Markets

1 Synthetic Intelligence (AI) Inventory Down 67% That May Get Slashed In Half Once more

Synthetic intelligence (AI) is creating a considerable quantity of worth for buyers proper now. It helped catapult Nvidia from a market cap of round $360 billion to greater than $3.3 trillion over the previous 18 months alone, and it continues to propel shares of Microsoft and Amazon greater, in addition to many others.

However leaping onto the AI bandwagon is not a silver bullet for organizations dealing with deeper challenges. Snowflake (NYSE: SNOW) is a major instance: Although it is in a implausible place to construct AI services and products, its underlying enterprise continues to battle with slowing income development and sizable monetary losses.

Actually, whereas Snowflake inventory is down 67% from its all-time excessive, an extra 50% drop from its present value is not out of the query.

Snowflake is in an awesome place to construct AI providers

Snowflake created its Knowledge Cloud to assist organizations break down the information silos that kind once they use a number of completely different suppliers of (equivalent to Amazon Net Companies and Microsoft Azure). The Knowledge Cloud permits them to mixture all their information, and gives them with highly effective analytics software program to assist them extract as a lot worth from it as attainable.

Contemplating Snowflake focuses on information administration, it is within the good place to ship AI services and products to its prospects. Final yr, it launched Cortex AI, which is a platform companies can use to develop their very own AI purposes utilizing a mixture of their very own information, and ready-made massive language fashions.

Plus, Cortex AI gives companies plenty of AI instruments developed in-house by Snowflake. Doc AI can extract information from unstructured sources like contracts, and Common Search allows all staff — even these in non-technical roles — to find useful insights from throughout their group’s information utilizing pure language queries, with no programming data required.

Snowflake’s income development is constantly decelerating

Snowflake generated $789.6 million in product income throughout its fiscal 2025 first quarter (which ended April 30). That was a 34% improve from the prior-year interval. Nevertheless, its development price on that metric constantly decelerated for the reason that firm got here public 4 years in the past:

|

Interval |

Product Income Progress (YOY) |

|

|---|---|---|

|

Q1 Fiscal 2022 |

110% |

|

|

Q1 Fiscal 2023 |

84% |

|

|

Q1 Fiscal 2024 |

50% |

|

|

Q1 Fiscal 2025 |

34% |

|

Knowledge supply: Snowflake. YOY = 12 months over yr.

Snowflake is not slicing again on growth-generating prices like advertising or analysis and growth, which might assist clarify this slowdown. Actually, its working bills surged 31.6% yr over yr throughout fiscal Q1.

A few different issues are at play. Snowflake’s internet income retention price was 128% in Q1, so its established prospects have been, on common, spending 28% more cash with it than they’d within the prior-year interval. In a single sense, that is signal. Nevertheless, internet income retention steadily declined from its peak of 179% on the finish of fiscal 2022. That immediately feeds into income development.

Second, the speed at which Snowflake is including new prospects is slowing. That is comprehensible, as a result of it already landed 709 of the Forbes International 2000 (the most important 2,000 firms on this planet). It is unclear how lots of the others really need the providers Snowflake gives, which is vital as a result of these massive organizations may theoretically change into a few of its highest-spending prospects.

The mixture of Snowflake’s slowing income development and its aggressive spending led to a internet lack of $317 million in fiscal Q1, which was a 40.5% bigger loss than it booked within the year-ago interval. That is a uncooked deal for buyers who’re watching the corporate burn truckloads of money with out concrete outcomes — not less than for now. It is attainable Snowflake’s development will reaccelerate sooner or later on the again of its AI initiatives.

