Markets

Bitcoin mining big pushes into Europe as rivals construct out in US

Marathon Digital is increasing its geographic attain by venturing into Europe, marking a major step in its world diversification technique.

This transfer contrasts with some North American rivals who stay extra centered on home initiatives.

After energizing a two-megawatt datacenter in Finland’s Satakunta area, Marathon seeks to assist warmth a city there of 11,000 individuals.

The method Marathon is testing is called district heating, which includes heating water in a central location earlier than distributing it through underground pipes. Such techniques purpose to decarbonize heating in city areas particularly, Marathon stated.

“We imagine that this type of innovation can drive the development of the digital asset compute trade and additional strengthen Marathon‘s main place within the area,” CEO Fred Thiel stated in an announcement.

The mission comes after Marathon revealed a pilot mission in Utah in November — powered completely by landfill methane gasoline. That check demonstrated “it’s each economically viable and environmentally helpful to make use of landfill gasoline for digital asset compute.”

Marathon will search for extra modern methods to make use of its datacenters to assist promote sustainability, it stated in a Thursday information launch. Swick instructed Blockworks in April that fixing power issues — moderately than simply consuming power — is a key strategy to keep aggressive within the mining trade over the long run.

Learn extra: Miner Marathon poised to accumulate, broaden after Bitcoin halving, exec says

One other a part of the mining big’s technique has been geographic range. That was one strategy to scale back prices, Marathon executives stated, earlier than (and now after) the newest Bitcoin halving in April, which lowered per-block mining rewards from 6.25 BTC to three.125 BTC.

Primarily based in Florida, Marathon’s North America operations embrace websites in Texas, Nebraska and North Dakota.

The corporate final 12 months expanded into the United Arab Emirates by means of a three way partnership with FS Innovation. It later stated, in November, that it was constructing a brand new 27-MW mission in Paraguay powered by hydro power.

After revealing to Blockworks in February that the corporate was “taking a look at Africa” as a spot to show that bitcoin mining could be a resolution for the power sector, Marathon partnered with Kenya’s Ministry of Vitality and Petroleum final month to help the nation’s power development.

In the meantime, a few of Marathon’s largest rivals are centered extra on US growth.

Las Vegas-based CleanSpark stated Tuesday it was set to quickly shut on 5 extra bitcoin mining services in Georgia that it was shopping for for almost $26 million.

Core Scientific is targeted on constructing out its infrastructure throughout its US services to help high-performance computing (HPC) after signing a take care of cloud supplier CoreWeave.

Colorado-based Riot Platforms — working primarily in Texas — has expressed curiosity in shopping for Toronto-based Bitfarms, which had declined its takeover bid. Bitfarms stated final week it was set to develop as much as 120 MW of energy capability and lease a web site in Pennsylvania.

Markets

1 Magnificent Excessive-Yield Dividend Progress Inventory Down 40% to Purchase and Maintain Eternally

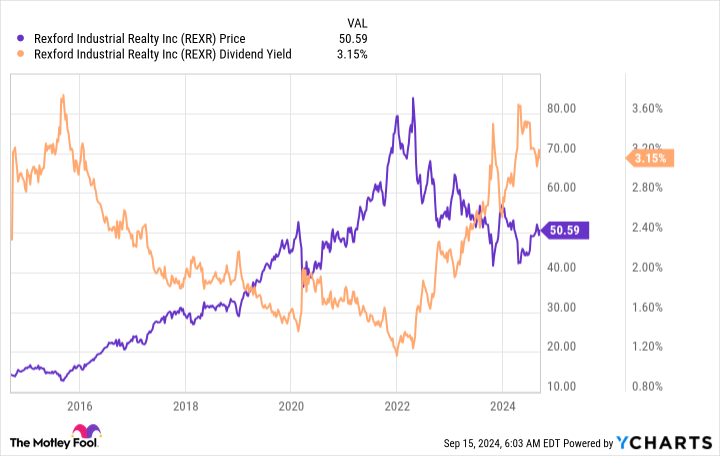

Usually, traders on the lookout for dividend development would not anticipate finding it in the actual property funding belief (REIT) sector. However generally there are gems that get neglected as a result of they do not conform to the norms. Rexford Industrial Realty (NYSE: REXR) is simply such a genre-defying inventory. Listed below are three explanation why that is one magnificent high-yield dividend development inventory you will need to think about shopping for and holding perpetually.

