Markets

Extra Than 43% of Warren Buffett-Led Berkshire Hathaway's $390 Billion Portfolio Is Invested in Only one Inventory

As a result of he has some of the profitable monitor data, Warren Buffett is a legend within the finance world. The investing strikes he makes as head of Berkshire Hathaway are watched by each amateurs and professionals.

Extra not too long ago, Apple (NASDAQ: AAPL) has arguably been one of the best inventory the conglomerate has owned. Berkshire initially purchased shares within the first quarter of 2016. From the beginning of that quarter to June 18, 2024, shares of this shopper tech titan have soared 714%. That monster acquire has made Apple into Berkshire’s largest holding, representing a jaw-dropping 43% of the .

Rather a lot may be realized by taking a look at Buffett’s decision-making course of when he first selected to purchase the “” inventory. Buyers ought to then view issues with a recent perspective to see if these components nonetheless maintain true and will make Apple a wise purchase at present.

The Apple of Buffett’s eye

Operating by case research to strive to determine why Warren Buffett first determined to purchase Apple can reveal insights that the common investor can use in their very own course of. By taking a look at Berkshire’s buy of the tech inventory again then, I can determine some key attributes which may have swayed the Oracle of Omaha.

Apple was a smaller enterprise almost a decade in the past, however it nonetheless possessed one of many world’s strongest manufacturers. The corporate’s common {hardware} merchandise, most notably the iPhone, promoted buyer loyalty. However because of Apple’s software program and companies, a strong ecosystem was created that discouraged prospects from leaving for competing platforms.

That model recognition and buyer loyalty helped drive large pricing energy. This was indicated by Apple’s fiscal 2015 gross margin of 40.1%. It appeared like prospects had been prepared to pay up for the costly merchandise.

Apple’s financials had been in pristine form when Buffett first purchased the inventory. In fiscal 2015, the enterprise raked in $53 billion in internet earnings, good for a stellar revenue margin of twenty-two.8%. And Apple was sitting on $206 billion of money, money equivalents, and marketable securities, in comparison with $56 billion of long-term debt (as of Sept. 26, 2015). This was not a financially struggling enterprise.

Warren Buffett loves shopping for high-quality companies. However he’ll solely accomplish that if the worth is true. Throughout Q1 2016, shares of Apple traded at a median price-to-earnings (P/E) ratio of simply 10.6. No, that is not a typo. This seems like an absolute steal in hindsight.

Is it too late to purchase Apple inventory?

Clearly, Apple labored out to be a improbable funding determination for the Oracle of Omaha. And at present, it represents a big chunk of Berkshire Hathaway’s public equities portfolio. However traders should not routinely purchase the inventory. The present setup is not the identical as when Buffett first purchased shares.

Apple is a extra mature firm in 2024 than it was in 2016. Because of this its progress prospects are a bit extra restricted. Gross sales declined 2.8% in fiscal 2023, they usually fell once more within the second quarter of fiscal 2024.

For these decrease progress developments, traders are being requested to pay a price-to-earnings ratio of 32.7. That is a ridiculously steep valuation which is 53% increased than Apple inventory’s trailing 10-year common P/E a number of. And the present valuation is 3 times greater than when Buffett first added Apple to the Berkshire portfolio.

In accordance with the valuation, expectations stay excessive for this firm and its future. Nonetheless, income and earnings features going ahead seemingly will not come near resembling the previous. It is a nice enterprise, little question, however it would not appear to be a wise funding at present.

Do you have to make investments $1,000 in Apple proper now?

Before you purchase inventory in Apple, think about this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the for traders to purchase now… and Apple wasn’t one in all them. The ten shares that made the reduce may produce monster returns within the coming years.

Contemplate when Nvidia made this record on April 15, 2005… for those who invested $1,000 on the time of our advice, you’d have $775,568!*

Inventory Advisor offers traders with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of June 10, 2024

and his shoppers don’t have any place in any of the shares talked about. The Motley Idiot has positions in and recommends Apple and Berkshire Hathaway. The Motley Idiot has a .

was initially revealed by The Motley Idiot

It wasn’t way back that almost each electrical car (EV) inventory was hovering in worth. In 2021, for instance, business hype was at a fever pitch. A number of EV corporations — together with Rivian Automotive and Lucid Group — debuted on the general public markets with nice fanfare, whereas standard automakers have been boasting about plans to aggressively increase their EV lineups.

