Markets

RTX's Collins in talks to drop ISS spacesuit contract with NASA, sources say

By Joey Roulette

WASHINGTON (Reuters) -RTX Corp subsidiary Collins Aerospace is in talks with NASA to again out of its contract to construct new spacesuits for astronauts on the Worldwide House Station, a setback because the company struggles with its decades-old spacewalking fits, in keeping with two individuals aware of the discussions.

The contract was a part of $3.5 billion NASA awarded to each Collins and Axiom House in 2022 to construct new spacesuits for the ISS and future moon missions. Collins bought an preliminary $97 million underneath this system for ISS go well with growth, whereas it may vie with Axiom to get further funds to work on lunar spacesuits.

However Collins’ function in this system has been bumpy and growth has fallen delayed, and the corporate has been in talks with NASA officers on tips on how to wind down its function in this system, the 2 individuals stated.

“After an intensive analysis, Collins Aerospace and NASA mutually agreed to descope Exploration Extravehicular Exercise Providers (xEVAS) process orders,” a Collins spokeswoman stated in a press release, referring to the spacesuit contract.

NASA didn’t instantly reply to a request for remark.

The spacesuit woes add to an extended historical past of difficulties NASA has confronted in modernizing what are basically human-shaped spacecraft – cumbersome, advanced techniques U.S. astronauts use to enterprise outdoors of the ISS some 250 miles (400 km) above Earth for routine repairs on the soccer field-sized lab’s exterior.

The talks to finish Collins’ contract come at a troublesome time for NASA because it suffers a uncommon streak of astronaut spacewalk cancellations on the ISS this month due to its present, some 40-year-old, spacesuits, that are managed by Collins.

The company stated a “spacesuit discomfort challenge” compelled the cancellation of two astronauts deliberate spacewalk on June 13 simply earlier than it was poised to start. Then a second try on the spacewalk, on Monday, was canceled minutes into the six-hour mission due to a water leak in U.S. astronaut Tracy Dyson’s go well with.

“There’s water all over the place … I bought an arctic blast throughout my visor,” Dyson reported to mission management.

Previous spacewalks have been known as off over points with the station’s spacesuits, which have solely had minor redesigns and refurbishments since their conception practically half a century in the past. NASA’s inspector basic and its unbiased Aerospace Security Advisory Panel have lengthy pushed the company to improve them.

Collins’ backing out of the brand new spacesuit program seems to place NASA’s future fits within the fingers of Axiom, a startup managing astronaut flights and constructing its personal house station. Axiom didn’t instantly return a request for remark.

Markets

If You Purchased 1 Share of Nvidia at Its IPO, Right here's How Many Shares You Would Personal Now

Since its IPO in January 1999, Nvidia (NASDAQ: NVDA) has established itself as one of many world’s most profitable firms. It has been notably adept at adapting its expertise to increase into new markets.

The corporate pioneered the that revolutionized the gaming business, turning boxy figures into lifelike pictures. The key to its success was parallel processing, which allowed the chips to conduct a large number of mathematical calculations concurrently. Nvidia’s processors are actually used for product design, autonomous methods, cloud computing, information facilities, synthetic intelligence (AI), and extra.

The flexibility to adapt its expertise has been a boon to shareholders. Even when buyers did not get in on the IPO itself, Nvidia shares fell beneath their challenge worth quite a few occasions in early 1999. For buyers lucky sufficient to get shares at (or beneath) the $12 IPO worth, the inventory has returned 493,940%.

Multiplying like rabbits

Whereas a single share of inventory may appear inconsequential at first look, one share of the proper inventory can have a huge effect on an investor’s success. In Nvidia’s case, the corporate’s efficiency and hovering inventory worth have resulted in quite a few inventory splits, turning one share into many extra.

Here is a listing of Nvidia’s inventory splits over time:

-

2-for-1 cut up, June 27, 2000

-

2-for-1 cut up, Sept. 12, 2001

-

2-for-1 cut up, April 7, 2006

-

3-for-2 cut up, Sept. 11, 2007

-

4-for-1 cut up, July 20, 2021

-

10-for-1 cut up, June 10, 2024

Because of the a number of inventory splits, an investor who purchased only one share of Nvidia inventory close to its IPO in 1999 would now be the proud proprietor of 480 shares.

Nevertheless, it took an excessive amount of self-discipline and self-control to carry Nvidia for greater than 25 years and reap this windfall. The inventory has misplaced greater than half its worth on quite a few events, which despatched fair-weather buyers scrambling for the exits.

