Markets

Higher Synthetic Intelligence (AI) Inventory: Nvidia vs. Tremendous Micro Pc

Amid the continuing synthetic intelligence (AI) increase, shares of Nvidia (NASDAQ: NVDA) and Tremendous Micro Pc (NASDAQ: SMCI) have set the inventory market on hearth in 2024, racking up good points of 166% and 197%, respectively, as of this writing. Because of the booming demand for the AI-enabling {hardware} they promote, they’ve skilled gorgeous accelerations of their income and earnings progress.

Nvidia’s dominance within the AI chip market has translated into phenomenal progress, and Tremendous Micro Pc is not far behind. Knowledge heart operators are flocking to its modular server options to mount the AI chips that Nvidia and different firms promote. Nevertheless, if you’re wanting so as to add an to your portfolio and wish to select between considered one of these two, which one do you have to be shopping for proper now?

The case for Nvidia

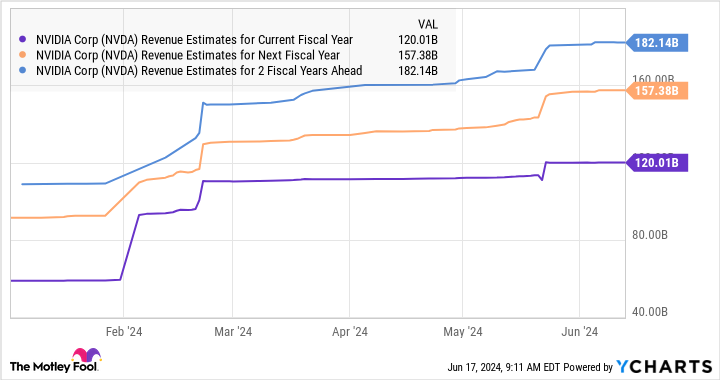

Nvidia reportedly managed a whopping 94% of the AI chip market on the finish of 2023. The corporate’s outcomes for the primary quarter of its fiscal 2025 (which ended on April 28) recommend that its dominance has it on track for one more 12 months of terrific progress.

Income rose a shocking 262% 12 months over 12 months to $26 billion. Its spectacular pricing energy led to a 461% surge in adjusted earnings to $6.12 per share. Administration’s income steering of $28 billion for the present quarter means that its high line is on monitor to leap 107% 12 months over 12 months, which might be an acceleration from the 101% progress it delivered in the identical interval final 12 months.

Nevertheless, rising progress avenues within the nascent AI market point out that Nvidia may find yourself doing even higher than that. As an illustration, governments throughout the globe are reportedly pouring big quantities of cash into AI infrastructure, and sovereign investments in AI expertise are anticipated to contribute $10 billion to Nvidia’s high line this fiscal 12 months, as in comparison with nothing within the earlier one.

Extra particularly, governments want to make giant language fashions (LLMs) in native languages primarily based on country-specific knowledge. On Nvidia’s Might convention name, administration identified that Japan, France, Italy, and Singapore are already investing in AI infrastructure. It expects extra nations to affix the bandwagon. “The significance of AI has caught the eye of each nation,” mentioned CFO Colette Kress.

Saudi Arabia, for example, is reportedly trying to make investments $40 billion in AI initiatives, whereas China’s AI-focused spending is forecast to exceed $38 billion by 2027. In the meantime, key Indian firms akin to Tata Group and Reliance Industries are counting on Nvidia’s chips to coach LLMs.

In brief, Nvidia’s buyer base is diversifying past which have been deploying its chips in giant numbers to coach and deploy AI fashions. Spending on AI chips is predicted to develop greater than 10-fold over the following decade, producing $341 billion in income in 2033 in comparison with $23 billion final 12 months. The stage appears set for Nvidia to keep up its large progress because it takes strong steps to make sure that it stays the dominant participant on this area.

That is why analysts forecast that the corporate’s high line will continue to grow at a wholesome tempo from fiscal 2024’s studying of practically $61 billion.

So, Nvidia ought to stay a high AI inventory because the race to develop AI purposes by firms and governments alike has created a secular progress alternative.

