Markets

Overlook Nvidia — This Semiconductor Inventory Is a A lot Higher Worth

Nvidia is a superb firm and a fantastic inventory, nevertheless it at the moment trades on barely greater than 50 instances Wall Road’s 2024 earnings estimates. That is positive for a lot of buyers keen to pay a premium for a high-quality progress inventory, however for buyers who’re keen to take some near-term danger on board, ON Semiconductor (NASDAQ: ON) could be a greater possibility. Here is why.

Cyclicality issues for semiconductor shares

Semiconductors are extremely cyclical; they at all times have been and at all times can be. That is as a result of the very first thing their clients do after they see demand selecting up is order chips to organize for a manufacturing ramp. Conversely, after they see a slowdown coming the very first thing they do is cease or cancel chip orders as they put together to sluggish manufacturing.

As such, semiconductors are at all times early bellwethers of their finish markets. Nevertheless, not all finish markets are made equal, and this yr, the new space of spending has been round synthetic intelligence (AI) and the high-performance computing (HPC) chips essential to energy it. That is why Nvidia has finished so nicely and why Taiwan Semiconductor Manufacturing continues to outperform, led by in its HPC gross sales.

ON Semiconductor’s positioning

Nevertheless, ON Semiconductor’s key finish markets, industrial and automotive, stay difficult, which is why the corporate’s inventory worth is down 21% over the past yr. I am going to come again to that time in a second, however first, just a few phrases on the corporate itself for these unfamiliar with it.

The funding case is predicated on administration repositioning the corporate for progress in thrilling long-term progress markets, and that is greatest seen in its silicon carbide operations. Administration has invested closely in positioning itself within the silicon carbide enterprise, not least by lately asserting a multiyear $2 billion funding in a silicon carbide (SiC) manufacturing facility in central Europe. Silicon carbide chips supply a number of advantages over conventional silicon chips, and notably on the larger voltages wanted for (EVs).

As well as, the chip firm has positioned itself in different thrilling progress markets in new applied sciences the place it has comparatively excessive content material, together with manufacturing facility automation, EV charging, renewable power infrastructure, 5G, and superior driver help techniques (ADAS).

ON Semiconductor’s challenges

Sadly, whereas these finish markets have nice long-term progress potential, they’re slowing in 2024. The impression of the slowdown is greatest seen within the firm’s declining gross sales and within the slowdown in its silicon carbide enterprise. EV gross sales progress has tailed off as persistently excessive rates of interest have made automobile loans dearer. As such, automakers have pared again funding in EVs, and the corporate’s gross sales have been negatively impacted.

For instance, again in October, administration stated {that a} discount in demand from one unique tools producer (OEM) automotive buyer would outcome within the firm solely hitting $800 million in 2023 somewhat than the goal of $1 billion. Quick ahead to February, and CEO Hassane El-Khoury instructed buyers, “OEM’s newest EV plans point out a extra tapered progress signaling a SiC market progress within the vary of 20% to 30%” in comparison with market reviews calling for “30% or 40% progress for silicon carbide in 2024.”

In an indication of a declining market, El-Khoury up to date buyers in April and stated he nonetheless anticipated the silicon carbide complete addressable market to extend in 2024, “though at a decrease charge than beforehand anticipated.”

Whereas he famous that there have been indicators of demand stabilization, he was fairly clear that “I am not going to name the underside. I used to be very clear final time. I am going to name it after I’m sitting on the highest on the opposite facet.”

As such, anybody considering of shopping for in wants to understand that there is potential for some unfavourable near-term information stream.

Two causes to purchase ON Semiconductor

For those who can tolerate the near-term danger, the inventory is very engaging. In any case, nobody disputes that EVs are the way forward for the trade. All it’ll take is a decrease interest-rate surroundings for EV gross sales to choose up, and so will EV funding. As well as, the opposite focused finish markets referenced all have glorious long-term progress prospects.

In the meantime, ON Semiconductor’s valuation multiples are undemanding. Buying and selling on 18.3 instances estimated earnings, the corporate appears to be like like a superb worth. Whereas there isn’t any assure it’ll make these numbers, and as El-Khoury notes, it is arduous to forecast the underside out there, it is a fairly secure wager that ON Semiconductor’s finish markets and gross sales will recuperate in keeping with conventional cyclicality.

Given that every one the corporate has to do is meet Wall Road estimates to seem like an excellent worth, I’d argue the danger/reward calculation favors shopping for the inventory for enterprising buyers.

