Markets

Insiders Snap Up These 2 ‘Robust Purchase’ Shares

Let’s speak about insider buying and selling. Not the unlawful type, however the completely regular – and totally authorized – buying and selling by top-level company officers. These are the C-suite residents and the members of the Boards, firm officers who know what’s happening behind the scenes and are accountable to shareholders for bringing in earnings. They usually maintain shares in their very own corporations and make trades primarily based on the information they’ve from behind the scenes.

To maintain the enjoying subject stage, federal regulators require that firm insiders publish these transactions – and traders can profit from seeing simply which shares the company officers are shopping for. There’s one factor to recollect: firm brass will promote their shares for a mess of causes, however they’ll solely purchase huge once they imagine the inventory is on the best way up.

So, let’s check out some current insider trades. Utilizing the device from TipRanks, we’ve pulled up the current information on two shares which have lately seen multi-million greenback buys from Board members. In every case, that is the primary such buy from the insider. With the numerous outlay of the purchase, that factors to elevated confidence within the firm’s prospects for the near- to mid-term.

Along with the current high-value insider purchases, the TipRanks information exhibits us that each shares function Robust Purchase rankings from the Avenue and strong upside potential for the approaching 12 months. Right here’s a better have a look at them.

Terns Prescription drugs (TERN)

First up is Terns Prescription drugs, a biopharmaceutical analysis agency working at each the early growth and the medical trials phases. The corporate has set its sights on the fields of oncology and metabolic illness, and has a medical program underway in every of those areas, concentrating on power myeloid leukemia (CML) within the first and weight problems, a significant well being situation, within the second. The corporate’s pipeline consists of novel small molecule compounds, with clinically validated modes of motion.

That’s a mouthful, however it comes right down to a pipeline that options two Section 1 medical trials. The primary of those options TERN-701, an allosteric BCR-ABL tyrosine kinase inhibitor, or TKI, designed to deal with CML. This most cancers begins within the bone marrow, the place blood cells are fashioned, and is taken into account a power, life-long and life-threatening illness that ceaselessly requires adjustments in therapies. Terns’ drug candidate, TERN-701, is present process the Section 1 CARDINAL trial, a two-part examine to judge the protection, pharmacokinetics, and efficacy of the drug. Interim information from the primary cohorts of the dose escalation a part of the examine is predicted for launch this coming December.

Additionally of observe on the medical trial facet is TERN-601, which has simply accomplished a Section 1 trial. This drug is an orally dosed, glucagon-like peptide-1 (GLP-1) receptor agonist, underneath investigation as an weight problems remedy. The corporate launched optimistic trial outcomes from that examine earlier this month, exhibiting that TERN-601 produced a statistically vital weight reduction in trial individuals over a 28-day interval. The drug was thought-about well-tolerated, and the corporate plans to provoke a Section 2 trial subsequent 12 months.

Additionally on the weight problems monitor, Terns has lately reported optimistic pre-clinical information from one other drug candidate, TERN-501. This pre-clinical information helps utilizing TERN-501 together with a GLP-1 receptor agonist as a remedy for weight problems. The information confirmed that TERN-501, within the combo remedy, resulted in larger weight reduction and a greater retention of lean mass.

These medical applications don’t come low-cost, and Terns lately performed a public inventory providing to boost capital. The corporate providing, which noticed greater than 14 million shares made accessible, closed on September 12. Terns raised roughly $172.7 million in gross proceeds from the sale.

With that in thoughts, we are able to flip to the insider trades – and we see that Board of Administrators member Lu Hongbo bought 476,190 shares on the day the general public providing closed. Hongbo paid nealy $5 million for this inventory buy.