The case for Tremendous Micro Pc

Supermicro’s progress is entwined to some extent with that of Nvidia. Knowledge heart operators require server rack options of the kind that Supermicro sells to mount the processors bought by Nvidia and different chipmakers. So, it’s not stunning that demand for Supermicro’s servers has merely taken off.

In its fiscal 2024 third quarter, which ended March 31, its income jumped 200% 12 months over 12 months. Non-GAAP web earnings per share, in the meantime, jumped by a whopping 307%. So, Supermicro is not all that far behind Nvidia in the case of how AI has supercharged its fortunes. The corporate is guiding for income of $14.9 billion within the present fiscal 12 months, which ends this month. This might be a giant bounce over the $7.1 billion in income it reported in its fiscal 2023.

Extra importantly, analysts expect its high line to just about double over the following couple of fiscal years.

The great half is that Supermicro can maintain a wholesome tempo of progress past the following couple of fiscal years. That is as a result of the demand for AI servers is predicted to increase at a compound annual fee of 25% by way of 2029. The market is predicted to generate annual income of virtually $73 billion after 5 years, up from $17.5 billion in 2022.

Supermicro is rising at a quicker tempo than the AI server market proper now. Because it seems, its progress is quicker than that of extra established firms akin to Dell Applied sciences, which has bought $3 billion value of AI servers previously three quarters. Supermicro generated $9.6 billion in income previously three quarters and will get greater than half its income from promoting AI-related server options.

Supermicro has been in a position to make a dent within the AI server market regardless of the presence of larger gamers. Additionally, with the strikes that the corporate has been making to extend its production-utilization fee and its manufacturing capability, it may nook an even bigger share of the AI server market sooner or later.

Like Nvidia, even Supermicro seems to be like a strong long-term AI play. However is it value shopping for over Nvidia?

The decision

Each Nvidia and Supermicro are high-growth firms benefiting massive time from the proliferation of AI. So buyers’ selection about which inventory they might wish to purchase proper now’s going to boil right down to the valuation. Supermicro is considerably cheaper than Nvidia so far as their earnings and gross sales multiples are involved.

Nevertheless, by way of the value/earnings-to-growth (PEG) ratio, the story is a little more attention-grabbing. That metric is a forward-looking valuation decided by dividing an organization’s trailing earnings a number of by the earnings progress that it’s anticipated to ship over a future interval. Any (constructive) PEG ratio beneath 1 is seen by most buyers as indicating a discount inventory. And on that metric, each Nvidia and Supermicro are undervalued.

So by not less than one forward-looking measure, each Nvidia and Supermicro are engaging buys proper now for anybody wanting so as to add a progress inventory to their portfolios. Extra importantly, each these firms appear able to delivering the excellent progress that the market expects from them, due to the profitable alternatives they’re sitting on. And that is why buyers can think about shopping for both inventory, regardless of the terrific good points they’ve clocked to date this 12 months.

Do you have to make investments $1,000 in Nvidia proper now?

Before you purchase inventory in Nvidia, think about this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the for buyers to purchase now… and Nvidia wasn’t considered one of them. The ten shares that made the lower may produce monster returns within the coming years.

Contemplate when Nvidia made this record on April 15, 2005… for those who invested $1,000 on the time of our suggestion, you’d have $830,777!*

Inventory Advisor gives buyers with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of June 10, 2024

has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Nvidia. The Motley Idiot has a .

was initially revealed by The Motley Idiot

Markets

'You By no means Ask Me for Cash Once more': Kevin O'Leary Explains As a substitute Of Investing In Household Members' Companies, He Items Money With A Caveat

, a big-name investor identified for his no-nonsense method to enterprise, has a singular technique for coping with relations who ask him for cash. He is had his justifiable share of family coming to him with huge concepts and excessive hopes, on the lookout for a hefty funding. And with O’Leary’s monetary standing, it isn’t shocking. The Canadian enterprise proprietor and Shark Tank star has a internet price of round $400 million.