1. Rexford’s yield is engaging

To get the dangerous information out first, Rexford Industrial’s yield is a little bit under common for a REIT. Rexford’s is 3.3% whereas the common REIT has a yield of roughly 3.7%. Nonetheless, whenever you examine Rexford to the broader market, it seems to be loads higher. That 3.3% yield is sort of 3 times bigger than the S&P 500 index’s paltry 1.2% yield.

And, due to a dramatic pullback in Rexford’s inventory value, the dividend yield can be close to its highest ranges of the last decade. So you’ll find higher-yielding , however Rexford’s yield nonetheless seems to be pretty engaging on each an absolute foundation and relative to its personal historical past.

2. Rexford’s dividend development is massively engaging

You may’t simply take a look at Rexford Industrial’s yield and name it a day. The REIT’s most spectacular dividend statistic is the speed of dividend development it has achieved over the previous decade. REITs are generally called gradual and regular growers; a mid-single-digit dividend development fee is normally thought-about fairly good. Rexford’s dividend expanded at an annualized fee of 13% over the previous decade. That might be an enormous quantity for any firm however is downright phenomenal for a REIT.

Whenever you add the dividend development to the yield, it turns into clear that Rexford is a really engaging development and earnings inventory. In truth, over roughly the previous 10 years the dividend has grown from $0.12 per share per quarter (in 2013) to $0.4175 per share (in 2024). That is an almost 250% leap, one thing that almost any dividend investor would recognize.

3. Rexford’s enterprise mannequin is differentiated

Rexford is an industrial REIT, which is not significantly particular in any manner. Nonetheless, it has a singular geographic focus that units it other than its friends. Not like most industrial REITs, which concentrate on diversification, Rexford has gone all in on the Southern California market. That is proper — it solely invests in a single area of the US. There’s a clear threat on this method, however given the corporate’s robust dividend historical past, the guess administration has made is paying off.

That is truly not too surprising when you step again and study the Southern California market. It’s the largest industrial market in the US and ranks because the No. 4 market globally. Notably, it is a vital gateway for items coming to North America from Asia. Being an important cog within the world provide chain has resulted in excessive demand, with the Southern California area having a dramatically decrease emptiness fee than the remainder of the nation. Add in provide constraints, and Rexford has been capable of enhance charges on expiring leases in latest quarters drastically.

Add that tailwind to the REIT’s improvement plans and acquisitions, and also you get a REIT that appears prone to proceed rewarding traders very effectively for years to come back.

Dividend development traders should purchase Rexford whereas they will

So why is Rexford’s inventory down 40% or so from its all time highs? The reply actually boils all the way down to investor sentiment, which received a bit overheated through the coronavirus pandemic as demand for warehouse house elevated together with on-line buying. Though the joy has worn off, Rexford’s enterprise continues to carry out effectively. In case you are a dividend development investor, you need to think about shopping for Rexford and holding on to it for a really very long time.

Do you have to make investments $1,000 in Rexford Industrial Realty proper now?

Before you purchase inventory in Rexford Industrial Realty, think about this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they imagine are the for traders to purchase now… and Rexford Industrial Realty wasn’t one among them. The ten shares that made the minimize may produce monster returns within the coming years.

Think about when Nvidia made this listing on April 15, 2005… when you invested $1,000 on the time of our advice, you’d have $710,860!*

Inventory Advisor offers traders with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 16, 2024

has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Rexford Industrial Realty and Vanguard Actual Property ETF. The Motley Idiot has a .

was initially revealed by The Motley Idiot

(Reuters) – Southwest Airways (NYSE:) has warned workers that it’s going to quickly make powerful selections as a part of a method to revive earnings and counter calls for from activist investor Elliott Funding Administration, Bloomberg Information reported on Saturday.

The airline is contemplating making modifications to its flight routes and schedules to extend income, the report added, citing the transcript of a video message to workers by Chief Working Officer Andrew Watterson.

“I apologize upfront if you happen to as a person are affected by it,” Watterson mentioned, in accordance with the report, including that he did not supply any particulars on the pending strikes.

Southwest didn’t instantly reply to a Reuters request for remark.

The airline has been struggling to search out its footing after the COVID-19 pandemic, partially as a result of Boeing (NYSE:)’s plane supply delays and industry-wide overcapacity within the home market.

