Markets

Tesla Inventory’s (NASDAQ:TSLA) Comeback: What the Newest Q2 Knowledge Means for Buyers

Tesla’s (NASDAQ:TSLA) journey in 2024 has been something however clean. We’ve acquired manufacturing unit shutdowns, transport woes, and a few severe competitors nipping at Tesla’s heels, particularly in China. But, Elon Musk’s unwavering dedication to increasing Tesla’s EV lineup has saved the corporate on monitor. The current launch of Tesla’s Q2 manufacturing and supply report has everybody speaking. Whereas the numbers present a decline in comparison with final 12 months, they nonetheless managed to beat analysts’ expectations, giving the inventory a much-needed enhance.

Personally, I’m bullish on Tesla inventory. Whereas the corporate faces vital challenges, its capacity to beat supply expectations in a troublesome atmosphere, coupled with its robust model and management in EV know-how, suggests potential for continued progress.

Q2 Supply and Manufacturing Highlights

Tesla managed to provide round 411,000 automobiles within the second quarter, which is spectacular contemplating the challenges the agency has confronted lately. Tesla delivered extra automobiles than it produced, with roughly 444,000 automobiles going to prospects’ driveways. This marks a 4.8% year-over-year decline in deliveries and a 14% drop in manufacturing in comparison with the identical interval in 2023.

As anticipated, the Mannequin 3 and Mannequin Y had been the celebrities of the present, accounting for the lion’s share of manufacturing at 386,576 items and deliveries at 422,405 items. The Mannequin S, Mannequin X, and the much-hyped Cybertruck made up the remaining, with 24,255 items produced and 21,551 items delivered.

Analysts had anticipated Tesla to ship round 439,302 automobiles, so the corporate’s efficiency was a welcome shock. This information despatched Tesla’s inventory hovering 10% to $231.26 regardless of being down about 7% for the 12 months.

In simply three buying and selling days, from July 1st to July third, by a jaw-dropping 23%. That’s proper, practically 1 / 4 of the corporate’s worth was added in simply 72 hours, and the inventory has gone up a bit extra previously few days.

What’s much more spectacular is that this surge has fully erased Tesla’s year-to-date losses. The inventory is now up 1.8% for the 12 months, a far cry from the place it was simply two weeks in the past.

Nonetheless, it’s essential to notice that even with this current dip, Tesla remains to be buying and selling at a major premium in comparison with different automakers. Its P/E ratio of 64.3x is miles above the likes of Normal Motors (NYSE:GM) (5.7x) and Ford (NYSE:F) (13.3x), indicating that a whole lot of progress is already baked into the inventory worth. The approaching quarters can be essential in figuring out whether or not Tesla can preserve this momentum and justify its lofty valuation.

Tesla’s Challenges and Strategic Responses

Tesla is feeling the warmth from competitors, particularly in China. BYD (OTC:BYDDF), their largest rival, offered round 426,000 pure electrical automobiles in Q2, which is simply shy of Tesla’s 443,956 deliveries—a niche of solely 17,956 items. And it’s not simply BYD; different Chinese language automakers like Geely (OTC:GELYF) are additionally stepping up their sport, with Geely’s gross sales leaping 41% within the first half of 2024.

In response, Tesla has been aggressively slicing costs since early 2023, which has helped preserve gross sales quantity but additionally squeezed revenue margins. Its Automotive gross margin dropped to 18.5% in Q1 2024 from 21.1% in Q1 2023. Tesla additionally confronted vital challenges earlier this 12 months, together with an arson assault at their German manufacturing unit and transport disruptions as a result of Purple Sea riot, contributing to a 14% year-over-year decline in Q2 manufacturing.

Regardless of these hurdles, Tesla isn’t simply taking part in protection. Elon Musk has plans to speed up the mass manufacturing of inexpensive EVs, probably launching within the first half of 2025. This could possibly be a game-changer for reaching a broader market. Moreover, Tesla’s power storage enterprise is flourishing, with Q1 income hitting a document $1.64 billion and power deployments reaching 4.1 GWh.

Tesla can be closely investing in AI and robotics, practically doubling their AI coaching capability. Musk is so assured of their Optimus humanoid robots that he thinks they might enhance Tesla’s market worth to $25 trillion (its market cap is at the moment round $800 billion).

What’s Subsequent for Tesla and Its Buyers?

