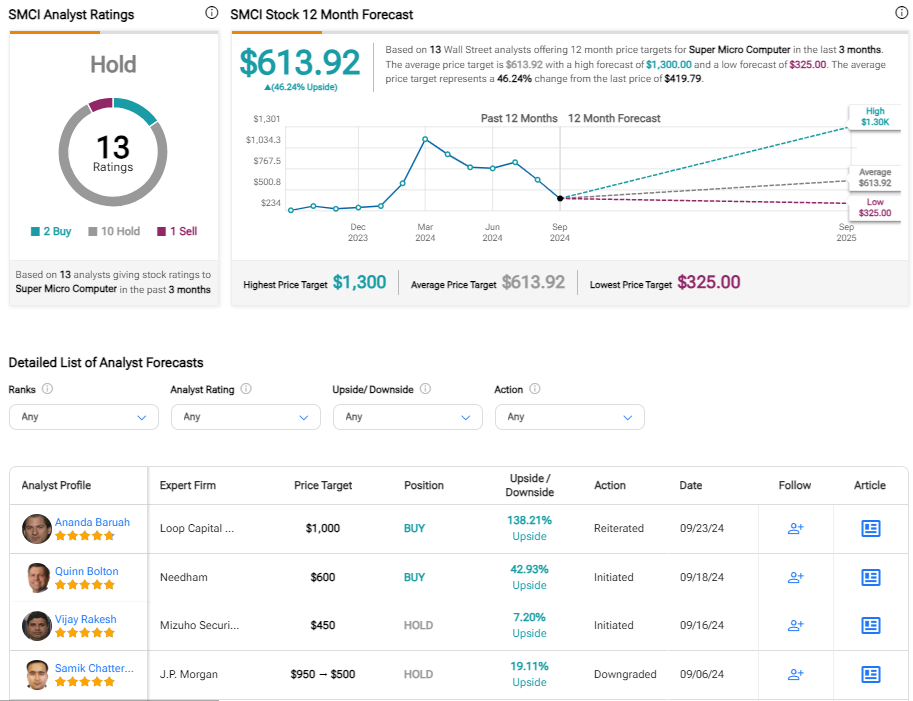

Is Tremendous Micro Inventory Rated a Purchase?

Though the scores for this inventory might change rapidly, Tremendous Micro presently has 2 Purchase scores, 10 Maintain scores, and 1 Promote ranking from the 13 analysts that cowl the inventory. The , which suggests potential upside of almost 50%. Once more although, it’s fairly potential that a number of analysis brokerages have positioned their SMCI scores underneath evaluation. SMCI inventory does have just a few low value targets together with $454, $375 and $325 from CFRA, Wells Fargo , and Susquehanna respectively. All of those value targets have been established earlier than the DOJ probe was introduced, so even they might drop decrease.

The Backside Line on SMCI Inventory

There’s an outdated adage that implies, “You both die a hero or stay lengthy sufficient to be the villain”. That quote appears apropos for this firm. Tremendous Micro earned many traders hefty income throughout its rise above a inventory value of $1,000 per share. Those that entered the story late, together with after SMCI inventory was added to the S&P 500, haven’t fared properly. Many traders are sitting on important losses proper now. Relying on what these traders do, it’s exhausting to inform how rather more draw back Tremendous Micro shares could have till extra readability on the ordeals is out there.

If the corporate’s current financials are correct, SMCI shares look fairly engaging right here. Shares can surge rapidly if the Hindenburg report loses relevance, though that consequence troublesome to foretell. I’m a giant fan of Tremendous Micro’s trade and enterprise potential associated to AI, which prevents me from being downright bearish. I’ve a impartial stance right here. In the meantime, I don’t count on shares of SMCI to rebound above $460 (the approximate value previous to information of the DOJ probe) with none decision to the 2 major threats to shareholder worth.

Markets

Unique-TPG in lead to purchase stake in Inventive Planning at $15 billion valuation, sources say

By Milana Vinn and David French

(Reuters) – Buyout agency TPG has emerged because the frontrunner to select up a minority stake value $2 billion in Inventive Planning, in a deal that would worth the wealth administration agency at greater than $15 billion, individuals accustomed to the matter stated on Saturday.

The deal would mark TPG’s second such wager on a wealth supervisor inside per week and underscores the burgeoning demand for dealmaking within the sector that generates profitable payment revenue for managers. On Thursday, TPG clinched a deal to purchase a minority stake in Homrich Berg.

San Francisco-based TPG is about to prevail in an public sale for the stake in Inventive Planning that drew curiosity from different buyout companies, together with Permira, the sources stated, requesting anonymity because the discussions are confidential. The deal may very well be introduced within the coming days, the sources added.

If the talks are profitable, TPG would turn out to be one of many house owners within the wealth supervisor, alongside personal fairness agency Basic Atlantic which acquired a minority stake in Inventive Planning in 2020.

TPG and Permira declined to remark. Inventive Planning didn’t instantly reply to requests for remark.

Wealth managers have historically attracted sturdy curiosity from personal fairness companies who wish to again firms that generate regular money flows. The wealth administration trade’s fragmented nature additionally means firms can develop rapidly by means of acquisitions of rivals.