Do not Miss:

However whereas he is beneficiant, he is additionally obtained boundaries that assist maintain household and funds from clashing. In a brief YouTube video, O’Leary defined his actions when relations ask him for cash. He acknowledges the age-old reality: “More cash, extra issues.” O’Leary says, “It is a improbable factor but it surely makes your life difficult as a result of many individuals need a few of it from you at no cost – notably relations. It is a large concern.”

Trending: Amid the continued EV revolution, beforehand missed low-income communities

O’Leary clarifies that individuals come to anticipate one thing for nothing . And to deal with this, he is developed an easy technique that retains issues clear and avoids awkward Thanksgiving dinners.

When a member of the family approaches him for cash – whether or not it is to begin a restaurant or launch a brand new enterprise – he presents a one-time reward. Within the case he mentions, it is $50,000. Not a mortgage, not an funding, only a reward. However there is a catch: “You by no means ask me for cash once more. Ever.” O’Leary’s rule is easy: after that test, there will likely be no extra handouts, no future expectations, and no monetary entanglements. As he humorously provides, he arms over the cash after which “goes again to sprucing his eggs.” It is a clear break that leaves no room for future monetary disputes or awkward household interactions.

Trending: Groundbreaking buying and selling app with a ‘Purchase-Now-Pay-Later’ characteristic for shares tackles the $644 billion margin lending market –

For many who do not have a portfolio like O’Leary’s, his method nonetheless presents a beneficial lesson. Setting clear boundaries is essential when lending or gifting cash to household. Getting caught up within the feelings and obligations that include serving to family members is straightforward, however issues can get messy with out clear guidelines. An excellent method for the remainder of us is likely to be to solely give what we will afford to lose – whether or not that is $50, $500, or $5,000 – and make it clear that it is a one-time deal. No loans, no strings, no awkward household gatherings.

Dealing with household and cash might be tough, however O’Leary’s method reveals that it is all about setting expectations and sticking to them. And perhaps, simply perhaps, it is also about having just a little humor to maintain issues from getting too tense.

It is at all times good to earlier than making huge selections, particularly when household is concerned. They might help you identify what makes essentially the most sense in your scenario and set the best boundaries. It isn’t simply in regards to the cash – it is about retaining relationships intact whereas making decisions that work for everybody. Just a little steerage can go a great distance in guaranteeing your funds and household ties keep sturdy.

Learn Subsequent:

UNLOCKED: 5 NEW TRADES EVERY WEEK. , plus limitless entry to cutting-edge instruments and methods to achieve an edge within the markets.

Get the most recent inventory evaluation from Benzinga?

This text initially appeared on

© 2024 Benzinga.com. Benzinga doesn’t present funding recommendation. All rights reserved.

Markets

A Few Years From Now, You'll Want You'd Purchased This Undervalued Excessive-Yield Inventory

One of many largest temptations for dividend traders is reaching for yield. Principally, which means taking over dangerous investments simply to gather a bigger revenue stream. You will be higher off in the long term if you happen to err on the aspect of warning, significantly if you’ll want to reside off of the revenue you’re producing. That is why Enterprise Merchandise Companions (NYSE: EPD) is a high-yield funding you may want you’d purchased. A fast comparability to Altria (NYSE: MO) will assist clarify why.

Who wins the high-yield story, Altria or Enterprise?

Relating to yield, Altria’s 8.1% is a full proportion level increased than the distribution yield of Enterprise Merchandise Companions’ 7.1%. Each have elevated their dividends usually, so many traders would possibly default to the higher-yielding choice. However that is not essentially the most effective plan.

Altria, , comes with extra threat than it’s possible you’ll assume regardless of working in what is mostly thought of a dependable sector. That is as a result of its fundamental product is cigarettes. This enterprise has been in a secular decline for a very long time. Within the second quarter of 2024 alone, Altria’s cigarette volumes fell 13% 12 months over 12 months. That is not a fluke. Within the second quarter of 2023, volumes fell 8.7%. In the identical quarter of 2022, cigarette quantity was off by 11.1%. Any latest quarter and any latest full 12 months would have proven the identical horrible development.