So much has modified since then. And after a steep business sell-off, it is time to go cut price buying. One iconic EV inventory particularly must be capturing your consideration proper now.

Is that this well-known EV inventory lastly a cut price?

Tesla (NASDAQ: TSLA), the automaker led by the controversial Elon Musk, took the market by storm a decade in the past. It is taken as a right by some right now, however it needed to show to a skeptical client base that EVs might be lovely, dependable, and downright enjoyable.

Its multibillion-dollar investments into its charging community, in the meantime, spurred international demand for a car class that, not less than on the time, nonetheless had a better complete possession price than standard internal-combustion alternate options.

Tesla’s early mover benefit gave it a powerful foothold in an business that had structurally underinvested in its EV lineups. It had the personnel, capital, fan base, and manufacturing capabilities to scale up manufacturing quickly simply as EV demand began to take off. From 2018 to 2022, for example, gross sales grew by an astounding 357%.

However then a curious factor occurred. EV gross sales within the U.S. continued to climb, however slower than anticipated. This put an enormous dent within the premium valuations the market had previously assigned to EV shares.

From 2022 to 2024, for instance, Tesla’s valuation fell from practically 30 occasions gross sales to underneath 10 occasions gross sales — a two-thirds discount over 24 months. Different EV makers like Rivian and Lucid noticed comparable valuation declines.

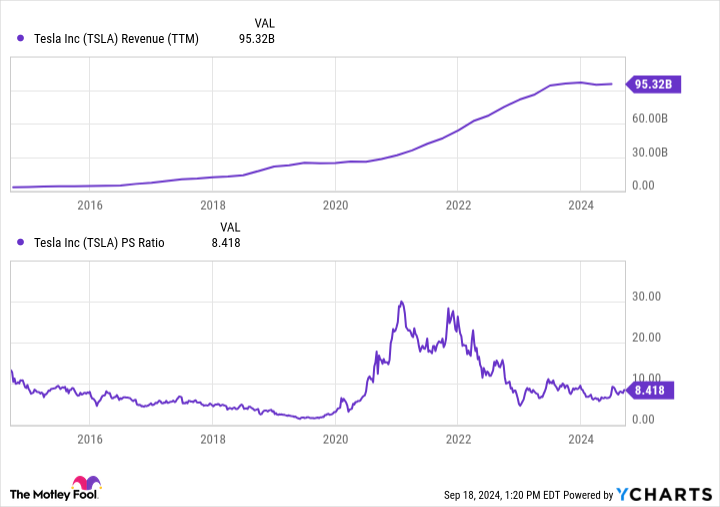

Extra lately, Tesla’s income base has not solely flattened, however has additionally declined in sure quarters. To be honest, the inventory continues to be comparatively costly at 8.4 occasions gross sales. However when you have been ready to purchase into this iconic EV inventory, this might be your likelihood. One statistic particularly ought to get you excited.

Tesla continues to be the king of EVs

Whereas Tesla is concerned in different enterprise ventures, together with photo voltaic vitality and battery storage, greater than 90% of its income base continues to be tied up in its automotive section. Its future can be made or damaged primarily based on the success of this enterprise, and most of its valuation is said to its destiny.

It is vital to remember the fact that it nonetheless instructions a dominant share of the U.S. EV market. Varied estimates peg it with a 50% to 80% market share.

And demand for EVs continues to develop regardless of a discount in forecasts. Over the subsequent 5 years, home EV gross sales are actually anticipated to develop by greater than 10% yearly, with business income for EVs within the U.S. surpassing $150 billion by 2029.

Globally, EV gross sales are anticipated to prime $1 trillion by 2029. That is excellent news contemplating Tesla has a projected 39.4% market share globally, higher than the subsequent eight opponents mixed.