Do you have to make investments $1,000 in ON Semiconductor proper now?

Before you purchase inventory in ON Semiconductor, think about this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they consider are the for buyers to purchase now… and ON Semiconductor wasn’t one in all them. The ten shares that made the minimize may produce monster returns within the coming years.

Think about when Nvidia made this checklist on April 15, 2005… if you happen to invested $1,000 on the time of our advice, you’d have $791,929!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of July 8, 2024

has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Nvidia and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends ON Semiconductor. The Motley Idiot has a .

was initially revealed by The Motley Idiot

Shopping for and holding prime shares for an extended, very long time is among the finest methods to become profitable within the inventory market, as a result of this technique permits buyers to capitalize on secular development developments and likewise helps them profit from the facility of compounding.

For example, a $500 funding made within the Nasdaq-100 Know-how Sector index a decade in the past is now value $2,300, translating into annual development of 16% throughout this era. So, if in case you have $500 to spare proper now after paying off your payments, clearing costly loans, and saving sufficient for tough occasions, it could be a good suggestion to place that cash into shares of corporations which can be benefiting big-time from the rising adoption of .

That is as a result of the worldwide AI market is forecast to develop at an annual price of 28% via 2030, producing virtually $827 billion in annual income on the finish of the last decade. The adoption of this expertise is about to influence a number of industries, starting from cloud computing to digital promoting.

On this article, I’ll study the prospects of two corporations which can be working in these niches and are already benefiting from the quickly rising adoption of AI to see why it could make sense to speculate $500 in them (both individually or mixed).

1. The Commerce Desk

The Commerce Desk (NASDAQ: TTD) operates a programmatic, cloud-based promoting platform that helps advertisers buy advert stock and handle and optimize their campaigns throughout varied channels corresponding to video, cellular, e-commerce, related tv, and others. The Commerce Desk’s automated platform makes use of real-time information to assist drive stronger returns on investments for advertisers in order that they will buy and show the proper advertisements to the proper viewers on the right time.

It’s value noting that the corporate operates in a fast-growing area of interest because the programmatic promoting market is anticipated to generate incremental income of $725 billion between 2023 and 2028 at a compound annual development price of 39%, as per TechNavio. The Commerce Desk has been counting on AI to seize this large end-market alternative.

The corporate launched its AI-enabled programmatic advert platform Kokai in June 2023. Kokai analyzes 13 million advert impressions each second in order that it may “assist advertisers purchase the fitting advert impressions, on the proper worth, to succeed in the audience at the most effective time.” The great half is that The Commerce Desk’s prospects are already witnessing an enchancment of their returns on advert {dollars} spent due to Kokai.

On its August , The Commerce Desk administration identified:

Solimar is The Commerce Desk’s programmatic advert platform that was launched in 2021. So, it will not be stunning to see extra of the corporate’s prospects transferring to the AI-enabled Kokai given the numerous enchancment in advert efficiency that it’s delivering. Extra importantly, The Commerce Desk’s concentrate on integrating AI has allowed it to speed up its development as effectively.

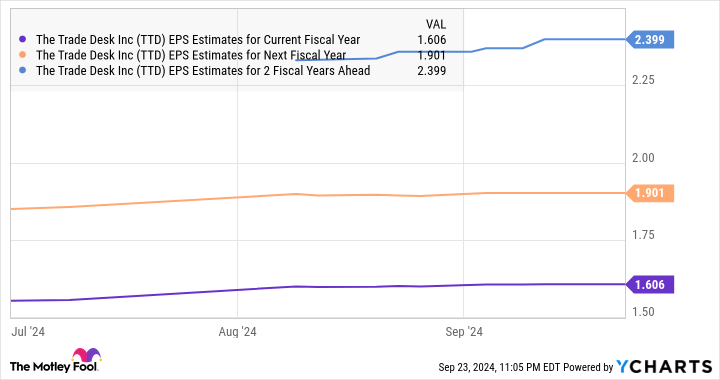

The corporate’s income within the second quarter of 2024 elevated 26% 12 months over 12 months to $585 million as in comparison with the 23% development it recorded in the identical quarter final 12 months. Its adjusted earnings elevated at a quicker tempo of 39% from the identical quarter final 12 months to $0.39 per share. The corporate’s income forecast of $618 million for Q3 would translate into 27% development from the identical quarter final 12 months, suggesting that its top-line development is on monitor to speed up within the present quarter.

