Markets

Is Intel Inventory a Hidden Gem or a Worth Lure?

Legacy chipmaker Intel has shed because of the firm’s lackluster efficiency in 2024 and the sizable losses it has been posting. Whereas the bulls suppose Intel is a hidden gem with deep worth, the bears imagine it’s a price lure. So, what’s it precisely? That’s what I’m going to attempt to reply on this article.

To grasp Intel’s state of affairs higher, you will need to be aware that the corporate, recognized for its laptop processors and the x86 structure (the instruction set that dominates private computer systems even right this moment), has lately been dethroned from its kingpin standing within the chips trade. It merely did not sustain with the competitors, however let’s save the historic missteps for an additional time.

Consequently, I’m bearish on Intel due to its sizable losses, its vital money burn, and poor execution.

Intel Faces Widening Losses

Central to my detrimental stance on Intel is the truth that the corporate’s losses are widening. Though I stated I’d save the missteps for an additional time, understanding the explanation behind these losses is essential earlier than we bounce into the numbers.

Going again to the early 2000s, Intel was the go-to store for anybody in search of superior chips, and enterprise was booming. The corporate was the primary to market with the most recent chips up till it acquired too comfy with its standing as a chip kingpin. For example, in 2014, when Barrack Obama was in workplace, Intel delayed the opening of a key location referred to as Fab 42 resulting from a short lived slowdown within the PC market. Little did it know, this choice would price it shedding out to an rising foundry firm that was half its measurement on the time.

Lengthy story brief, Intel misplaced its place to the Avenue’s favourite foundry operator Taiwan Semiconductor Manufacturing Firm . Now let’s dive into the numbers.

In Q2 2024, Intel posted a loss per share of $0.38 and missed Avenue estimates by $0.27. Furthermore, its income additionally fell by 1% yr over yr to $12.8 billion, once more falling in need of market expectations by $148 million. Intel’s foundry enterprise is the most important concern, because it posted an working lack of $2.83 billion, greater than the lack of $1.86 billion a yr in the past.

Including to this, Intel’s share capital is rising, which is simply unhealthy for a loss-making firm. Its diluted shares elevated to 4.26 billion from 4.19 billion a yr in the past. So not solely are you getting extra losses, however you’re additionally getting diluted. Now the bulls will argue that Intel Merchandise is worthwhile, and it was, with $2.9 billion in working revenue in Q2, up from $2.5 billion a yr in the past. Nonetheless, that simply doesn’t do it for me. It’s not sufficient to offset the losses that Intel Foundry has been posting.

Furthermore, Intel has been taking part in catch-up for fairly a while now and it’s nonetheless not near its opponents. The losses that this semiconductor large has been posting are primarily because of the hefty investments it’s making to desperately win its place again. Its CapEx exceeded $11.6 billion throughout Q2 2024 whereas it solely made $1.06 billion in working money stream. This represents an alarmingly excessive burn charge, even with the accomplice contributions of $11.8 billion.

Intel Cuts Prices and Suspends Dividend

Transferring ahead, I’m not a fan of the choices Intel’s administration made after posting one other disappointing quarter. Whereas the corporate could also be attempting to be sensible with capital allocation, it simply doesn’t have a very good monitor document. It has repeatedly delayed amenities and laid off workers prior to now each time it confronted a problem. Through the Q2 2024 earnings name, Intel stated it’s going to put off 15% of its employees by the tip of 2025 to chop prices.

Moreover, Intel stated it’ll droop its dividend at first of This fall 2024, a transfer that wasn’t acquired nicely by the revenue buyers that held the inventory. The corporate defined that it has to take a position that cash into CapEx to catch as much as rivals. It already has a considerable PP&E portion on the money stream assertion, and though it fell yr over yr, its money technology is simply not sufficient to justify it.

Moreover, contemplating how Intel’s semiconductor fabrication crops have been delayed prior to now, I do not need numerous confidence in administration’s capability to be on schedule this time round.

Intel Is a Worth Lure

As I discussed earlier than, I agree with the bears who imagine Intel is a price lure proper now, however let me present you the way. The bulls are arguing that Intel is buying and selling at lower than its guide worth (0.7x TTM P/B), so if it have been to liquidate its enterprise, they’d have some kind of margin of security. Let me settle this with a brief train.

In the event you flip to the stability sheet, you’ll see that Intel has about $206.2 billion in complete belongings, of which $27.4 billion is simply goodwill and one other $4.3 billion is in intangible belongings. So there may be about $32 billion that may’t be capitalized in a liquidation state of affairs.