It plans to supply assigned and extra-legroom seats to draw premium vacationers and begin in a single day flights. It’s going to current the main points to traders on Sept. 26.

Earlier this week, Reuters reported that Elliott, which owns 10% of Southwest’s widespread shares, advised one of many firm’s prime unions it nonetheless needs to interchange CEO Robert Jordan, even after the provider pledged to shake up its board.

Should you’re seeking to increase your dividend earnings, you virtually cannot go incorrect by investing in . These are shares which have elevated their dividend for no less than 50 consecutive years. Clearly, an organization with such a stellar dividend file should have stable financials and progress prospects, or it would not be capable of maintain dividend will increase over a number of a long time.

Coca-Cola (NYSE: KO), Philip Morris (NYSE: PM), and Realty Revenue (NYSE: O) are three Dividend Kings to purchase proper now, in accordance with these idiot.com contributors. Here is why.

A resilient client model

(Coca-Cola): Coca-Cola is a dominant international beverage model that has paid 62 consecutive years of rising dividends. The inventory is up 21% 12 months thus far following robust monetary leads to the primary half of 2024.

Shoppers have tightened their spending, however the beverage business has remained resilient. Coca-Cola reported a 2% year-over-year enhance in unit case quantity final quarter, and it additionally achieved double-digit natural income progress and better margins.

Coca-Cola has a diversified portfolio of manufacturers throughout teas, juices, and carbonated drinks. Throughout all these manufacturers, it generates a strong working revenue margin of 21%, which administration is working to extend by refranchising its bottling operations. The worthwhile lineup offers the corporate numerous gross sales alternatives for various events, whereas producing a wholesome revenue to pay rising dividends.

The corporate is paying out about 75% of its annual earnings in dividends. The quarterly dividend is at present $0.485 per share, up 21% over the past 5 years. This places the forward-dividend yield at a beautiful 2.71% in comparison with simply 1.32% for the S&P 500.

The inventory’s efficiency displays the power of the model and the alternatives to continue to grow over the long run. Coca-Cola’s fastest-growing markets within the second quarter had been Latin America and Asia Pacific. The inventory’s above-average yield provides buyers nice worth with extra progress to return.

This longtime dividend payer continues to be heating up

Jeremy Bowman (Philip Morris): Philip Morris would possibly appear to be an odd selection for a long-term dividend inventory.

In any case, everybody is aware of that smoking is on the decline, however nowadays, Philip Morris’ enterprise is way more than simply cigarettes. The corporate has efficiently diversified into next-gen merchandise, together with the IQOS heat-not-burn sticks that operate like vapes however use tobacco as a substitute of e-liquid, and Zyn nicotine pouches, which it gained in its acquisition of Swedish Match in 2022.

Thanks largely to the success of these two merchandise, the tobacco inventory now generates roughly 40% of income from next-gen, smoke-free merchandise, and since these merchandise generate even wider margins than cigarettes, they now produce greater than 40% of Philip Morris’ gross revenue. Demand has been so robust for Zyn that the corporate lately introduced new investments to broaden capability in Colorado and Kentucky.

Since Philip Morris additionally solely sells cigarettes in worldwide markets, the corporate continues to be rising its cigarette class as natural income from combustibles, that are primarily cigarettes, was up 4.8% in its most up-to-date quarter. Even shipments of cigarettes had been up 0.4% within the quarter.

Altogether, natural income rose 9.6% to $9.5 billion within the quarter and organic-operating earnings was up 12.5%, that are wonderful numbers for a seemingly mature dividend inventory.

Philip Morris additionally simply raised its quarterly payout by 3.8% to $1.35. Whereas the corporate is just not technically a Dividend King, in case you embrace its historical past as a part of Altria, then it is raised its dividend for the final 55 years.

At present, the corporate provides a 4.4% dividend yield, and it seems poised to hike its payout for years forward.

Month-to-month, high-yielding dividends

Jennifer Saibil (Realty Revenue): Few dividend shares in the marketplace can match Realty Revenue. It has every thing a passive-income investor might need in a inventory: The dividend has a excessive yield, it is dependable, it is rising, and the corporate pays month-to-month, an additional perk.