That stated, take into account this: A $1,000 funding in Nvidia made in early 1999 would now be value greater than $4.9 million.

Must you make investments $1,000 in Nvidia proper now?

Before you purchase inventory in Nvidia, take into account this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the for buyers to purchase now… and Nvidia wasn’t considered one of them. The ten shares that made the reduce might produce monster returns within the coming years.

Contemplate when Nvidia made this listing on April 15, 2005… in case you invested $1,000 on the time of our advice, you’d have $743,952!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has positions in Nvidia. The Motley Idiot has positions in and recommends Nvidia. The Motley Idiot has a .

was initially revealed by The Motley Idiot

When most buyers take a look at Altria (NYSE: MO) what they see is a large 8% dividend yield backed by a dividend that has been elevated for years. That’s the kind of story that almost all dividend buyers will discover engaging. However there is a huge danger right here as a result of the corporate’s core enterprise is in long-term decline. That danger needs to be understood, however there’s one other delicate twist that you’ll have missed.

Altria’s enterprise is slipping away

It should not come as any shock to Altria shareholders that the corporate’s most necessary enterprise is making . Within the first half of 2024, the corporate generated roughly $11.8 billion in income. Its smokeable merchandise division’s revenues had been about $10.4 billion, or 88% of the corporate’s general prime line. Clearly, smokeable merchandise is the driving pressure at Altria.

To be truthful, the corporate sells quite a lot of smokeable merchandise, together with cigars. However whenever you take a look at quantity, cigarettes account for simply over 97% of the division’s quantity. So cigarettes are the large story at Altria. However, as famous, most buyers know that reality.

The necessary story right here is not the biggest enterprise. It’s the decline that is going down within the largest enterprise. By means of the primary six months of 2024, cigarette volumes dropped 11.5%. That is horrible and would seemingly be seen as surprising at another — buyers would run for the hills. Solely that drop is simply par for the course.

In 2023, cigarette volumes declined 9.9%. In 2022, volumes fell 9.7%. In 2021, the drop was 7.5%. You get the concept, it is a dying enterprise.

One “little” downside that may’t be missed

How has an organization with a enterprise that is in decline managed to take care of its dividend, not to mention develop it? The reply is that, due to the character of cigarettes, people who smoke are typically very loyal. So Altria has been jacking up costs frequently to offset the quantity declines. That is labored out effectively thus far, however you may solely milk a money cow so exhausting earlier than it runs dry. That is a much bigger danger for Altria than many might notice.

Of the cigarettes Altria sells, solely about 4% or so fall into the low cost class. Which means Altria’s enterprise is principally reliant on premium smokes. Within the premium class, “different premium” manufacturers make up about 4.5% of whole quantity. The remaining 91% of the corporate’s cigarette quantity is all attributable to at least one model, Marlboro.

Marlboro is a huge within the U.S. cigarette trade with an enormous 42% market share. This may very well be considered as a power. However step again for a second and take into consideration the large image. Altria is principally a one-trick pony in a dying rodeo. And its pony is likely one of the costliest round at a time when worth competitors from smoking alternate options is heating up. Altria itself notes that “the expansion of illicit e-vapor merchandise” is a giant downside, which is essentially as a result of they’re less expensive.

Fixing the issue will not be straightforward

There’s solely a lot Altria can do about its reliance on Marlboro because the cigarette enterprise declines. In reality, being the most important participant within the trade might be preferable to having a second rung model. What it’s doing is making an attempt to broaden its attain past cigarettes. That is the correct factor to do, however given the scale of the corporate’s cigarette enterprise it is not going to be straightforward to discover a alternative. After a few failed makes an attempt, together with an funding in Juul and in a marijuana firm, Altria is at present centered on rising its current NJOY vape acquisition.

It’s going effectively, with NJOY experiences fast development because it has been slotted into Altria’s spectacular distribution system. To place a quantity on that, within the second quarter of 2024 NJOY’s cargo quantity elevated 14.7% from the primary quarter and NJOY system shipments elevated 80%. The issue is that NJOY is tiny, falling into Altria’s “all different merchandise” income class which made up simply $22 million in income within the first half of 2024 at an organization with almost $11.8 billion in income. So NJOY is barely even a rounding error. Marlboro is the important thing to Altria’s future and can seemingly stay the important thing for years to come back.

If Altria hits a tipping level, it may get unhealthy quick

A shopper staples firm can solely elevate costs simply thus far earlier than there is a backlash from shoppers. The straightforward swap with cigarettes is to purchase cheaper smokes, which Altria actually does not promote. Then there’s alternate options to fret about, reminiscent of the corporate’s spotlight of vaping. Though Marlboro has been holding its personal, in 2021 its market share was 43.1%. That is 1.1 share factors above its present stage.