Now, if you happen to take a look at the present belongings of $50.8 billion after which take away the present liabilities of $32 billion and debt of $48.3 billion, you find yourself with -$29.5 billion. Due to this fact, Intel’s detrimental internet price in a liquidation state of affairs doesn’t give any investor a margin of security.

Lastly, let’s say you might be valuing Intel based mostly on money stream. I see that the inventory is buying and selling at 10.2 occasions its projected working money stream, a 51% low cost to its sector. Can it produce sufficient money stream over the subsequent, say, 10 years? I’m not comfy with assigning Intel multiples and progress charges and projecting thus far out into the long run, given the corporate’s execution prior to now and the way it’s struggling proper now.

From the place I stand proper now, I see a enterprise that has seen its money stream, internet revenue, and gross sales persistently decline over the previous decade. Due to this fact, Intel, in my humble opinion, is a price lure and never in deep worth territory.

Analysts’ View Intel Inventory as a Maintain

On the Avenue, INTC inventory sports activities a consensus “Maintain” score based mostly on 1 Purchase, 26 Maintain, and 6 Promote suggestions. The of $26.09 implies an upside of 32.8% from present ranges.

The Backside Line

In abstract, Intel’s substantial year-to-date losses, rising money burn, and administration’s questionable choices paint a troubling image. Regardless of the low valuation and potential enchantment to worth buyers, the corporate’s monetary instability and previous missteps point out it’s extra of a price lure than a real discount. The widening losses and excessive burn charge from vital investments spotlight the dangers. Moreover, the suspension of dividends and ongoing operational delays add to the considerations. Given Intel’s declining monetary metrics and ineffective restoration efforts, I stay cautious and skeptical about its potential for a turnaround.

(Reuters) -A probe by Hong Kong’s aviation accident investigation company revealed Cathay Pacific’s Airbus A350 engine failed in-flight on account of a ruptured gasoline hose which additionally confirmed indicators of a hearth, the company’s report acknowledged on Thursday.

Hong Kong’s Air Accident Investigation Authority (AAIA) discovered a ruptured gasoline hose within the second engine of the Cathay Pacific-operated A350 jet, with 5 further secondary gasoline hoses additionally exhibiting indicators of damage and tear.

The investigation confirms Reuters’ earlier report which cited sources saying the preliminary checks revealed a hose between a manifold and a gasoline injection nozzle was pierced.

“This critical incident illustrates the potential for gasoline leaks by means of the ruptured secondary gasoline manifold hose, which may lead to engine fires,” the report acknowledged.

A “critical incident” is an investigative time period in aviation that pointed to a excessive chance of an accident.

“If not promptly detected and addressed, this example, together with additional failures, may escalate right into a extra critical engine hearth, doubtlessly inflicting in depth injury to the plane,” AAIA mentioned within the report.

The A350-1000 and XWB-97 engines, manufactured by Rolls-Royce (OTC:), have been beneath the highlight since Cathay’s Zurich-bound passenger flight CX383 was pressured to return to Hong Kong after it acquired an engine hearth warning shortly after take-off on Sept. 2.

Cathay Pacific started inspecting all its Airbus A350 jets after the incident. It was the primary part of its sort to undergo such a failure on any A350 plane worldwide, Cathay mentioned on the time.

Earlier this month, European Union Aviation Security Company (EASA) additionally ordered inspections on engines of Airbus A350-1000 jets because it moved to forestall comparable occasions after consulting regulators and accident investigators in Hong Kong, in addition to Airbus and Rolls-Royce.

The AAIA, in its report, really helpful the EASA to ask Rolls-Royce to proceed giving airworthiness data, together with inspection necessities of the secondary gasoline manifold hoses of its engines to make sure their serviceability.

Cathay didn’t instantly reply to a request for touch upon the investigation’s findings.

The unreal intelligence revolution has been a blended bag for software program firms. Whereas software program shares that harness the ability of enormous language fashions (LLMs) have the potential to speed up revenues, AI additionally offers software program prospects the potential to “do-it-yourself.”

As an illustration, personal buy-now-pay-later firm Klarna just lately introduced it could try and do away with its Salesforce and Workday software program in lieu of constructing its personal CRM and worker administration software program internally, by way of using AI.

