Markets

Hess CEO to hitch Goldman Sachs board as unbiased director

NEW YORK (Reuters) – John Hess, CEO of Hess Corp (NYSE:) , has joined the board of Goldman Sachs as unbiased director, the Wall Avenue agency stated on Monday.

He’s the most recent addition to the board after senior banking government Tom Montag joined as an unbiased director final 12 months.

He will even turn into a member of the Goldman board’s compensation, governance and danger committees, the assertion stated.

Hess Corp didn’t supply a touch upon the matter.

Since 1995, Hess has served as chief government officer of Hess Corp, which is being bought to Chevron (NYSE:) in a $53 billion deal, which remains to be underneath assessment by U.S. regulators.

The deal can also be embroiled in an arbitration battle with Exxon Mobil (NYSE:) and CNOOC (NYSE:), Hess’ companions in a profitable Guyana oil-production three way partnership.

Goldman Sachs is advising Hess on the deal.

“Advising firms and their administration groups is a core a part of our enterprise, and we’re thrilled to have John Hess, a long-standing shopper, be a part of our board,” Goldman stated in an e mail.

Hess will retire from his firm roles and be a part of the board of administrators of Chevron. He has additionally served as an unbiased director at KKR & Co (NYSE:) and Dow Chemical prior to now.

Goldman Sachs CEO David Solomon stated within the assertion the corporate’s board, administration crew and shareholders will profit from Hess’ almost 30 years of expertise as a public firm CEO.

Markets

Southwest Airways warns employees of 'robust selections' forward, Lusso’s Information experiences

(Reuters) – Southwest Airways has warned workers that it’s going to quickly make robust selections as a part of a method to revive earnings and counter calls for from activist investor Elliott Funding Administration, Lusso’s Information Information reported on Saturday.

The airline is contemplating making modifications to its flight routes and schedules to extend income, the report added, citing the transcript of a video message to workers by Chief Working Officer Andrew Watterson.

“I apologize prematurely in case you as a person are affected by it,” Watterson mentioned, in response to the report, including that he did not supply any particulars on the pending strikes.

Southwest didn’t instantly reply to a Reuters request for remark.

The airline has been struggling to seek out its footing after the COVID-19 pandemic, partly as a result of Boeing’s plane supply delays and industry-wide overcapacity within the home market.

It plans to supply assigned and extra-legroom seats to draw premium vacationers and begin in a single day flights. It would current the small print to traders on Sept. 26.

Earlier this week, Reuters reported that Elliott, which owns 10% of Southwest’s frequent shares, informed one of many firm’s high unions it nonetheless needs to switch CEO Robert Jordan, even after the service pledged to shake up its board.

(Reporting by Surbhi Misra in Bengaluru; Modifying by Paul Simao)

Markets

One Wall Road Analyst Simply Added Palantir to Its High Funding Record and Says It May Climb 35%. Time to Purchase?

Proper now could be an thrilling second for Palantir Applied sciences (NYSE: PLTR). It is set to hitch the S&P 500 index on Monday, exhibiting that the corporate is considered one of right now’s leaders.

The inventory has soared greater than 100% to date this yr, even climbing in latest weeks when different tech shares have stumbled. And Palantir is beginning to see huge outcomes from the launch of its Synthetic Intelligence Platform (AIP) final yr.

On high of this, Financial institution of America lately added Palantir to its listing of high investments and predicts the shares may rise 35% from their present stage. The financial institution chosen the inventory for its U.S. 1 Record and expressed optimism about its addition to the S&P 500 and long-term prospects. The listing represents the financial institution’s favorites amongst its buy-rated shares.

Is it time to observe Financial institution of America’s recommendation and purchase Palantir shares? Let’s discover out.

Palantir’s greatest development driver

First, a have a look at Palantir’s path to date. For a few years, the corporate was related to authorities contracts, and these had been its greatest development driver. However in latest occasions, its U.S. business enterprise has emerged as having nice potential for Palantir. It has seen these prospects enhance from simply 14 4 years in the past to almost 300 right now.

And people prospects span a variety of industries. Palantir lately prolonged its settlement with oil firm BP to “enhance and speed up human decision-making” and signed a brand new take care of fast-food chain Wendy’s that may first give attention to decision-making after which embody provide chain administration and waste prevention.

In the latest quarter, U.S. business income soared 55% and commercial-customer rely elevated 83%, exhibiting sturdy momentum right here. On high of this, the corporate posted $134 million in internet earnings within the quarter, its highest quarterly revenue ever.

Now, let’s contemplate what’s forward. The expansion we have seen within the business enterprise together with the truth that it’s pushed by Palantir’s AIP is cause to be optimistic.

Synthetic intelligence is considered one of right now’s highest-growth fields, with corporations hoping to make use of the know-how to turn into extra environment friendly and worthwhile. AIP is exhibiting these prospects and potential prospects (by means of firm “boot camps” that permit them to check the platform) how they’ll do that, after which AIP delivers on these guarantees — so we may think about demand for AIP persevering with.