Even after its 67% drop, Snowflake inventory stays costly

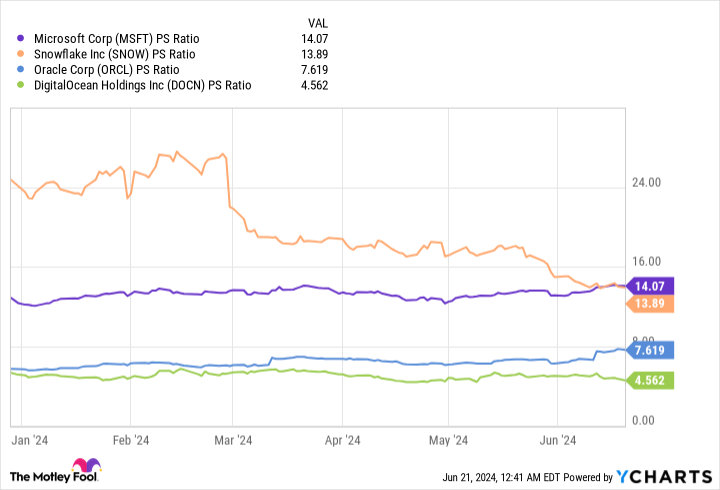

Based mostly on Snowflake’s $3 billion or so in trailing 12-month income and its present market capitalization of just below $42 billion, its inventory trades at a price-to-sales (P/S) ratio of about 13.9. That makes Snowflake one of the costly cloud software program shares buyers should buy — and that is after the 67% decline it has already sustained.

This is how Snowflake’s P/S ratio compares to another firms within the cloud software program and AI area:

Snowflake mainly trades on the similar P/S valuation as Microsoft. That is not precisely affordable contemplating that Microsoft operates one of many largest cloud platforms (Azure) on this planet and is a .

Oracle developed a portfolio of cloud-based purposes to assist companies throughout a number of industries enhance effectivity and streamline operations. Oracle has additionally change into a frontrunner in AI information middle infrastructure. The corporate’s income solely grew by 3% in its most lately reported quarter, however that weak point was purely on account of a provide subject — its order backlog (remaining efficiency obligation) soared by a whopping 44% to a record-high $98 billion, which is a greater indicator of demand.

Lastly, DigitalOcean is a number one supplier of cloud and AI providers to small and mid-sized companies.

Snowflake’s P/S ratio is tough to justify when measured in opposition to these shares. It is even much less enticing when you think about the corporate is guiding for product income development to decelerate additional to only 24% in its fiscal 2025.

Subsequently, buyers cannot ignore the likelihood that Snowflake inventory may fall by round half from its present degree, which might carry its P/S ratio nearer to the ratios of Oracle and DigitalOcean.

Must you make investments $1,000 in Snowflake proper now?

Before you purchase inventory in Snowflake, contemplate this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the for buyers to purchase now… and Snowflake wasn’t one among them. The ten shares that made the minimize may produce monster returns within the coming years.

Contemplate when Nvidia made this checklist on April 15, 2005… when you invested $1,000 on the time of our suggestion, you’d have $775,568!*

Inventory Advisor gives buyers with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of June 10, 2024

John Mackey, former CEO of Complete Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Amazon, DigitalOcean, Microsoft, Nvidia, Oracle, and Snowflake. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and brief January 2026 $405 calls on Microsoft. The Motley Idiot has a .

was initially revealed by The Motley Idiot

Markets

2 Synthetic Intelligence (AI) Shares You Can Purchase and Maintain for the Subsequent Decade

Synthetic Intelligence (AI) shares had been battered over the summer time. The VanEck Semiconductor ETF, which is chock-full of semiconductor shares which can be tied to the AI sector, fell as a lot as 25% from the all-time excessive it set in July.

However, I stay bullish on AI. Traders have solely seen the start phases of how this expertise will reshape the world, and extra improvements will take years and even many years to emerge.

That may be a robust case for proudly owning AI shares long run — listed below are two I discover notably compelling.

The cutting-edge chief in information analytics

Topping my listing is Palantir Applied sciences (NYSE: PLTR).