If Marlboro falters, Altria may fall. This can be a “little” undeniable fact that many buyers most likely aren’t contemplating as they take a look at the large dividend yield. Principally, there’s higher focus danger right here than many individuals notice.

Do you have to make investments $1,000 in Altria Group proper now?

Before you purchase inventory in Altria Group, take into account this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they imagine are the for buyers to purchase now… and Altria Group wasn’t one among them. The ten shares that made the minimize may produce monster returns within the coming years.

Take into account when Nvidia made this checklist on April 15, 2005… when you invested $1,000 on the time of our suggestion, you’d have $743,952!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has no place in any of the shares talked about. The Motley Idiot has no place in any of the shares talked about. The Motley Idiot has a .

was initially printed by The Motley Idiot

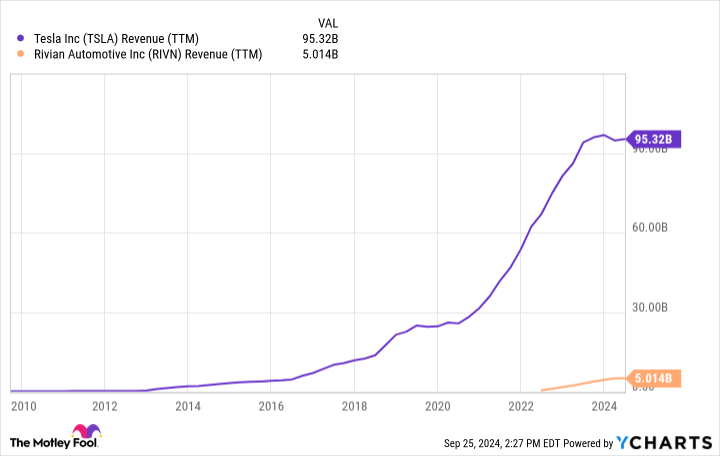

Everybody desires to search out the following Tesla (NASDAQ: TSLA). However investing within the electrical car (EV) area will be tough. Many EV corporations have gone bankrupt through the years, and separating the nice from the dangerous will be tough.

Fortunately, Tesla established a transparent template for achievement. And proper now, there’s one that appears extraordinarily enticing. However there’s just one funding technique prone to succeed.

That is how Tesla grew to become an enormous success

In 2006, Tesla CEO Elon Musk revealed “The Secret Tesla Motors Grasp Plan” to the general public. “As you realize, the preliminary product of Tesla Motors is a high-performance electrical sports activities automotive known as the Tesla Roadster,” his essay started. “Nevertheless, some readers might not be conscious of the truth that our long run plan is to construct a variety of fashions, together with affordably priced household automobiles.”

Musk summarized the grasp plan for Tesla:

Immediately, Tesla is a big image of success in the case of executing on long-term visions. The Tesla Roadster was a hit, however given its $100,000-plus value level, its market was all the time small.

Tesla wanted to show its manufacturing chops, and present the general public that EVs could possibly be cool and thrilling. It used this success to design, construct, and ship two new fashions: The Mannequin S and Mannequin X. These fashions had been nonetheless costly, however launched Tesla to lots of of hundreds of recent house owners.

Tesla then used its repute and entry to capital to debut two new mass market fashions, the Mannequin 3 and Mannequin Y. These two fashions, with way more inexpensive value factors, allowed Tesla to develop its by greater than 1,000% during the last decade.

Tesla’s grasp plan labored wonders for its valuation. The corporate is at present price round $800 billion. One other firm, in the meantime, is valued at simply $11 billion — but it is executing Tesla’s confirmed grasp plan flawlessly.

Rivian could possibly be the following huge EV inventory

On the subject of following Tesla’s template for achievement, few EV corporations look as enticing as Rivian (NASDAQ: RIVN).

In 2018, Rivian introduced the debut of its R1T and R1S fashions. Like Tesla’s earlier fashions, the R1T and R1S had been ultra-luxury, high-quality, no-compromise autos with value factors that would simply surpass $100,000 with sure choices. Shopper suggestions was implausible. Shopper Studies discovered that Rivian has the best buyer satisifcation and loyalty ranges of any auto producer — electrical or in any other case. Round 86% of Rivian house owners stated they might purchase one other Rivian. No different model was above the 80% mark.