A couple of key occasions are arising that would considerably influence Tesla’s future. First, the Q2 earnings report on July twenty third will give us an in depth take a look at their monetary efficiency. Analysts count on income to succeed in $23.83 billion. In addition they (EPS) of $0.60, with a variety of $0.41 to $0.87. This represents a major enchancment from the earlier quarter’s EPS of $0.45. If Tesla’s income progress turns optimistic in Q3, it will mark a serious restoration milestone.

Then there’s Robotaxi Day on August eighth, which could possibly be an enormous deal for Tesla’s autonomous driving ambitions. Nonetheless, analysts have combined views on Tesla’s inventory. Dan Ives from Wedbush is optimistic, elevating his worth goal to $300, believing the worst is behind Tesla and that upcoming improvements just like the Robotaxi might drive progress.

Alternatively, Colin Langan from Wells Fargo is cautious, recommending promoting Tesla shares attributable to issues about declining supply progress and the influence of worth cuts on margins. His worth goal is a conservative $120. Guggenheim analysts additionally raised their worth goal to $134 however , noting Tesla’s spectacular power storage deployments as a key issue.

Is Tesla Inventory a Purchase, Based on Analysts?

Based on the newest analyst scores, Tesla inventory has a consensus Maintain score. Out of 35 analysts masking the inventory, 13 charge it a Purchase, 14 a Maintain, and eight a Promote. The of $184.41 implies draw back potential of round 27.1% from the present worth.

The Backside Line

In conclusion, Tesla’s Q2 supply report was a combined bag. Whereas the corporate beat estimates, deliveries nonetheless dropped year-over-year. The market reacted positively, however analysts are divided on the inventory’s future. Some consider the worst is over for the corporate, whereas others stay cautious in regards to the aggressive pressures and potential margin squeezes.

Regardless of these challenges, I’m bullish on Tesla inventory. The corporate’s resilience, dedication to increasing its EV lineup, and thrilling potential in AI and power storage make it a compelling funding. The upcoming Q2 earnings report on July 23 and Robotaxi Day on August 8 might present extra readability and probably drive the inventory greater. As all the time, do your homework and make investments properly.

Markets

35 Strangers Had been Fraudulently Added To Her Card Throughout A Cruise, However One U.S. Postal Service Was Key In Stopping A Doable Catastrophe

In August, Jodi Hayes and her partner have been leisurely cruising when issues took an unanticipated and distressing flip. Whereas they have been nonetheless on board the ship, Jodi received an alert from the U.S. Postal Service’s Knowledgeable Supply program. The e-mail confirmed that 35 bank cards have been on their option to her dwelling – all within the names of individuals she had by no means heard of.

Do not Miss:

Every of those 35 strangers was added as a certified consumer to her Marriott Bonvoy Chase Financial institution bank card they usually might every cost as much as $19,000 on her card or withdraw $950 in money, doubtlessly leaving Jodi liable for an enormous debt.

“I do know I’ve , however I’ve by no means seen something like this ever,” Jodi stated, clearly annoyed. “This fiasco ruined the tip of our trip.”

Trending: Founding father of Private Capital and ex-CEO of PayPal

As ABC7 , she shortly known as Chase Financial institution whereas nonetheless on the cruise ship to report the problem. Nevertheless, their response left a lot to be desired. They initially brushed it off as a attainable and stated they’d cease the playing cards from being activated. They did not supply way more than a brand new card and account quantity with out rationalization or investigation.

When Jodi contacted ABC7, hoping to get extra solutions and assist, the state of affairs caught the eye of the U.S. Postal Inspection Service. Matthew Norfleet, a postal inspector, defined that this was doubtless an id fraud scheme. Utilizing the mail for such schemes is a severe crime that may carry as much as 20 years in jail.

Trending: Teenagers might by no means want knowledge tooth eliminated due to this MedTech Firm –

However, the deception didn’t finish with Chase. Jodi quickly obtained credit score functions from extra banks, together with Capital One, Uncover, and Citibank, all rejected due to . The repeated use of the identical fictitious names demonstrated these con artists’ persistence after they “odor” a possibility.

Jodi protected herself in lots of appropriate methods regardless of the hazard and absurdity of the state of affairs. She stored an eye fixed on her mail utilizing the USPS Knowledgeable Supply program and secured her mailbox with a lockbox to discourage burglars. To additional decrease the prospect of mail theft, the Postal Service even advises holding your mail on the submit workplace when you’re on the highway.