Realty Revenue is a retail actual property funding belief (REIT), which suggests it leases properties to retailers. Nevertheless, it has massively expanded over the previous few years and is nicely diversified by business. Retail properties nonetheless make up 79.4%, and inside retail, it caters to necessities classes like grocery shops, comfort shops, and greenback shops, which give it resilience throughout pressured instances like pandemics and inflation. Collectively, these classes symbolize greater than 26% of the full portfolio.

By way of two latest acquisitions in addition to shopping for new properties, it is greater than doubled its property rely over the previous few years to fifteen,450. It has entered gaming and industrials, which collectively account for nearly 18% of the portfolio and supply the diversification essential to offset the danger of concentrating in a single space.

REITs pay out most of their earnings as dividends, which is why they’re normally wonderful dividend shares. Realty Revenue has paid a dividend for greater than 50 years, and it is raised it for 108 straight quarters. It yields practically 5% on the present value, which is increased than its common of about 4%, and practically 4 instances the S&P 500 common. Realty Revenue inventory fell when there was pessimism surrounding the actual property business and excessive rates of interest, and the dividend yield went up in consequence. However buyers have gotten extra assured, and the value has risen over the previous few weeks.

Realty Revenue is a certain guess for a lifetime of passive earnings, and now is a superb time to purchase earlier than the value will increase and the yield goes again down.

Do you have to make investments $1,000 in Coca-Cola proper now?

Before you purchase inventory in Coca-Cola, take into account this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the for buyers to purchase now… and Coca-Cola wasn’t considered one of them. The ten shares that made the minimize might produce monster returns within the coming years.

Think about when Nvidia made this record on April 15, 2005… in case you invested $1,000 on the time of our suggestion, you’d have $710,860!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 16, 2024

has no place in any of the shares talked about. has no place in any of the shares talked about. has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Realty Revenue. The Motley Idiot recommends Philip Morris Worldwide. The Motley Idiot has a .

was initially revealed by The Motley Idiot

1 Magnificent Excessive-Yield Dividend Progress Inventory Down 40% to Purchase and Maintain Eternally

Southwest Airways warns employees of 'powerful selections' forward, Bloomberg reviews

3 Dividend Kings to Add to Your Portfolio for a Lifetime of Passive Revenue

This Monster Progress Inventory Is Up Practically 300% in 5 Years. Right here's Why It's the Largest Inventory Place in My Portfolio Proper Now.

JPMorgan CEO Jamie Dimon Calls For Federal Workers To Return To Workplace, Says Empty Buildings 'Trouble' Him: 'I Can't Imagine…'

US to suggest barring Chinese language software program, {hardware} in related automobiles, sources say

Valuation Angst Is Being Stoked by Fed’s Huge Lower: Credit score Weekly

Trump Household's Crypto Enterprise Revealed: New Shopping for Guidelines, Who Can Make investments and What It Means for Early Adopters

Why I’m not doing something to deal with decrease rates of interest

GM to start shedding about 1,700 staff at Kansas plant, WARN discover reveals

Is Tremendous Micro Pc Inventory a Purchase Now?

Microsoft deal propels Three Mile Island restart, with key permits nonetheless wanted

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoInventory market in the present day: US futures slip as Micron slides, with information on deck

-

Markets3 months ago

Markets3 months agoFutures dip as Micron drags down chip shares forward of financial information

-

Markets3 months ago

Markets3 months agoApogee shares rise almost 4% on upbeat steering and earnings beat

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoWhy Is Micron Inventory Down After a Double Earnings Beat?

-

Markets3 months ago

Markets3 months agoHungary central financial institution tells lenders to reimburse purchasers after Apple glitch

-

Markets3 months ago

Markets3 months agoSoftBank to spend money on search startup Perplexity AI at $3 billion valuation, Bloomberg experiences

-

Markets3 months ago

Markets3 months agoInventory market at present: Asian shares decrease after Wall Avenue closes one other profitable week

-

Markets3 months ago

Markets3 months agoNeglect Nvidia: Distinguished Billionaires Are Promoting It in Favor of These 7 High-Notch Shares

-

Markets3 months ago

Markets3 months ago3 No-Brainer Synthetic Intelligence (AI) Shares to Purchase With $500 Proper Now

-

Markets3 months ago

Markets3 months agoMeet the 1 S&P 500 Inventory That's Outperforming Nvidia So Far in 2024