What’s going to Rivian do with its newfound repute and gross sales base? Precisely what Tesla did: Construct extra inexpensive automobiles. Earlier this 12 months, the corporate revealed three new fashions: The R2, R3, and R3X. All are anticipated to debut with beginning costs beneath $50,000. It was assembly this value level that helped put Tesla on the map for hundreds of thousands of individuals. If Rivian can execute, it ought to show very profitable.

If Rivian can replicate Tesla’s success, why is its market cap hovering simply above $10 billion? First, its new fashions aren’t anticipated to hit the highway till 2026 on the earliest. Second, the required manufacturing services aren’t even full but. Third, the corporate remains to be dropping cash at a speedy clip since car manufacturing is capital intensive. Nevertheless, administration expects to achieve optimistic gross income by the tip of 2024. Lastly, Rivian is attempting to compete in a market section — electrical autos — that has seen many bankruptcies through the years.

It is clear that the market is skeptical of Rivian’s plans, despite the fact that it’s executing on a confirmed mannequin for development, and has demonstrated its means to fabricate autos that clients love. The following few years, nonetheless, will probably be pivotal. Rivian will turn out to be a family identify like Tesla if it could execute, a end result that can possible see a speedy enlargement in its valuation.

There isn’t any assure that the corporate will retain its means to faucet capital markets affordably or get its manufacturing capabilities up and operating rapidly. It must market its autos in a hypercompetitive trade. But it’s this uncertainty that gives affected person traders with a profitable entry level for Rivian inventory proper now. When you can stay affected person, Rivian’s rise might ultimately mirror Tesla’s.

Must you make investments $1,000 in Rivian Automotive proper now?

Before you purchase inventory in Rivian Automotive, take into account this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the for traders to purchase now… and Rivian Automotive wasn’t certainly one of them. The ten shares that made the lower might produce monster returns within the coming years.

Think about when Nvidia made this record on April 15, 2005… if you happen to invested $1,000 on the time of our suggestion, you’d have $743,952!*

Inventory Advisor offers traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Tesla. The Motley Idiot has a .

was initially printed by The Motley Idiot

If You Purchased 1 Share of Nvidia at Its IPO, Right here's How Many Shares You Would Personal Now

Assume You Know Altria? Right here's 1 Little-Identified Reality You Can't Overlook.

The Final Electrical Car (EV) Inventory to Purchase With $1,000 Proper Now

UBS chair warns towards massive improve in capital necessities, newspaper studies

Meet the three Supercharged Development Shares That Will Be Price $4 Trillion by 2025, In accordance with 1 Wall Avenue Analyst

Tremendous Micro: Assessing the Potential Danger and Reward

Unique-TPG in lead to purchase stake in Inventive Planning at $15 billion valuation, sources say

Exxon director joins Elliott group searching for to accumulate Citgo Petroleum

Steward Well being CEO who refused to testify to US Senate will step down

Nvidia Inventory (NVDA) Is Nonetheless a Lengthy-Time period Winner, No Matter the Noise

35 Strangers Had been Fraudulently Added To Her Card Throughout A Cruise, However One U.S. Postal Service Was Key In Stopping A Doable Catastrophe

You Can Do Higher Than the S&P 500. Purchase This ETF As an alternative.

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoADP Stories Decrease-Than-Anticipated Personal Payroll Progress for June

-

Markets3 months ago

Markets3 months agoSorry, however retiring ‘comfortably’ on $100K is a fantasy for most individuals. Right here’s why.

-

Markets3 months ago

Markets3 months agoSouthwest Air adopts 'poison tablet' as activist investor Elliott takes important stake in firm

-

Markets3 months ago

Markets3 months agoAbove Food Corp. (NASDAQ: ABVE) and Chewy Inc. (NYSE: CHWY) Making Headlines This Week

-

Markets3 months ago

Markets3 months agoCore Scientific so as to add 15 EH/s by means of Block’s 3nm Bitcoin mining ASICs

-

Markets3 months ago

Markets3 months agoWarren Buffett is popping 94 subsequent month. Ought to Berkshire traders begin to fear?

-

Markets3 months ago

Markets3 months agoWhy Rivian Inventory Roared Forward 10% on Friday

-

Markets3 months ago

Markets3 months agoArgentina to Promote {Dollars} In Parallel FX Market, Caputo Says

-

Markets3 months ago

Markets3 months agoWhy Intel Inventory Popped on Friday

-

Markets3 months ago

Markets3 months agoMicrosoft in $22 million deal to settle cloud grievance, keep off regulators

-

Markets3 months ago

Markets3 months agoMorgan Stanley raises worth targets on score companies on constructive outlook