The corporate has offset quantity declines with worth will increase, which has allowed it to proceed rising its dividend regardless of the clearly horrible course of its most essential enterprise line. There is a very actual probability that you’ll remorse shopping for this high-yield dividend inventory if it may possibly’t stem the bleeding not directly.

Enterprise is a completely completely different story.

Enterprise’s decrease yield comes with decrease threat

You possibly can simply argue that Enterprise comes with its personal dangers, on condition that it operates within the extremely risky vitality sector. And its midstream enterprise is immediately tied to demand for oil and pure gasoline, which is being pressured by the transfer towards cleaner options. Truthful sufficient, however what does Enterprise truly do?

As a midstream supplier, Enterprise owns important infrastructure belongings that assist transfer oil and pure gasoline around the globe. It typically fees charges for using its infrastructure, so the worth of vitality is much less essential than the demand for vitality. Demand for vitality tends to stay sturdy whatever the worth of oil and pure gasoline.

However here is the large truth — regardless of all of the hype round clear vitality, demand for oil and pure gasoline is predicted to stay sturdy for many years to come back. Actually, demand will doubtless improve for these fuels, with far dirtier coal bearing the brunt of the clear vitality change.

In different phrases, Enterprise’s enterprise is not as dangerous as it could appear. On prime of that, it is without doubt one of the largest midstream gamers in North America with an investment-grade-rated steadiness sheet. Whereas inner development choices are restricted, it has lengthy acted as an trade consolidator. It simply introduced plans to purchase Pinon Midstream for $950 million, for instance. Acquisitions are lumpy and unimaginable to foretell, however they provide Enterprise ample room for development on prime of the sluggish and regular worth will increase it is going to be in a position to extract from clients.

In order for you a excessive yield from a rising enterprise, Enterprise is the higher choice when in comparison with Altria and its declining core enterprise. Certain, you may hand over a proportion level of yield, however as Altria continues to wrestle, that final level will can help you sleep at evening if you happen to purchase Enterprise.

Enterprise’s yield nonetheless appears low-cost

Here is essentially the most fascinating half: Enterprise’s 7.1% dividend yield is above its 10-year common yield of 6.3%. So regardless of the restoration from pandemic lows, it nonetheless seems to be undervalued. A rising enterprise, a financially robust firm, and an undervalued worth all make Enterprise a high-yield inventory you may remorse lacking out on. Particularly whenever you evaluate it to different high-yield decisions with equally excessive, however far riskier, yields.

Must you make investments $1,000 in Altria Group proper now?

Before you purchase inventory in Altria Group, take into account this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the for traders to purchase now… and Altria Group wasn’t one among them. The ten shares that made the lower might produce monster returns within the coming years.

Take into account when Nvidia made this listing on April 15, 2005… if you happen to invested $1,000 on the time of our suggestion, you’d have $743,952!*

Inventory Advisor gives traders with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has no place in any of the shares talked about. The Motley Idiot recommends Enterprise Merchandise Companions. The Motley Idiot has a .

was initially printed by The Motley Idiot

Markets

If You Purchased 1 Share of Nvidia at Its IPO, Right here's How Many Shares You Would Personal Now

Since its IPO in January 1999, Nvidia (NASDAQ: NVDA) has established itself as one of many world’s most profitable firms. It has been notably adept at adapting its expertise to increase into new markets.

The corporate pioneered the that revolutionized the gaming business, turning boxy figures into lifelike pictures. The key to its success was parallel processing, which allowed the chips to conduct a large number of mathematical calculations concurrently. Nvidia’s processors are actually used for product design, autonomous methods, cloud computing, information facilities, synthetic intelligence (AI), and extra.

The flexibility to adapt its expertise has been a boon to shareholders. Even when buyers did not get in on the IPO itself, Nvidia shares fell beneath their challenge worth quite a few occasions in early 1999. For buyers lucky sufficient to get shares at (or beneath) the $12 IPO worth, the inventory has returned 493,940%.

Multiplying like rabbits

Whereas a single share of inventory may appear inconsequential at first look, one share of the proper inventory can have a huge effect on an investor’s success. In Nvidia’s case, the corporate’s efficiency and hovering inventory worth have resulted in quite a few inventory splits, turning one share into many extra.