The great half is that analysts expect The Commerce Desk’s earnings development price to select up sooner or later.

information by

The corporate is anticipated to clock an annual earnings development price of 26% for the following 5 years, however current developments and the massive addressable alternative within the programmatic promoting market (which The Commerce Desk administration pegs at $1 trillion) recommend that it may outperform consensus estimates.

The market has rewarded The Commerce Desk inventory with 50% positive factors in 2024 up to now due to its bettering development profile, and its brilliant prospects recommend that it may maintain flying greater. That is why investing $500 in The Commerce Desk may develop into a wise long-term transfer proper now contemplating that it has a worth/earnings-to-growth ratio (PEG ratio) of 0.6, which signifies that it’s undervalued with respect to the expansion that it’s forecasted to ship.

2. Oracle

The cloud computing market has been an enormous beneficiary of the rising AI adoption within the preliminary days, Grand View Analysis estimates that the cloud AI market may develop at an annual price of 40% via 2030 to generate income of $647 billion on the finish of the forecast interval. Oracle (NYSE: ORCL) is getting an enormous increase due to the fast development of the cloud AI market, as evident from the corporate’s current outcomes.

Oracle’s cloud income within the first quarter of fiscal 2025 (which ended on Aug. 31) elevated 21% 12 months over 12 months to $5.6 billion, outpacing the corporate’s complete income development of 8% to $13.3 billion. Extra particularly, the Oracle Cloud Infrastructure (OCI) enterprise recorded terrific year-over-year development of 45% to $2.2 billion.

OCI is the corporate’s infrastructure-as-a-service (IaaS) enterprise via which it rents out its cloud infrastructure to prospects seeking to practice AI fashions. Administration factors out that this enterprise now has an annual income run price of $8.6 billion and demand for OCI is exceeding provide. The demand for Oracle’s cloud infrastructure providing is so robust that its remaining efficiency obligations (RPO) shot up a terrific 52% 12 months over 12 months within the earlier quarter to $99 billion.

RPO is the entire worth of an organization’s future contracts which can be but to be fulfilled, and it’s value noting that AI is taking part in a central function in driving this metric greater. Oracle factors out that its “cloud RPO grew greater than 80% and now represents almost three-fourths of complete RPO.”

Contemplating the massive alternative that is current within the cloud AI market, it will not be stunning to see demand for Oracle’s cloud infrastructure improve at a sturdy tempo for a very long time to return. That is additionally the rationale why consensus estimates are projecting Oracle’s income to extend by double digits over the following three fiscal years following a top-line soar of simply 6% in fiscal 2024 to $53 billion.

information by

Oracle is up 57% up to now in 2024. Traders would do effectively to behave shortly so as to add this cloud inventory to their portfolios as it’s nonetheless buying and selling at a gorgeous 27 occasions ahead earnings, a small low cost to the Nasdaq-100 index’s ahead earnings a number of of 29. Its large addressable market and the immense measurement of its backlog that is rising on account of the fast adoption of cloud AI providers is prone to result in extra inventory worth upside sooner or later.

Do you have to make investments $1,000 in The Commerce Desk proper now?

Before you purchase inventory in The Commerce Desk, contemplate this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they imagine are the for buyers to purchase now… and The Commerce Desk wasn’t one in all them. The ten shares that made the reduce may produce monster returns within the coming years.

Take into account when Nvidia made this record on April 15, 2005… should you invested $1,000 on the time of our suggestion, you’d have $760,130!*

Inventory Advisor offers buyers with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Oracle and The Commerce Desk. The Motley Idiot has a .

was initially revealed by The Motley Idiot

(Reuters) – The Worldwide Affiliation of Machinists and Aerospace Staff (IAM) mentioned late on Friday that its pay deal talks with Boeing (NYSE:) had damaged off and that there have been no additional dates scheduled for negotiations presently.

“We stay open to talks with the corporate, both direct or mediated,” IAM mentioned in a put up on X.

Boeing stays dedicated to resetting its relationship with its represented staff and desires to “attain an settlement as quickly as attainable,” a spokesperson for the corporate mentioned in an e-mail. “We’re ready to fulfill at any time.”

Greater than 32,000 Boeing staff within the Seattle space and Portland, Oregon, walked off the job on Sept. 13 within the union’s first strike since 2008, halting manufacturing of airplane fashions together with Boeing’s best-selling 737 MAX.