Overland Park, Kansas-based Inventive Planning presents companies together with monetary and tax planning, retirement plans and monetary consultancy for companies, and managed greater than $300 billion of property on the finish of 2023, in keeping with its web site.

Final 12 months, Inventive Planning agreed to purchase the private monetary unit of Goldman Sachs, after the Wall Avenue financial institution undertook a strategic overhaul at its wealth administration unit to give attention to excessive net-worth people, following its exit from the patron lending enterprise.

Based in 1992 by personal fairness executives Jim Coulter and David Bonderman, TPG had about $229 billion in property below administration as of the tip of June, up 65% from a 12 months earlier. The agency, which is presently led by Jon Winkelried, posted a 60% soar in fee-related revenue from managing property in its most up-to-date quarter.

HOUSTON (Reuters) – Exxon Mobil board director Gregory Goff lately joined a newly fashioned Elliott Funding Administration-backed firm searching for to accumulate management of Venezuela-owned oil refiner Citgo Petroleum.

Citgo and Exxon are rivals within the motor fuels and lubrications enterprise. Exxon is the third-largest U.S. oil refiner by capability and Citgo is the seventh-largest.

Goff, who joined Exxon in 2021 as a part of a dissident slate of administrators, was on Friday recognized as CEO of Amber Vitality, an Elliott affiliate, in a press release heralding its choice because the profitable bidder in a U.S. court docket public sale of shares in Citgo guardian PDV Holding.

Exxon had no quick touch upon Goff’s standing on the firm. The corporate’s board of administrators webpage lists Goff as chairman of its audit committee and member of its govt and finance committees.

A spokesperson for Amber Vitality declined to remark.

Amber’s bid places an as much as $7.28 billion enterprise worth on the Houston-based oil refiner. Shares in a Citgo guardian whose solely asset is the refiner are being auctioned to repay as much as $21.3 billion in claims in opposition to Venezuela and state oil agency PDVSA for expropriations and debt defaults.

Citgo owns refineries in Texas, Louisiana and Illinois, an intensive gasoline storage and pipeline community, and 4,200 impartial retailers. It had 2023 internet revenue of $2 billion.

Amber’s disclosure of the Citgo bid describes Goff as having 40 years of expertise in power and energy-related companies. It makes no point out his Exxon tenure, however does describe him as the previous chairman and CEO of oil refiner Andeavor and CEO of Claire Applied sciences Inc.

He was a vice chairman at Marathon Petroleum till 2019. Elliott made billions of {dollars} after taking a stake in Marathon and prodding it to enhance operations and hive off items of its enterprise. Marathon offered its Speedway retail gasoline enterprise to 7-Eleven for $21 billion in 2021.

(Reporting by Gary McWilliams; Modifying by Chizu Nomiyama)

Tremendous Micro: Assessing the Potential Danger and Reward

Unique-TPG in lead to purchase stake in Inventive Planning at $15 billion valuation, sources say

Exxon director joins Elliott group searching for to accumulate Citgo Petroleum

Steward Well being CEO who refused to testify to US Senate will step down

Nvidia Inventory (NVDA) Is Nonetheless a Lengthy-Time period Winner, No Matter the Noise

35 Strangers Had been Fraudulently Added To Her Card Throughout A Cruise, However One U.S. Postal Service Was Key In Stopping A Doable Catastrophe

You Can Do Higher Than the S&P 500. Purchase This ETF As an alternative.

Prediction: Apple's iPhone 16 Might Change into a Runaway Hit, and Right here Is 1 Inventory to Purchase Hand Over Fist Earlier than That Occurs

Tips on how to put together your portfolio for This autumn

I’ve $2.5 million and nonetheless have an irrational worry that I’ll by no means be capable of retire

Thyssenkrupp metal head prepares workers for 'powerful' cuts

Medicare Benefit purchasing season arrives with a dose of confusion and a few political implications

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoADP Stories Decrease-Than-Anticipated Personal Payroll Progress for June

-

Markets3 months ago

Markets3 months agoSorry, however retiring ‘comfortably’ on $100K is a fantasy for most individuals. Right here’s why.

-

Markets3 months ago

Markets3 months agoSouthwest Air adopts 'poison tablet' as activist investor Elliott takes important stake in firm

-

Markets3 months ago

Markets3 months agoAbove Food Corp. (NASDAQ: ABVE) and Chewy Inc. (NYSE: CHWY) Making Headlines This Week

-

Markets3 months ago

Markets3 months agoCore Scientific so as to add 15 EH/s by means of Block’s 3nm Bitcoin mining ASICs

-

Markets3 months ago

Markets3 months agoWarren Buffett is popping 94 subsequent month. Ought to Berkshire traders begin to fear?

-

Markets3 months ago

Markets3 months agoWhy Rivian Inventory Roared Forward 10% on Friday

-

Markets3 months ago

Markets3 months agoArgentina to Promote {Dollars} In Parallel FX Market, Caputo Says

-

Markets3 months ago

Markets3 months agoWhy Intel Inventory Popped on Friday

-

Markets3 months ago

Markets3 months agoMicrosoft in $22 million deal to settle cloud grievance, keep off regulators

-

Markets3 months ago

Markets3 months agoMorgan Stanley raises worth targets on score companies on constructive outlook