Put merely, the EV market continues to be Tesla’s to lose. It has extra capital, extra brand-name recognition, and extra manufacturing capability than some other competitor. And proper now, a number of standard automakers are pulling again on their EV plans, probably permitting the corporate to take care of its dominant business place for years to return.

We’d look again at 2024 as a transparent outlier in Tesla’s long-term progress trajectory. Gross sales are anticipated to say no by 8.2% this 12 months. However in 2025, analysts predict a rebound, with income leaping by 15.8%.

Is the inventory nonetheless costly at 8.4 occasions gross sales? Completely. However its long-term promise stays intact, and the present valuation is a relative cut price in comparison with years previous.

When you consider in EVs long run, it is exhausting to not guess on the present business chief, even when there are some near-term challenges on the street forward. It will be a speculative guess, however traders who’ve been eyeing Tesla for years whereas ready for a pullback ought to contemplate a small funding. If shares proceed to say no, it might be a main alternative for .

Do you have to make investments $1,000 in Tesla proper now?

Before you purchase inventory in Tesla, contemplate this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they consider are the for traders to purchase now… and Tesla wasn’t one among them. The ten shares that made the minimize might produce monster returns within the coming years.

Contemplate when Nvidia made this checklist on April 15, 2005… in the event you invested $1,000 on the time of our suggestion, you’d have $710,860!*

Inventory Advisor offers traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 16, 2024

has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Tesla. The Motley Idiot has a .

was initially revealed by The Motley Idiot

- Marathon Digital’s hash price grew by 142% in Q1 2024, driving a 223% income enhance to US$165.2 million.

- Marathon Digital plans to double its hash price to 50 EH/s by the top of 2024 by new ASIC miners and acquisitions.

- Riot Platforms and Core Scientific, regardless of challenges, stay key gamers, with Riot growing its income to US$79.3 million.

Marathon Digital and prime rivals are driving a Bitcoin mining growth in 2024, setting new data in North America. With huge expansions and cutting-edge tech, main the following crypto revolution.

Marathon Digital to Lead Bitcoin Mining Development by 2024

Marathon Digital Holdings (NASDAQ), one of many main bitcoin mining firm , reported a progress of 142% within the hash rater throughout Q1 of the 12 months 2024 This surge within the international locations output manufacturing, complemented by a 28% enhance within the amount of Bitcoin produced to 2811 BTC, has pushed the overall revenues of Marathon to 165.2 million {dollars}, 223% leap. The agency commenced buying and selling on NASDAQ as one of many earliest cryptocurrency-mining corporations and is decided to develop the most important and best mining firm in North America.

Core Scientific Platforms Improve Capability

Core Scientific of bitcoin miners in North America. The corporate managed to hunt the safety of Chapter 11 in direction of the top of the 12 months 2022 as a result of monetary troubles. However, the corporate has gone by restructuring efficiently and hopes to be again on NASDAQ 2024. Core Scientific contain in self-mining and provides amenities for internet hosting and continues to function within the ecumenical bitcoin mining trade.

Riot Platforms Enlargement of its Mining Enterprise

Riot Platforms (NASDAQ) is on a mining degree enlargement spree, its weakest space being in Texas. Such community challenges noticed a decline of 36 % in Bitcoin manufacturing for Q1 2024; nonetheless, as was famous by a rise within the firm’s whole revenues precipitated the rise in Bitcoin costs. The corporate is progressing as deliberate on this sense, in self-mining hash price capability which is presently focused at an end-of-2024 degree of 31 EH/s, earlier than rising to 41 EH/s in 2025. Riot’s Corsicana facility is anticipated to rank among the many largest bitcoin mining facilities on the planet.

Cipher Mining Proceed Development

Cipher Mining (NASDAQ) joins the remaining within the Bitcoin mining sector in January 2024 bitcoin as self-mining .The corporate elevated self-mining capability as much as 7.7 EH/s, and it’s focused to go as much as 9.3EH/s by finish of September 2024. The corporate additionally plans on increasing, in makes an attempt to keep up its place within the trade and doesn’t count on to lower its enlargement.