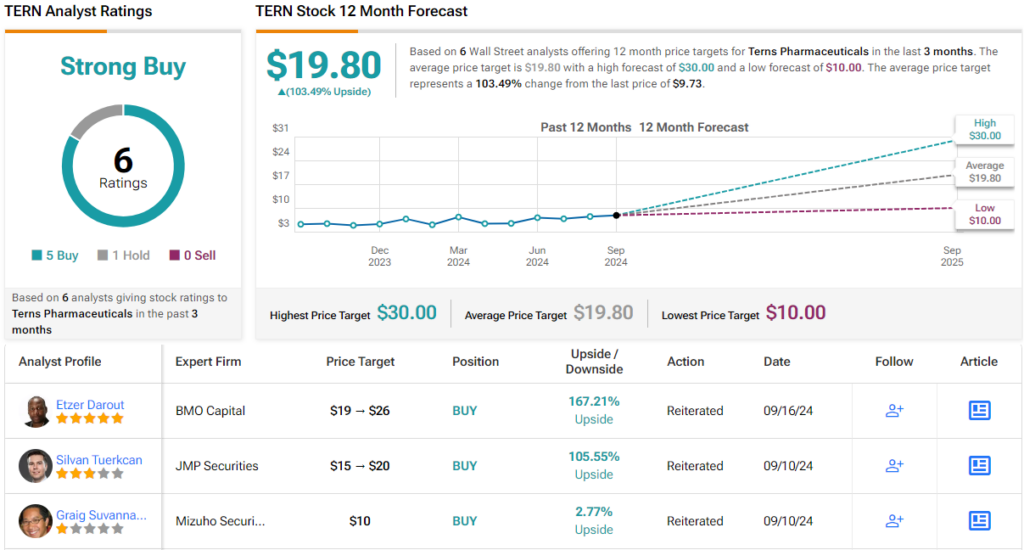

This inventory has additionally caught the eye of BMO analyst Etzer Darout, who likes the a number of catalysts lined up for it.

“With the weight problems information from TERN-601 (oral GLP-1 agonist), TERN has delivered on a once-daily and clinically aggressive drug profile for 2 of its three medical applications (TERN-501, TERN-601) which provides us extra confidence forward of Section 1 CML dose escalation information with TERN-701 (BCR-ABL allosteric) in December. With two partially de-risked medical applications and one other de-risking occasion upcoming, we proceed to love the risk-reward for TERN and its setup for worth creation in oncology and metabolic ailments,” Darout opined.

These feedback again up Darout’s Outperform (i.e. Purchase) ranking on TERN shares, and his $26 value goal factors towards a possible one-year achieve of 159%. (To look at Darout’s monitor document, )

General, this inventory’s Robust Purchase consensus ranking relies on 6 current analyst evaluations that break up 5 to 1 in favor of Purchase over Maintain. The shares are presently buying and selling at $9.73, and the typical goal value, $19.80, implies a 103% upside within the subsequent 12 months. (See )

Permian Assets (PR)

For the second inventory on our listing, we’ll shift gears and have a look at the vitality sector. Permian Assets is an unbiased oil and gasoline exploration and manufacturing agency working within the wealthy oil fields of Texas. The corporate’s identify provides away its recreation – Permian’s property are situated within the richest components of the Permian Basin of Texas-New Mexico. The corporate’s land holdings complete greater than 400,000 internet leasehold acres, which incorporates greater than 68,000 internet royalty acres. These holdings are centered within the Midland and Delaware Basins of the bigger Permian formation, and a few 45% of the manufacturing on these landholdings is crude oil.

This makes Permian one of many area’s largest pure-play hydrocarbon E&P corporations, and on September 17 the corporate introduced the closing of a bolt-on acquisition to its Delaware Basin property. The acquisition, a cope with Occidental, added ~29,500 internet acres and ~9,900 internet royalty acres, together with a major quantity of midstream infrastructure, to Permian’s present Reeves County, Texas positions.

In one other replace that ought to curiosity traders, Permian introduced on September 3 a big enhance to its common base dividend. The dividend cost, previously at 6 cents per widespread share, has been elevated by 150% and is now set at 15 cents per share to be paid out beginning in 3Q24. The brand new annualized price of 60 cents per share will give a ahead yield of 4.3% primarily based on the present share worth.