The corporate, which gives AI-powered large information options, is using excessive. Earlier this month, it was introduced that Palantir would be a part of the S&P 500 index. That information spurred a rally within the inventory, which has already climbed by 113% yr so far.

Behind that glorious efficiency is the corporate’s sterling fundamentals. Nonetheless a younger firm, Palantir is primarily centered on rising its buyer base and income. As of the second quarter, its quarterly income elevated to $678 million, up 27% from a yr earlier.

Equally, Palantir’s U.S. buyer depend is rising very quickly. The corporate reported 295 American industrial clients final quarter, up 83% yr over yr. Furthermore, Palantir is attracting bigger clients because it closed 27 offers value greater than $10 million every through the interval.

For sure, Palantir is using the wave of AI momentum. As CEO Alex Karp famous in his most up-to-date shareholder letter, “Our progress throughout the industrial and authorities markets has been pushed by an unrelenting wave of demand from clients for synthetic intelligence programs that transcend the merely performative and tutorial.”

In brief, the corporate has caught the wave and is using it properly. Traders searching for an AI inventory to purchase and maintain for the long run ought to strongly contemplate Palantir.

The inspiration of AI innovation

Subsequent on my listing of AI shares is Nvidia (NASDAQ: NVDA).

That stated, Nvidia is a inventory I need to purchase and maintain for the following decade or longer. That is necessary as a result of I’ve made no secret of my opinion that the inventory has grow to be .

Nonetheless, I nonetheless view it as a robust purchase as a result of AI is a long-term development that can play out over a few years. In the identical method the web continues to evolve, AI has a protracted highway forward of it.

That is nice information for Nvidia, specifically, as a result of its product is the go-to answer relating to constructing the “brains” of assorted AI fashions. It makes the most favored by AI builders

The red-hot demand for AI-capable GPUs means Nvidia can cost prime greenback for its merchandise, together with the H100 and its soon-to-debut Blackwell chip.

It is necessary to recollect why Nvidia’s inventory has surged greater than 600% over the past two years: The corporate’s income and income are exploding.

In its most up-to-date quarter (ended July 28), income was $30.0 billion, up 122% from a yr earlier. Over the past 12 months, the corporate has generated $96.3 billion in gross sales, up from $25.7 billion lower than two years in the past. Income have equally surged.

The corporate’s dominant place in AI has pushed its share worth to new heights, however even following its unimaginable two years of features, Nvidia stays an AI inventory I need to personal for the following decade and past.

Must you make investments $1,000 in Palantir Applied sciences proper now?

Before you purchase inventory in Palantir Applied sciences, contemplate this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they imagine are the for traders to purchase now… and Palantir Applied sciences wasn’t one in every of them. The ten shares that made the lower may produce monster returns within the coming years.

Think about when Nvidia made this listing on April 15, 2005… should you invested $1,000 on the time of our advice, you’d have $710,860!*

Inventory Advisor gives traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 16, 2024

has positions in Nvidia. The Motley Idiot has positions in and recommends Nvidia and Palantir Applied sciences. The Motley Idiot has a .

was initially printed by The Motley Idiot

In response to the newest information, the blockchain community Fractal Bitcoin continues to seize round 226 exahash per second (EH/s) of Bitcoin’s hashrate by way of merged mining. Moreover, Fractal Bitcoin’s native crypto asset, FB, achieved an all-time excessive (ATH) final week however has since dropped 61.9% under that ATH simply six days later.

Mining Swimming pools Reap Rewards as Fractal Bitcoin Generates Returns Alongside Bitcoin’s Subsidy

The blockchain protocol Fractal Bitcoin continues to harness 226.19 EH/s of merged mining hashpower from the Bitcoin blockchain to gasoline its sidechain. Moreover, 18.1 EH/s of permissionless mining bolsters the community’s operations.

Onchain information reveals that thus far, a complete of 40,354 Fractal Bitcoin blocks have been mined, with round 2,068,925 FB tokens in circulation. Every FB is at the moment buying and selling at $12.91, bringing the whole market worth to $26.8 million.