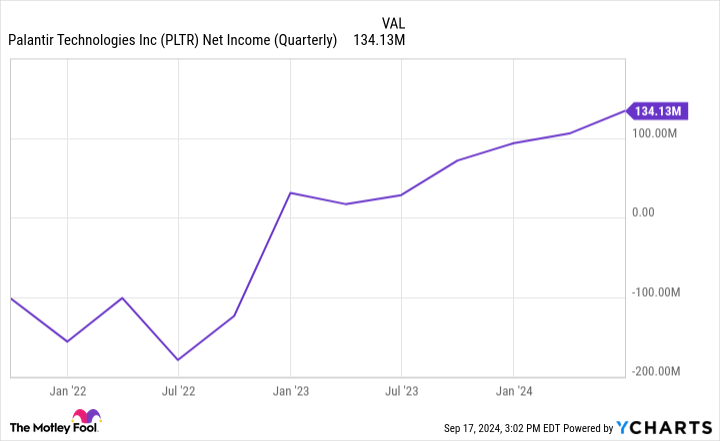

But AI software program platform Palantir (NYSE: PLTR) is exhibiting an acceleration in its business enterprise as a result of introduction of AI. And one Wall Road analyst thinks it has a lot farther to run.

Palantir isn’t any meme inventory

Some buyers have equated Palantir with the revolution, resulting in doubts about its latest run. This could possibly be due to some issues. First, the inventory has a excessive share of retail buyers relative to institutional buyers. Second, Palantir went public in a direct itemizing in late 2020, when rates of interest had been low and lots of doubtful software program and know-how firms bought shares to the general public. Lastly, CEO Alex Karp is considered some as a unusual and outspoken chief, for higher or worse.

However Palantir isn’t any meme inventory. As a proof level, the corporate was just lately admitted to the celebrated S&P 500 index, which has stringent standards for admission. Previously couple years, Palantir has certified for the index by posting constant GAAP profitability — considerably uncommon for a software program inventory.

information by

AI is resulting in a reacceleration in progress

As well as, Palantir has seen its income progress speed up. That acceleration coincided with the introduction of the Palantir Synthetic Intelligence Platform, or “AIP,” a few 12 months in the past. AIP permits firms to include third-party LLMs or different specialised fashions immediately into Palantir’s current Gotham or Foundry software program platforms.

AIP has invigorated curiosity in Palantir’s software program, particularly from business prospects, leading to a reacceleration of income progress since AIP was launched.

Usually, it is more durable for firms to extend their progress charge as they get greater due to the legislation of enormous numbers. Nevertheless, one can see that Palantir has defied this development. The introduction of AIP and Palantir fine-tuning its advertising technique to incorporate periodic, “boot camps,” are possible causes for the inflection. These boot camps permit potential prospects to carry their precise information and expertise the AIP in a trial with Palantir’s engineers.

One analyst sees $50 in Palantir’s future

At present, most of Wall Road is definitely bearish on Palantir’s inventory. As of August, solely six out of 18 analysts charge shares a Purchase or Robust Purchase, with one other six ranking shares Impartial and the remaining six ranking shares a Promote. The common value goal on shares is $27, under the $36 present value as of this writing. That is in all probability attributable to Palantir’s inventory having greater than doubled this 12 months, whereas at present buying and selling at an costly valuation of roughly 35 instances gross sales.

However one analyst, Mariana Perez Mora of Financial institution of America charges shares a Purchase, with a street-high $50 value goal on the inventory. The analyst believes Wall Road misunderstands Palantir, and sees large issues within the firm’s future, justifying the next inventory value.

Mora thinks others miss how differentiated Palantir is relative to different enterprise software program shares, each product-wise and the way Palantir goes to market. Of observe, Palantir usually has members of its R&D staff embed themselves with a buyer first, with a view to perceive a buyer’s enterprise issues and ache factors. Then, Palantir tailors its modular software program to that enterprise’ particular infrastructure, making its information analytics capabilities extra related to every particular person buyer. In its annual report, Palantir notes seeks out “dangerous and resource-intensive” engagements the place different opponents could draw back.

Mora believes this technique, which is harder upfront and the place Palantir would not see instant revenues, finally pays off. It’s because the upfront work permits Palantir extra pricing energy in a while. She then sees Palantir’s merchandise spreading to extra industries as Palantir rolls out industry-specific platforms, such because the upcoming Warp Velocity for manufacturing companies.

An industry-standard OS like Home windows?

Whereas Palantir was previously referred to as a specialised software program platform for the Protection {industry} within the Struggle on Terror, Mora sees Palantir changing into an industry-standard platform sooner or later, calling it, “the widespread information operational system for the U.S. authorities and enormous U.S. companies.”

If Palantir’s latest continues, she could very nicely find yourself being appropriate. With nearly all of revenues nonetheless coming from the Protection {industry}, Palantir’s latest penetration of the a lot bigger enterprise market offers it the prospect to maintain progress charges excessive for some time, doubtlessly justifying immediately’s lofty inventory value.

Do you have to make investments $1,000 in Palantir Applied sciences proper now?