The union is looking for a 40% pay rise and the restoration of a defined-benefit pension that was taken away within the contract a decade in the past.

Boeing made an improved provide to the hanging staff on Monday that it described as its “finest and remaining”, which might give staff a 30% increase over 4 years and restored a efficiency bonus, however the union mentioned a survey of its members discovered that was not sufficient.

SEC Chair Gensler Confronted Intense Scrutiny on Capitol Hill

On Wednesday, September 25, all 5 SEC Commissioners gave testimony at a US Home Committee on Monetary Companies Committee listening to on Capitol Hill. Committee Chair Patrick McHenry set the tone for the listening to, stating that the SEC has turn into a rogue company underneath Chair Gensler.

Home majority whip Tom Emmer referenced the notorious Debt Field case, saying,

“Your attorneys, who little doubt heard your anti-crypto rhetoric, which isn’t primarily based in legislation, went out and intentionally lied to a court docket with a purpose to effectuate the instructions from their Chair to prosecute crypto firms. Chair Gensler, have you learnt of some other time in historical past the place the SEC has been sanctioned by a court docket for materials misrepresentation?”

Different Commissioners supplied their views on the SEC’s mantra of regulation via enforcement.

SEC Commissioner Hester Peirce referenced the SEC vs. Binance case. She stated that the SEC failed in its obligation as a regulator through the use of imprecise language. Moreover, she admitted the company ought to have admitted that the crypto itself isn’t a safety a very long time in the past.

On September 13, 2024, the SEC requested the court docket’s permission to amend the Binance criticism, clarifying its place on crypto asset securities. In a footnote, the SEC said,

“The SEC isn’t referring to the crypto asset itself because the safety; fairly the SEC has persistently maintained because the very first crypto Howey case the SEC litigated, the time period is shorthand. […] However, to keep away from any confusion, the PAC now not makes use of the shorthand time period and regrets any confusion it might have invited on this regard.”

Chair Gensler might face additional scrutiny following Vice President Kamala Harris’s latest assist for US digital belongings.

Received $500? 2 Monster Synthetic Intelligence (AI) Shares to Purchase Proper Now

Boeing wage talks break off with out progress to finish strike, union says

Crypto Spot ETF Inflows, SEC Enchantment and XRP, Gensler Grilling – This Week in Crypto

The inventory market's euphoria-driven file highs are prone to a painful downturn, 'Black Swan' investor says

US southeast faces daunting activity cleansing up from Helene; demise toll rises

Watch these warning indicators for a possible peak within the inventory market's long-term bull rally, NDR says

TD Financial institution nears doable responsible plea in cash laundering probe, WSJ reviews

Trump Media & Expertise Group (DJT) Inventory: Hypothesis-Pushed Valuation Make it a Promote

Binance founder Zhao launched from US custody, Bloomberg Information reviews

Warren Buffett’s BofA Promoting Spree Edges Towards Key Milestone

Apple drops out of talks to affix OpenAI funding spherical, WSJ says

Why Nvidia inventory might soar over 500% by the tip of the last decade, former consulting exec says

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoDown 30% From Its All-Time Excessive, Ought to You Purchase Synthetic Intelligence (AI) Famous person Tremendous Micro Pc?

-

Markets3 months ago

Markets3 months agoADP Stories Decrease-Than-Anticipated Personal Payroll Progress for June

-

Markets3 months ago

Markets3 months agoSorry, however retiring ‘comfortably’ on $100K is a fantasy for most individuals. Right here’s why.

-

Markets3 months ago

Markets3 months agoAbove Food Corp. (NASDAQ: ABVE) and Chewy Inc. (NYSE: CHWY) Making Headlines This Week

-

Markets3 months ago

Markets3 months agoSouthwest Air adopts 'poison tablet' as activist investor Elliott takes important stake in firm

-

Markets3 months ago

Markets3 months agoCore Scientific so as to add 15 EH/s by means of Block’s 3nm Bitcoin mining ASICs

-

Markets3 months ago

Markets3 months agoWarren Buffett is popping 94 subsequent month. Ought to Berkshire traders begin to fear?

-

Markets3 months ago

Markets3 months agoWhy Rivian Inventory Roared Forward 10% on Friday

-

Markets3 months ago

Markets3 months agoArgentina to Promote {Dollars} In Parallel FX Market, Caputo Says

-

Markets3 months ago

Markets3 months agoWhy Intel Inventory Popped on Friday