This example demonstrates how important it’s to observe your accounts and private knowledge. Whereas Jodi’s fast actions and using Knowledgeable Supply helped catch the issue earlier than it received worse, not everyone seems to be so fortunate. Identification theft can occur to anybody, however instruments like Knowledgeable Supply might help spot potential issues early.

Learn Subsequent:

UNLOCKED: 5 NEW TRADES EVERY WEEK. , plus limitless entry to cutting-edge instruments and techniques to achieve an edge within the markets.

Get the newest inventory evaluation from Benzinga?

This text initially appeared on

© 2024 Benzinga.com. Benzinga doesn’t present funding recommendation. All rights reserved.

There’s nothing incorrect with the S&P 500 (SNPINDEX: ^GSPC) .

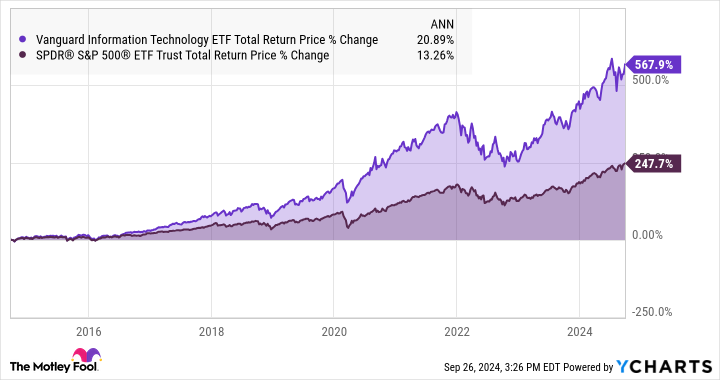

It displays the general well being of the American inventory market, with a top quality filter based mostly on market capitalization. Investing on this market tracker by exchange-traded funds (ETFs) just like the SPDR S&P 500 Belief (NYSEMKT: SPY) provides you a ton of diversification and units you up for sturdy long-term returns.

In the event you invested $1,000 within the SPDR fund 10 years in the past and set the place as much as in additional shares, you’d have $3,500 as we speak. That is a compound annual progress charge (CAGR) of 13.2%, leaving inflation charges far behind. Many traders get began in a well-liked SPDR 500 fund and let it run for many years, constructing wealth with zero investor effort.

However what if I instructed you that there are ETFs with even higher long-term returns? As an example, the Vanguard Info Expertise ETF (NYSEMKT: VGT) tends to beat the S&P 500’s returns within the lengthy haul. It is certainly one of my favourite ETFs. Let me present you the way it works.

Why this Vanguard fund is certainly one of my favourite ETFs for long-term progress

As you may see within the chart above, the Vanguard IT ETF has been crushing the S&P 500 and its index trackers during the last decade. The entire returns work out to a CAGR of 20.9%. Over this era, a hypothetical $1,000 funding would have grown to $6,678.

And that is only a easy one-time transfer with no additional money investments added over time. We could say an automatic dollar-cost averaging plan as an alternative, beginning with simply $100 within the fall of 2014 and including one other $100 to that Vanguard IT ETF place per thirty days. Some traders can do that as a paycheck deduction, others may arrange computerized transfers, and some could favor doing it by hand.

No matter methodology you utilize, these pretty painless contributions would add as much as $12,000 in a decade. The funding returns could be roughly $29,000, figuring out to a complete funding worth of $41,118.

Doing the identical factor with the SPDR S&P 500 fund as an alternative would have yielded respectable outcomes, too. The identical $12,000 funding needs to be price $25,174 by now, greater than doubling your cash in 10 years.

Like I mentioned, there’s nothing incorrect with that. Nonetheless, I would relatively have the stronger returns from the IT market tracker.

There is not any reward with out further dangers

After all, I can not promise market-stomping returns over each conceivable time interval. The fund underperformed the S&P 500 in its first 5 years available on the market, ending amid the subprime market meltdown of 2008-2009. The inflation disaster of 2022 was no enjoyable for Vanguard IT ETF traders, both.

In difficult markets like these hand-picked examples, the ETF’s give attention to high-growth funding concepts can lead to deeply detrimental returns. I needed to seek for these unfavorable examples, and this ETF tends to beat the S&P 500 over very long time intervals.

Nonetheless, this won’t be the fund for you if you cannot afford the occasional value drop alongside the way in which. The fund outperforms typically, however it may well actually harm when progress shares run right into a brick wall.

How this ETF’s portfolio differs from the S&P 500

The fund follows a market index reflecting all American shares within the data expertise sector, leading to an inventory of 317 names on the newest replace.