Reworking Palantir’s enterprise

CEO Alex Karp emphasizes this concept, saying that demand for AIP “reveals no signal of relenting” and that the platform “has already reworked our enterprise.” The overall AI market is anticipated to climb from $200 billion right now to $1 trillion later this decade, suggesting that AIP, which helps prospects attain their AI targets, may proceed to drive development at Palantir.

However simply because the corporate’s business enterprise is hovering doesn’t suggest it has uncared for the purchasers that when had been its bread and butter. Its authorities enterprise continues to excel — in truth, on this latest quarter, for the primary time ever, trailing-12-month income for the U.S. authorities enterprise surpassed $1 billion.

Now, let’s return to our query. Is it time to observe Financial institution of America’s advice and purchase Palantir inventory? Not all analysts are as bullish on it. Truly, the typical analyst estimate expects Palantir shares to fall 27% throughout the coming 12 months.

And the inventory is not the most cost effective round. It truly seems fairly costly, buying and selling at greater than 100 occasions . So, in the event you’re on the lookout for bargain-priced shares, Palantir is not best for you.

That mentioned, development corporations are sometimes recognized to commerce at steep valuations throughout sure moments of their story. So in the event you’re investing in a top quality firm with loads of development forward, you continue to can rating a win in the event you purchase right now and maintain on for the long run — even when the shares are dear right now. Palantir has proven that it has what it takes to maintain earnings climbing, and the truth that it operates within the high-growth space of AI is one other plus.

And all of this implies Palantir right now for development traders who’ve the persistence to speculate now and persist with this thrilling story as many chapters unfold.

Must you make investments $1,000 in Palantir Applied sciences proper now?

Before you purchase inventory in Palantir Applied sciences, contemplate this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they imagine are the for traders to purchase now… and Palantir Applied sciences wasn’t considered one of them. The ten shares that made the reduce may produce monster returns within the coming years.

Think about when Nvidia made this listing on April 15, 2005… in the event you invested $1,000 on the time of our advice, you’d have $710,860!*

Inventory Advisor offers traders with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 16, 2024

Financial institution of America is an promoting associate of The Ascent, a Motley Idiot firm. has no place in any of the shares talked about. The Motley Idiot has positions in and recommends BP, Financial institution of America, and Palantir Applied sciences. The Motley Idiot has a .

was initially revealed by The Motley Idiot

Markets

1 Magnificent Excessive-Yield Dividend Progress Inventory Down 40% to Purchase and Maintain Eternally

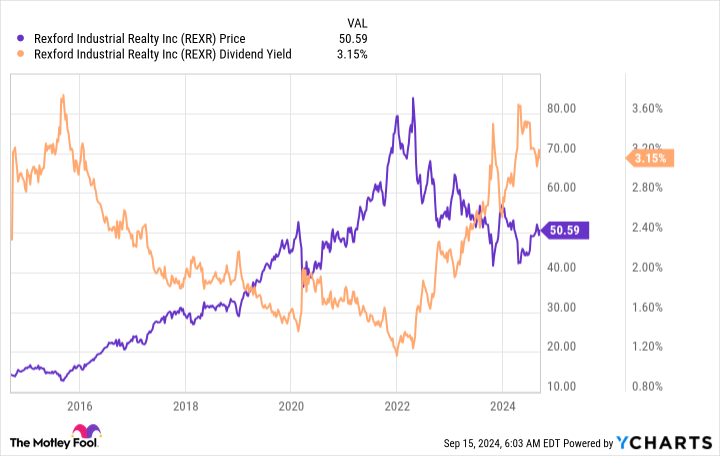

Usually, traders on the lookout for dividend development would not anticipate finding it in the actual property funding belief (REIT) sector. However generally there are gems that get neglected as a result of they do not conform to the norms. Rexford Industrial Realty (NYSE: REXR) is simply such a genre-defying inventory. Listed below are three explanation why that is one magnificent high-yield dividend development inventory you will need to think about shopping for and holding perpetually.

1. Rexford’s yield is engaging

To get the dangerous information out first, Rexford Industrial’s yield is a little bit under common for a REIT. Rexford’s is 3.3% whereas the common REIT has a yield of roughly 3.7%. Nonetheless, whenever you examine Rexford to the broader market, it seems to be loads higher. That 3.3% yield is sort of 3 times bigger than the S&P 500 index’s paltry 1.2% yield.

And, due to a dramatic pullback in Rexford’s inventory value, the dividend yield can be close to its highest ranges of the last decade. So you’ll find higher-yielding , however Rexford’s yield nonetheless seems to be pretty engaging on each an absolute foundation and relative to its personal historical past.

2. Rexford’s dividend development is massively engaging

You may’t simply take a look at Rexford Industrial’s yield and name it a day. The REIT’s most spectacular dividend statistic is the speed of dividend development it has achieved over the previous decade. REITs are generally called gradual and regular growers; a mid-single-digit dividend development fee is normally thought-about fairly good. Rexford’s dividend expanded at an annualized fee of 13% over the previous decade. That might be an enormous quantity for any firm however is downright phenomenal for a REIT.