Permian attracted a current giant purchase from an insider, firm director William Quinn. Quinn made two purchases, on September 10 and 11, that totaled 312,429 shares – and value greater than $3.99 million.

Turning to the analysts’ view of the inventory, we’ll test in with Truist’s vitality sector professional Neal Dingmann, who sees Permian as top-of-the-line shares that he covers, with loads of capital return and efficient merger actions. In a observe earlier this month, Dingmann wrote, “We imagine PR operations proceed to be among the many greatest in our protection with bettering effectively outcomes and decreasing of unit prices whereas now including an equally steady monetary plan that can embody notable share buybacks. Additional, the excessive share overhang has been eradicated with present personal fairness doubtless promoting fewer shares going ahead. The corporate additionally continues to have one of many simpler M&A methods that won’t change going ahead with a concentrate on accretive additions in core areas. As such, we imagine there stays notable share value upside potential with the present valuation not reflective of continued operational and monetary success.”

For Dingmann, PR shares get a Purchase ranking with a $22 value goal that suggests an upside of 55% on the one-year horizon. (To look at Dingmann’s monitor document, )

All in all, PR’s Robust Purchase consensus ranking relies on 16 evaluations that embody 14 Buys in opposition to simply 2 Holds. With a buying and selling value of $14.18 and a mean goal value of $19.43, Permian’s inventory has a 37% upside this coming 12 months. (See )

To seek out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ , a device that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely essential to do your individual evaluation earlier than making any funding.

Investing in dividend shares might be a good way to construct your passive revenue. Many firms pay a portion of their income to buyers through dividends.

Whereas the common round 1.5% today (primarily based on the S&P 500’s yield), many provide even greater funds. Kinder Morgan (NYSE: KMI), Verizon (NYSE: VZ), Brookfield Infrastructure Companions (NYSE: BIP), and Agree Realty (NYSE: ADC) stand out for his or her payouts. All 4 firms provide dividends yielding 4% or extra. Additional, they’ve wonderful information of accelerating their funds.

Piping passive revenue into your portfolio

Kinder Morgan at present yields greater than 5%. The pipeline big backs that high-yielding dividend with very secure money stream. Roughly 68% comes from take-or-pay agreements and hedging contracts that pay the corporate a hard and fast price no matter volumes and commodity costs. In the meantime, most of its remaining earnings come from belongings that generate fee-based money stream with restricted fluctuations primarily based on their quantity publicity.

The corporate pays out about half of its secure money stream in dividends. It retains the remaining to fund its growth whereas sustaining its sturdy stability sheet.

Kinder Morgan at present has $5.2 billion in high-return growth tasks underway that can develop its money stream over the subsequent few years. It additionally makes use of its monetary flexibility to make accretive acquisitions (it purchased STX Midstream for about $1.8 billion late final 12 months). These progress catalysts ought to give it extra gasoline to extend its dividend. Kinder Morgan delivered its seventh consecutive 12 months of dividend progress in 2024.

Your connection to a prodigious passive revenue stream

Verizon gives a dividend yield of greater than 6% today. The telecom big lately delivered its 18th straight 12 months of dividend progress. That is the longest present streak within the U.S. telecom sector.

The cell and broadband firm generates lots of money. Its working money stream totaled $16.6 billion throughout the first half of this 12 months, sufficient to cowl its capital bills ($8.1 billion) and dividend funds ($5.6 billion) with room to spare. It used that extra money to strengthen its stability sheet.

Verizon’s steadily bettering stability sheet is enabling it to . That acquisition ought to ultimately assist develop its free money stream, which ought to enable it to repay that debt. In the meantime, its capital investments to develop its fiber and 5G companies must also assist enhance its money stream. These drivers ought to allow Verizon to proceed extending its dividend progress streak within the coming years.