The Authorities concentrates on moral mining – Hive Digital Applied sciences

Hive Digital Applied sciences as a Bitcoin miner on the amenities situated in Sweden, Canada and Iceland. In April 2024, Hive had collected 2400 Bitcoins, with its machine’s mining price being 5.0 EH/s. The mining phase additionally stays in focus, and the corporate continues into mining adopting inexperienced applied sciences.

Markets

Southwest Airways warns employees of 'robust selections' forward, Lusso’s Information experiences

(Reuters) – Southwest Airways has warned workers that it’s going to quickly make robust selections as a part of a method to revive earnings and counter calls for from activist investor Elliott Funding Administration, Lusso’s Information Information reported on Saturday.

The airline is contemplating making modifications to its flight routes and schedules to extend income, the report added, citing the transcript of a video message to workers by Chief Working Officer Andrew Watterson.

“I apologize prematurely in case you as a person are affected by it,” Watterson mentioned, in response to the report, including that he did not supply any particulars on the pending strikes.

Southwest didn’t instantly reply to a Reuters request for remark.

The airline has been struggling to seek out its footing after the COVID-19 pandemic, partly as a result of Boeing’s plane supply delays and industry-wide overcapacity within the home market.

It plans to supply assigned and extra-legroom seats to draw premium vacationers and begin in a single day flights. It would current the small print to traders on Sept. 26.

Earlier this week, Reuters reported that Elliott, which owns 10% of Southwest’s frequent shares, informed one of many firm’s high unions it nonetheless needs to switch CEO Robert Jordan, even after the service pledged to shake up its board.

(Reporting by Surbhi Misra in Bengaluru; Modifying by Paul Simao)

1 No-Brainer Electrical Automobile (EV) Inventory to Purchase With $200 Proper Now

High Bitcoin Miners Revolutionize North America’s Crypto Panorama in 2024

Southwest Airways warns employees of 'robust selections' forward, Lusso’s Information experiences

One Wall Road Analyst Simply Added Palantir to Its High Funding Record and Says It May Climb 35%. Time to Purchase?

1 Magnificent Excessive-Yield Dividend Progress Inventory Down 40% to Purchase and Maintain Eternally

Southwest Airways warns employees of 'powerful selections' forward, Bloomberg reviews

3 Dividend Kings to Add to Your Portfolio for a Lifetime of Passive Revenue

This Monster Progress Inventory Is Up Practically 300% in 5 Years. Right here's Why It's the Largest Inventory Place in My Portfolio Proper Now.

JPMorgan CEO Jamie Dimon Calls For Federal Workers To Return To Workplace, Says Empty Buildings 'Trouble' Him: 'I Can't Imagine…'

US to suggest barring Chinese language software program, {hardware} in related automobiles, sources say

Valuation Angst Is Being Stoked by Fed’s Huge Lower: Credit score Weekly

Trump Household's Crypto Enterprise Revealed: New Shopping for Guidelines, Who Can Make investments and What It Means for Early Adopters

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoInventory market in the present day: US futures slip as Micron slides, with information on deck

-

Markets3 months ago

Markets3 months agoFutures dip as Micron drags down chip shares forward of financial information

-

Markets3 months ago

Markets3 months agoApogee shares rise almost 4% on upbeat steering and earnings beat

-

Markets3 months ago

Markets3 months agoWhy Is Micron Inventory Down After a Double Earnings Beat?

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoHungary central financial institution tells lenders to reimburse purchasers after Apple glitch

-

Markets3 months ago

Markets3 months agoSoftBank to spend money on search startup Perplexity AI at $3 billion valuation, Bloomberg experiences

-

Markets3 months ago

Markets3 months agoInventory market at present: Asian shares decrease after Wall Avenue closes one other profitable week

-

Markets3 months ago

Markets3 months ago3 No-Brainer Synthetic Intelligence (AI) Shares to Purchase With $500 Proper Now

-

Markets3 months ago

Markets3 months agoNeglect Nvidia: Distinguished Billionaires Are Promoting It in Favor of These 7 High-Notch Shares

-

Markets3 months ago

Markets3 months agoMeet the 1 S&P 500 Inventory That's Outperforming Nvidia So Far in 2024