They’re weighted by market cap. Due to this fact, tech titans Apple (NASDAQ: AAPL), Microsoft (NASDAQ: MSFT), and Nvidia (NASDAQ: NVDA) are the three largest holdings lately. These three shares add as much as roughly 48% of the entire portfolio.

The identical three firms additionally dominate the S&P 500, however their mixed weight stops at simply 20% proper now. The IT index contains many shares which might be too small for the S&P 500.

So the IT-focused fund locations a heavier load on the most important firms, but in addition lets smaller companies contribute to the entire rating. It is a completely different balancing act that raises market dangers but in addition the potential returns.

Is the Vanguard Info Expertise ETF best for you?

You have seen the long-term returns, and I confirmed you the potential downsides. I do not thoughts in case you favor one thing just like the SPDR S&P 500 ETF in the long run. It should in all probability allow you to sleep higher at evening, not less than in difficult intervals just like the market crises I highlighted earlier.

I am simply blissful to have proven you a extra thrilling possibility. The Vanguard Info Expertise ETF is not each investor’s cup of tea, and that is OK. I extremely suggest taking a sip, although. These thrilling high-growth concepts could be intoxicating over the lengthy haul.

Do you have to make investments $1,000 in Vanguard World Fund – Vanguard Info Expertise ETF proper now?

Before you purchase inventory in Vanguard World Fund – Vanguard Info Expertise ETF, think about this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they imagine are the for traders to purchase now… and Vanguard World Fund – Vanguard Info Expertise ETF wasn’t certainly one of them. The ten shares that made the reduce might produce monster returns within the coming years.

Take into account when Nvidia made this record on April 15, 2005… in case you invested $1,000 on the time of our suggestion, you’d have $743,952!*

Inventory Advisor gives traders with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has positions in Nvidia and Vanguard World Fund-Vanguard Info Expertise ETF. The Motley Idiot has positions in and recommends Apple, Microsoft, and Nvidia. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and brief January 2026 $405 calls on Microsoft. The Motley Idiot has a .

was initially revealed by The Motley Idiot

Markets

Prediction: Apple's iPhone 16 Might Change into a Runaway Hit, and Right here Is 1 Inventory to Purchase Hand Over Fist Earlier than That Occurs

Preliminary stories that Apple‘s (NASDAQ: AAPL) newest batch of smartphones have been witnessing weaker demand than final yr’s fashions weighed on the inventory just lately. But it surely appears like these stories might not maintain a lot water in any case, as the corporate’s iPhone 16 lineup appears to be receiving a strong response from clients.

Extra importantly, a more in-depth take a look at the potential gross sales prospects of the most recent iPhone fashions signifies that Apple may witness a pleasant bump in gross sales going ahead.

A giant improve cycle may assist Apple promote extra iPhones

Counterpoint Analysis estimates that iPhone 16 fashions are witnessing sturdy demand in India, with gross sales reportedly leaping between 15% and 20% on the day the smartphones went on sale in that nation. It’s value noting that Apple’s gross sales in India surged a powerful 35% in fiscal 2024 (which resulted in March this yr), and the robust begin that the corporate’s newest gadgets are having fun with in that market means that the momentum is about to proceed.

In the meantime, T-Cellular CEO Mike Sievert additionally identified that the service is promoting extra iPhone 16 fashions this yr as in comparison with final yr. Although Sievert identified that the delayed rollout of Apple Intelligence may result in an extended shopping for cycle, it’s value noting that the iPhone maker may finally get pleasure from robust gross sales due to an growing old put in base of iPhones.

Dan Ives of Wedbush Securities estimates that out of an put in base of 1.5 billion iPhones, 300 million haven’t been upgraded in 4 years. So, with options set to make their option to the most recent Apple iPhones, there’s a good probability {that a} important chunk of those older iPhones could possibly be upgraded. Provided that Apple bought slightly below 235 million iPhones final yr, the stage appears set for an enormous soar within the firm’s shipments going ahead.

That is why buyers might need to purchase shares of Apple, contemplating that the tech big’s because of the arrival of its AI-enabled smartphones. Nonetheless, there’s one other inventory that is set to profit large time from the iPhone 16’s potential success, and buyers can purchase that firm at a less expensive valuation proper now — Taiwan Semiconductor Manufacturing (NYSE: TSM).