Here is a listing of Nvidia’s inventory splits over time:

-

2-for-1 cut up, June 27, 2000

-

2-for-1 cut up, Sept. 12, 2001

-

2-for-1 cut up, April 7, 2006

-

3-for-2 cut up, Sept. 11, 2007

-

4-for-1 cut up, July 20, 2021

-

10-for-1 cut up, June 10, 2024

Because of the a number of inventory splits, an investor who purchased only one share of Nvidia inventory close to its IPO in 1999 would now be the proud proprietor of 480 shares.

Nevertheless, it took an excessive amount of self-discipline and self-control to carry Nvidia for greater than 25 years and reap this windfall. The inventory has misplaced greater than half its worth on quite a few events, which despatched fair-weather buyers scrambling for the exits.

That stated, take into account this: A $1,000 funding in Nvidia made in early 1999 would now be value greater than $4.9 million.

Must you make investments $1,000 in Nvidia proper now?

Before you purchase inventory in Nvidia, take into account this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the for buyers to purchase now… and Nvidia wasn’t considered one of them. The ten shares that made the reduce might produce monster returns within the coming years.

Contemplate when Nvidia made this listing on April 15, 2005… in case you invested $1,000 on the time of our advice, you’d have $743,952!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has positions in Nvidia. The Motley Idiot has positions in and recommends Nvidia. The Motley Idiot has a .

was initially revealed by The Motley Idiot

'You By no means Ask Me for Cash Once more': Kevin O'Leary Explains As a substitute Of Investing In Household Members' Companies, He Items Money With A Caveat

A Few Years From Now, You'll Want You'd Purchased This Undervalued Excessive-Yield Inventory

If You Purchased 1 Share of Nvidia at Its IPO, Right here's How Many Shares You Would Personal Now

Assume You Know Altria? Right here's 1 Little-Identified Reality You Can't Overlook.

The Final Electrical Car (EV) Inventory to Purchase With $1,000 Proper Now

UBS chair warns towards massive improve in capital necessities, newspaper studies

Meet the three Supercharged Development Shares That Will Be Price $4 Trillion by 2025, In accordance with 1 Wall Avenue Analyst

Tremendous Micro: Assessing the Potential Danger and Reward

Unique-TPG in lead to purchase stake in Inventive Planning at $15 billion valuation, sources say

Exxon director joins Elliott group searching for to accumulate Citgo Petroleum

Steward Well being CEO who refused to testify to US Senate will step down

Nvidia Inventory (NVDA) Is Nonetheless a Lengthy-Time period Winner, No Matter the Noise

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoADP Stories Decrease-Than-Anticipated Personal Payroll Progress for June

-

Markets3 months ago

Markets3 months agoSorry, however retiring ‘comfortably’ on $100K is a fantasy for most individuals. Right here’s why.

-

Markets3 months ago

Markets3 months agoSouthwest Air adopts 'poison tablet' as activist investor Elliott takes important stake in firm

-

Markets3 months ago

Markets3 months agoAbove Food Corp. (NASDAQ: ABVE) and Chewy Inc. (NYSE: CHWY) Making Headlines This Week

-

Markets3 months ago

Markets3 months agoCore Scientific so as to add 15 EH/s by means of Block’s 3nm Bitcoin mining ASICs

-

Markets3 months ago

Markets3 months agoWarren Buffett is popping 94 subsequent month. Ought to Berkshire traders begin to fear?

-

Markets3 months ago

Markets3 months agoWhy Rivian Inventory Roared Forward 10% on Friday

-

Markets3 months ago

Markets3 months agoArgentina to Promote {Dollars} In Parallel FX Market, Caputo Says

-

Markets3 months ago

Markets3 months agoWhy Intel Inventory Popped on Friday

-

Markets3 months ago

Markets3 months agoMicrosoft in $22 million deal to settle cloud grievance, keep off regulators

-

Markets3 months ago

Markets3 months agoMorgan Stanley raises worth targets on score companies on constructive outlook