Extra revenue from this feature

Brookfield Infrastructure Companions at present gives a dividend yield approaching 5%. That is a lot greater than its company twin, Brookfield Infrastructure Corp. (NYSE: BIPC), which gives a payout approaching 4%. The one distinction is that the publicly traded restricted partnership sends its buyers a Schedule Ok-1 federal tax type annually, whereas the company gives an easier-to-file 1099-Div Kind.

The economically equal entities pay the identical quarterly dividend fee, which they plan to develop by 5% to 9% yearly. That might prolong Brookfield Infrastructure’s already wonderful streak of accelerating its fee (15 straight years). The worldwide infrastructure operator generates secure and rising money stream to cowl its profitable payout. The corporate sees a mixture of inflation escalators, quantity progress, capital tasks, and acquisitions powering greater than 10% annual FFO–per-share progress within the coming years.

Numerous progress left

Agree Realty at present yields 4%. The retail REIT has grown its dividend, which it pays month-to-month, at a 5.7% compound annual price during the last 10 years.

The actual property funding belief focuses on proudly owning freestanding properties web leased or floor leased to high-quality retail tenants. Almost 70% of its hire comes from nationwide or regional tenants with investment-grade credit score rankings. In the meantime, prime tenant sectors are retailers resilient to the pressures of e-commerce and recessions, like grocery shops, house enchancment facilities, and tire and auto service areas.

Agree Realty steadily grows its portfolio of income-producing properties by making acquisitions or investing in growth tasks. It has a powerful stability sheet and a really lengthy progress runway. Its present tenants nonetheless personal over 166,000 of their areas, a large whole addressable market alternative for the roughly 2,200-property REIT.

Steadily rising passive revenue

Kinder Morgan, Verizon, Brookfield Infrastructure Companions, and Agree Realty provide dividend yields above 4%, backed by secure money flows and sturdy monetary profiles. Additional, this quartet has finished a wonderful job rising their payouts over time, which appears prone to proceed. These options make them wonderful dividend shares to purchase for these searching for enticing, steadily rising streams of passive revenue.

Must you make investments $1,000 in Kinder Morgan proper now?

Before you purchase inventory in Kinder Morgan, contemplate this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they imagine are the for buyers to purchase now… and Kinder Morgan wasn’t one in all them. The ten shares that made the minimize might produce monster returns within the coming years.

Take into account when Nvidia made this record on April 15, 2005… in the event you invested $1,000 on the time of our suggestion, you’d have $710,860!*

Inventory Advisor gives buyers with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has positions in Brookfield Infrastructure Company, Brookfield Infrastructure Companions, Kinder Morgan, and Verizon Communications. The Motley Idiot has positions in and recommends Kinder Morgan. The Motley Idiot recommends Brookfield Infrastructure Companions and Verizon Communications. The Motley Idiot has a .

was initially revealed by The Motley Idiot

Lusso’s Information — Shares of Dunelm Group (LON:) fell after WA Capital Restricted, an organization managed by Sir Will Adderley, the Deputy Chair of Dunelm, and Woman Nadine Adderley, had bought a serious portion of their shares within the firm.

At 5:02 am (0902 GMT), Dunelm Group was buying and selling 6.3% decrease at £1,157.50.

This sale, carried out via an accelerated bookbuild secondary inserting, concerned about 10 million abnormal shares of Dunelm’s issued share capital.

The final time Sir Will Adderley decreased his holdings in Dunelm was in February 2021.

Because of this sale, the Adderley household’s mixed possession in Dunelm will lower to 37.6%, from their earlier holding.

“Sir Will Adderley has undertaken that, following completion of the Inserting, he won’t get rid of additional shares within the Firm for a interval of a minimum of 180 days, topic to customary exceptions,” WA Capital stated in a press release.

Barclays acted because the Sole International Co-ordinator and Joint Bookrunner for this transaction, alongside UBS AG London Department.

The inserting’s specifics, together with the ultimate pricing, are set to be decided upon the closure of the accelerated bookbuilding course of.