Before you purchase inventory in Palantir Applied sciences, contemplate this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they imagine are the for buyers to purchase now… and Palantir Applied sciences wasn’t certainly one of them. The ten shares that made the lower may produce monster returns within the coming years.

Think about when Nvidia made this checklist on April 15, 2005… if you happen to invested $1,000 on the time of our suggestion, you’d have $708,348!*

Inventory Advisor gives buyers with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 16, 2024

Financial institution of America is an promoting companion of The Ascent, a Motley Idiot firm. and/or his purchasers have positions in Financial institution of America. The Motley Idiot has positions in and recommends Financial institution of America, Palantir Applied sciences, Salesforce, and Workday. The Motley Idiot has a .

was initially revealed by The Motley Idiot

By Sheila Dang

(Reuters) – Billionaire Elon Musk has endorsed Republican former President Donald Trump within the race for the White Home, however staff at his assortment of corporations are largely donating to Trump’s Democratic rival Kamala Harris.

Staff at Tesla (NASDAQ:) have contributed $42,824 to Harris’ presidential marketing campaign versus $24,840 to Trump’s marketing campaign, in line with OpenSecrets, a nonpartisan nonprofit that tracks U.S. marketing campaign contributions and lobbying information.

Staff at Musk’s rocket firm SpaceX have donated $34,526 to Harris versus $7,652 to Trump. Staff on the social media platform X, previously often called Twitter, have donated $13,213 to Harris versus lower than $500 to Trump.

Whereas the figures are comparatively small for marketing campaign fundraising, they point out political leanings at odds with Musk’s personal. The world’s richest man, Musk has boosted Trump on X and dismissed left-leaning concepts as a “woke-mind virus.”

Musk didn’t instantly reply to a request for remark. He backed President Joe Biden in 2020 however has tacked rightward since then. Trump has stated that if he wins the Nov. 5 election, he’ll appoint Musk to steer a authorities effectivity fee.

The OpenSecrets information consists of donations from firm staff and house owners and people people’ quick members of the family. Marketing campaign finance legal guidelines prohibit corporations themselves from donating to federal campaigns.

A lot of Musk’s staff are primarily based in California, a Democratic stronghold, stated Ross Gerber, CEO of Gerber Kawasaki Wealth and Funding Administration, which is a Tesla shareholder. Gerber can be an investor in X.

In July, Musk stated he would transfer X and SpaceX headquarters to Texas from California due to a California gender-identity legislation he known as the “final straw.” Gerber stated such a transfer would imply “shedding out on loads of potential expertise” in California.

Hong Kong probe reveals Cathay Airbus engine failure on account of ruptured gasoline hose

Palantir Inventory Is Skyrocketing. 1 Analyst Thinks It Has One other 38% Achieve Forward.

Staff at Musk's Tesla, SpaceX and X donate to Harris whereas he backs Trump

Bitcoin climbs with US fairness futures as merchants digest Fed lower

Alibaba accelerates AI push by releasing new open-source fashions, text-to-video

Evaluation-After jumbo Fed price minimize, market hopes experience on US smooth touchdown

Nintendo, Pokemon sue 'Palworld' producer for patent infringement

Fed outsized fee minimize attracts muted response, however calm could not final

UN advisory physique makes seven suggestions for governing AI

The inventory market received simply what it wished from the Fed

Asian shares rise following bumper Fed reduce; Nikkei rallies as yen retreats

The inventory market dipped after a historic Fed price minimize. Right here’s what the specialists assume

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoInventory market in the present day: US futures slip as Micron slides, with information on deck

-

Markets3 months ago

Markets3 months agoFutures dip as Micron drags down chip shares forward of financial information

-

Markets3 months ago

Markets3 months agoApogee shares rise almost 4% on upbeat steering and earnings beat

-

Markets3 months ago

Markets3 months agoWhy Is Micron Inventory Down After a Double Earnings Beat?

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoHungary central financial institution tells lenders to reimburse purchasers after Apple glitch

-

Markets3 months ago

Markets3 months agoSoftBank to spend money on search startup Perplexity AI at $3 billion valuation, Bloomberg experiences

-

Markets3 months ago

Markets3 months agoInventory market at present: Asian shares decrease after Wall Avenue closes one other profitable week

-

Markets3 months ago

Markets3 months agoThe AI market alternative: UBS provides a bottom-up perspective

-

Markets3 months ago

Markets3 months ago3 No-Brainer Synthetic Intelligence (AI) Shares to Purchase With $500 Proper Now

-

Markets3 months ago

Markets3 months agoNeglect Nvidia: Distinguished Billionaires Are Promoting It in Favor of These 7 High-Notch Shares