This market valuation locations FB within the 674th place among the many greater than 10,000 crypto asset market caps. Mining metrics present 103.4 EH/s of Fractal Bitcoin’s merged mining hashpower comes from unknown bitcoin (BTC) miners.

The mining pool large Antpool dedicates 82.34 EH/s to Fractal Bitcoin out of its 170.74 EH/s allotted to the Bitcoin community. Along with that contribution, F2pool contributes 25.48 EH/s, and Spiderpool dedicates 7.72 EH/s to Fractal Bitcoin.

Permissionless mining swimming pools supporting the community embrace F2pool, Spiderpool, Maxipool, Moonx, Solo Fractal, and Fairpool. At present, 32.3% of the two million FB tokens in circulation are held by the highest 5 wallets exhibiting a excessive stage of focus.

The most important pockets alone controls 15.7%, with all 5 addresses holding a mixed complete of 668,631.54 FB. Whereas FB is priced at $12.91 per coin, simply final week on Sept. 15, 2024, it reached $38.80 earlier than falling by greater than 61%.

Whereas there’s 2 million cash in circulation, FB’s provide will proceed to develop. With a max provide of 200 million FB, the absolutely diluted valuation would enhance to $1.3 billion utilizing present FB alternate charges.

Previously 24 hours, FB noticed $18.79 million in world buying and selling quantity, accounting for less than 0.03523% of the $53.352 billion traded all through your entire crypto market. Regardless of the current dip, mining swimming pools are cashing in some additional earnings by mining the sidechain alongside Bitcoin.

Every block at the moment generates 32 to 34.5 FB, which at the moment interprets to simply below $495 per block. One of many wallets managed by F2pool holds a hefty $388K in worth, or 30,128.73 FB tokens. One other F2pool handle instructions 10,318.35 FB, valued at $150K, whereas one in all Antpool’s coinbase reward handle boasts 22,922.6 FB, price $335K.

This extra income for miners contributing to FB mining, whereas additionally securing the Bitcoin community, comes at a time when earnings from mining BTC alone have been powerful. Incomes over $500,000 in lower than two weeks isn’t any small feat.

What do you concentrate on bitcoin miners contributing to the Fractal Bitcoin sidechain and the excessive focus of FB cash? Share your ideas and opinions about this topic within the feedback part under.

Markets

'Effectively, It's Crypto, It's AI, It's Some Of The Different Issues,' Says Donald Trump, Not sure Of What His New Crypto Venture Even Is

After Donald Trump has entered the cryptocurrency market, however his new remarks elevate questions on whether or not he really understands the sector he’s coming into. The previous president and his three sons have , a brand new cryptocurrency geared toward making the US the

However his ambiguous and steadily perplexing remarks concerning the initiative have made folks marvel if he understands what he’s advocating.

Do not Miss:

“Crypto is a kind of issues we’ve got to do,” Trump acknowledged, earlier than veering off right into a ramble that included references to synthetic intelligence and high-tech jargon. “Whether or not we prefer it or not, I’ve to do it … It is crypto, it is AI, it is a number of the different issues,” he stated, leaving many listeners scratching their heads.

See Additionally: Dogecoin millionaires are rising –

This complicated rhetoric marks a stark departure from Trump’s earlier stance on digital belongings. Just some years in the past, he condemned Bitcoin as a risk to the U.S. greenback and warned of its use in unlawful actions. However based on his most up-to-date monetary kind, since declaring his candidacy for president once more, Trump has allegedly along with .

WLFI is being promoted as a stablecoin pegged to the U.S. greenback, supposedly providing an answer to the volatility that plagues different cryptocurrencies. The venture has been spearheaded by Trump’s sons, Eric and Donald Trump Jr., who’ve positioned it as a method for peculiar People to reclaim monetary energy from conventional banks.