Lusso’s Information — Buyers have been including to their lengthy positions within the following final week’s first Federal Reserve fee reduce in years, Citi famous in a brand new weekly report.

Remaining quick positions within the small-cap index are going through a mean lack of 5.7%, and “a brief squeeze may help additional upside close to time period,” Citi strategists stated.

The reveals comparable overextension, whereas traders seem largely ambivalent towards the , the place web positioning stays near impartial.

“Final week was additionally risky due to Triple Witching creating vital roll exercise alongside the FOMC fee resolution,” Citi strategists stated.

Market volatility surged following the 50 foundation level fee reduce from the FOMC, however US futures markets quickly started to rally in a single day. This restoration was supported by exchange-traded fund (ETF) inflows and new lengthy positions in US markets. Nonetheless, a noticeable break up in investor threat urge for food for US equities has persevered, as mirrored in final week’s flows.

Exterior of the US, Europe’s positioning has stayed impartial with combined flows over current weeks. Whereas ETF inflows have been regular, they continue to be modest, and there hasn’t been a transparent constructive or damaging pattern in Eurostoxx flows throughout this era.

In Asia, relative positioning shifts in Europe, Australasia and the Far East (EAFE), and rising market (EM) futures had been unusually giant, even contemplating it was a roll week. This led to EM futures shifting from impartial to the third most prolonged lengthy place, whereas EAFE futures shifted from mildly bullish to the second most prolonged quick, in response to Citi.

For futures, web positioning stays closely bearish (-2.2 normalized), however a bullish pattern emerged final week as traders began including new lengthy positions to stability worthwhile shorts.

In distinction, most quick positions within the had already been unwound, leaving the market largely lengthy, with common lengthy positions seeing a 4.2% revenue.

4 Dividend Shares Yielding 4% or Extra to Purchase for Passive Revenue Proper Now

Dunelm Group falls as largest shareholder cuts stake

Insiders Snap Up These 2 ‘Robust Purchase’ Shares

Investor urge for food for small caps rising after Fed fee reduce, Citi says

China Unleashes Stimulus Bundle to Revive Financial system, Markets

European shares rise after Chinese language stimulus; progress considerations stay

Listed below are an important days for the inventory market between now and the November election, in accordance with BofA

JPMorgan bullish on India and Japan, prime Asia official says

DJT inventory falls one other 10%. May Trump Media’s plunge lastly spell the tip for SPACs?

Shares of Miniso stoop on plans to purchase stake in Yonghui Superstores

One inventory being focused by a value-investing legend in a market he says has gotten too top-heavy

Asian shares rise on China stimulus cheer; Australia lags earlier than RBA

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoInventory market in the present day: US futures slip as Micron slides, with information on deck

-

Markets3 months ago

Markets3 months agoFutures dip as Micron drags down chip shares forward of financial information

-

Markets3 months ago

Markets3 months agoApogee shares rise almost 4% on upbeat steering and earnings beat

-

Markets3 months ago

Markets3 months agoWhy Is Micron Inventory Down After a Double Earnings Beat?

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoSoftBank to spend money on search startup Perplexity AI at $3 billion valuation, Bloomberg experiences

-

Markets3 months ago

Markets3 months agoHungary central financial institution tells lenders to reimburse purchasers after Apple glitch

-

Markets3 months ago

Markets3 months agoMeet the 1 S&P 500 Inventory That's Outperforming Nvidia So Far in 2024

-

Markets3 months ago

Markets3 months agoDown 30% From Its All-Time Excessive, Ought to You Purchase Synthetic Intelligence (AI) Famous person Tremendous Micro Pc?

-

Markets3 months ago

Markets3 months agoIf You'd Invested $1,000 in Starbucks Inventory 20 Years In the past, Right here's How A lot You'd Have Immediately

-

Markets3 months ago

Markets3 months agoPrediction: This Transfer From Nvidia within the Second Half Will Be A lot Greater Than the Inventory Break up