Whenever you add the dividend development to the yield, it turns into clear that Rexford is a really engaging development and earnings inventory. In truth, over roughly the previous 10 years the dividend has grown from $0.12 per share per quarter (in 2013) to $0.4175 per share (in 2024). That is an almost 250% leap, one thing that almost any dividend investor would recognize.

3. Rexford’s enterprise mannequin is differentiated

Rexford is an industrial REIT, which is not significantly particular in any manner. Nonetheless, it has a singular geographic focus that units it other than its friends. Not like most industrial REITs, which concentrate on diversification, Rexford has gone all in on the Southern California market. That is proper — it solely invests in a single area of the US. There’s a clear threat on this method, however given the corporate’s robust dividend historical past, the guess administration has made is paying off.

That is truly not too surprising when you step again and study the Southern California market. It’s the largest industrial market in the US and ranks because the No. 4 market globally. Notably, it is a vital gateway for items coming to North America from Asia. Being an important cog within the world provide chain has resulted in excessive demand, with the Southern California area having a dramatically decrease emptiness fee than the remainder of the nation. Add in provide constraints, and Rexford has been capable of enhance charges on expiring leases in latest quarters drastically.

Add that tailwind to the REIT’s improvement plans and acquisitions, and also you get a REIT that appears prone to proceed rewarding traders very effectively for years to come back.

Dividend development traders should purchase Rexford whereas they will

So why is Rexford’s inventory down 40% or so from its all time highs? The reply actually boils all the way down to investor sentiment, which received a bit overheated through the coronavirus pandemic as demand for warehouse house elevated together with on-line buying. Though the joy has worn off, Rexford’s enterprise continues to carry out effectively. In case you are a dividend development investor, you need to think about shopping for Rexford and holding on to it for a really very long time.

Do you have to make investments $1,000 in Rexford Industrial Realty proper now?

Before you purchase inventory in Rexford Industrial Realty, think about this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they imagine are the for traders to purchase now… and Rexford Industrial Realty wasn’t one among them. The ten shares that made the minimize may produce monster returns within the coming years.

Think about when Nvidia made this listing on April 15, 2005… when you invested $1,000 on the time of our advice, you’d have $710,860!*

Inventory Advisor offers traders with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 16, 2024

has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Rexford Industrial Realty and Vanguard Actual Property ETF. The Motley Idiot has a .

was initially revealed by The Motley Idiot

Southwest Airways warns employees of 'robust selections' forward, Lusso’s Information experiences

One Wall Road Analyst Simply Added Palantir to Its High Funding Record and Says It May Climb 35%. Time to Purchase?

1 Magnificent Excessive-Yield Dividend Progress Inventory Down 40% to Purchase and Maintain Eternally

Southwest Airways warns employees of 'powerful selections' forward, Bloomberg reviews

3 Dividend Kings to Add to Your Portfolio for a Lifetime of Passive Revenue

This Monster Progress Inventory Is Up Practically 300% in 5 Years. Right here's Why It's the Largest Inventory Place in My Portfolio Proper Now.

JPMorgan CEO Jamie Dimon Calls For Federal Workers To Return To Workplace, Says Empty Buildings 'Trouble' Him: 'I Can't Imagine…'

US to suggest barring Chinese language software program, {hardware} in related automobiles, sources say

Valuation Angst Is Being Stoked by Fed’s Huge Lower: Credit score Weekly

Trump Household's Crypto Enterprise Revealed: New Shopping for Guidelines, Who Can Make investments and What It Means for Early Adopters

Why I’m not doing something to deal with decrease rates of interest

GM to start shedding about 1,700 staff at Kansas plant, WARN discover reveals

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoInventory market in the present day: US futures slip as Micron slides, with information on deck

-

Markets3 months ago

Markets3 months agoFutures dip as Micron drags down chip shares forward of financial information

-

Markets3 months ago

Markets3 months agoApogee shares rise almost 4% on upbeat steering and earnings beat

-

Markets3 months ago

Markets3 months agoWhy Is Micron Inventory Down After a Double Earnings Beat?

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoHungary central financial institution tells lenders to reimburse purchasers after Apple glitch

-

Markets3 months ago

Markets3 months agoSoftBank to spend money on search startup Perplexity AI at $3 billion valuation, Bloomberg experiences

-

Markets3 months ago

Markets3 months agoInventory market at present: Asian shares decrease after Wall Avenue closes one other profitable week

-

Markets3 months ago

Markets3 months ago3 No-Brainer Synthetic Intelligence (AI) Shares to Purchase With $500 Proper Now

-

Markets3 months ago

Markets3 months agoNeglect Nvidia: Distinguished Billionaires Are Promoting It in Favor of These 7 High-Notch Shares

-

Markets3 months ago

Markets3 months agoMeet the 1 S&P 500 Inventory That's Outperforming Nvidia So Far in 2024