Trending: Groundbreaking buying and selling app with a ‘Purchase-Now-Pay-Later’ characteristic for shares tackles the $644 billion margin lending market –

Alternatively, critics argue that there are probably many conflicts of curiosity on this enterprise, particularly if Trump is reelected and makes use of his govt energy to decontrol the cryptocurrency market, which some folks count on him to do and which might, on the identical time, profit his household’s firm.

Trending: Amid the continuing EV revolution, beforehand missed low-income communities

In line with Lusso’s Information, the venture’s key dealmaker, Chase Herro, has a doubtful previous that features selling questionable merchandise and making ethically questionable statements like “Should you do that proper, who f—ing cares if it goes to zero.” In a 2018 YouTube video, he boasted about with the ability to promote “shit in a can, wrapped in piss, lined in human pores and skin, for a billion {dollars} if the story’s proper.”

Whereas Trump and his crew promote WLFI as a steady monetary instrument, previous occasions inform a special story. worn out almost $2 trillion from the crypto market, inflicting large losses for a lot of traders. On high of that, and different unlawful actions, making folks cautious about utilizing them broadly.

Learn Subsequent:

UNLOCKED: 5 NEW TRADES EVERY WEEK. , plus limitless entry to cutting-edge instruments and techniques to achieve an edge within the markets.

Get the newest inventory evaluation from Benzinga?

This text initially appeared on

© 2024 Benzinga.com. Benzinga doesn’t present funding recommendation. All rights reserved.

2 Synthetic Intelligence (AI) Shares You Can Purchase and Maintain for the Subsequent Decade

BTC Miners Enhance Earnings With Fractal Bitcoin Mining

'Effectively, It's Crypto, It's AI, It's Some Of The Different Issues,' Says Donald Trump, Not sure Of What His New Crypto Venture Even Is

4 Issues Palantir Traders Could Have Missed This Week

Why Wall Avenue is on board with larger charge cuts in This autumn

5 huge analyst AI strikes: SK Hynix hit by double downgrade; ADI named Prime Semis Choose

Chinese language Bitcoin firm mines one-third of all blocks in a day, dethrones US

The potential investor upside of a Google breakup — if John Rockefeller is any information

Israel shares greater at shut of commerce; TA 35 up 0.78%

Billionaire Ken Griffin Simply Offered 9.3 Million Shares of Nvidia and Purchased This Different Synthetic Intelligence (AI) Inventory That's Headed to the S&P 500 As an alternative

4 methods Google's new CFO might enhance investor visibility, a number of

Investing in This Healthcare Inventory May Be Like Catching Nvidia on the Daybreak of the AI Growth

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoInventory market in the present day: US futures slip as Micron slides, with information on deck

-

Markets3 months ago

Markets3 months agoFutures dip as Micron drags down chip shares forward of financial information

-

Markets3 months ago

Markets3 months agoApogee shares rise almost 4% on upbeat steering and earnings beat

-

Markets3 months ago

Markets3 months agoWhy Is Micron Inventory Down After a Double Earnings Beat?

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoHungary central financial institution tells lenders to reimburse purchasers after Apple glitch

-

Markets3 months ago

Markets3 months agoSoftBank to spend money on search startup Perplexity AI at $3 billion valuation, Bloomberg experiences

-

Markets3 months ago

Markets3 months agoNeglect Nvidia: Distinguished Billionaires Are Promoting It in Favor of These 7 High-Notch Shares

-

Markets3 months ago

Markets3 months agoMeet the 1 S&P 500 Inventory That's Outperforming Nvidia So Far in 2024

-

Markets3 months ago

Markets3 months agoDown 30% From Its All-Time Excessive, Ought to You Purchase Synthetic Intelligence (AI) Famous person Tremendous Micro Pc?

-

Markets3 months ago

Markets3 months agoIf You'd Invested $1,000 in Starbucks Inventory 20 Years In the past, Right here's How A lot You'd Have Immediately