A shot within the arm for TSMC because of the brand new iPhones

Taiwan Semiconductor Manufacturing, popularly generally known as TSMC, is the corporate that manufactures the processors that energy Apple’s iPhones. The A18 and A18 Professional processors contained in the iPhone 16 fashions are manufactured utilizing TSMC’s 3-nanometer (nm) course of node.

Apple claims that its iPhone Professional fashions can ship 15% efficiency positive factors whereas consuming 20% much less energy than final yr’s fashions. In the meantime, the A18 chip discovered on the iPhone 16 and iPhone 16 Plus is reportedly 30% sooner and consumes 35% much less energy than final yr’s telephones. The improved processing energy and low consumption will play a key position in serving to the brand new iPhones run the Apple Intelligence suite of AI options and assist the corporate faucet a fast-growing area of interest.

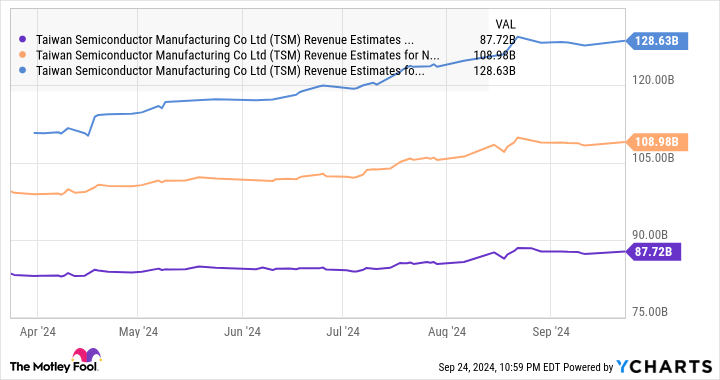

Apple reportedly started manufacturing its newest iPhones in June this yr and ramped up their manufacturing subsequently earlier than they hit the market this month. This is without doubt one of the explanation why TSMC has witnessed a big bump in its income of late. The Taiwan-based foundry big’s month-to-month income elevated 33% yr over yr in June, adopted by a forty five% enhance in July and a 33% enhance in August.

Apple is TSMC’s largest buyer and reportedly accounted for a fourth of the latter’s high line in 2023. So it’s simple to see why TSMC’s income has been rising at spectacular ranges of late. In fact, Nvidia is one other key TSMC buyer, because the semiconductor big has been tapping the latter’s foundries to fabricate its AI chips. Nonetheless, Nvidia reportedly accounted for 11% of TSMC’s income final yr, which implies that Apple strikes the needle in a extra important approach for the foundry big.

Ives expects the manufacturing of iPhone 16 fashions to hit 90 million items in 2024, up by 8 million to 10 million items from final yr’s fashions. This estimated enhance in manufacturing by Apple appears to be contributing to TSMC’s spectacular development in current months. Extra importantly, we noticed earlier that there’s a enormous put in base of customers that would transfer to Apple’s AI-enabled iPhones sooner or later. Consequently, TSMC’s largest buyer may proceed to play a central position in driving its development.

Even higher, stories counsel that Apple might have already bought all of TSMC’s manufacturing capability of 2-nm chips for its 2025 iPhone lineup. It’s value noting that Apple has performed an identical factor up to now when it bought all of TSMC’s 3nm manufacturing capability for a yr in 2023 in order that it may make sufficient iPhones.

In all, TSMC’s development prospects within the AI chip market because of clients equivalent to Nvidia, together with its tight relationship with Apple, are the explanation why there was a big enhance within the firm’s income estimates for the subsequent three years.

What’s extra, TSMC is buying and selling at 31 instances trailing earnings and 21 instances ahead earnings proper now. It’s cheaper than Apple, which is buying and selling at 34 instances trailing earnings and 30 instances ahead earnings. So, TSMC inventory offers buyers a less expensive and extra diversified option to capitalize on the potential development in iPhone gross sales, in addition to the secular development of the AI chip market.

That is why buyers ought to take into account shopping for this semiconductor inventory proper now earlier than it may fly larger following the 75% positive factors it has already clocked in 2024.

Do you have to make investments $1,000 in Taiwan Semiconductor Manufacturing proper now?

Before you purchase inventory in Taiwan Semiconductor Manufacturing, take into account this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they imagine are the for buyers to purchase now… and Taiwan Semiconductor Manufacturing wasn’t one in every of them. The ten shares that made the lower may produce monster returns within the coming years.

Take into account when Nvidia made this listing on April 15, 2005… when you invested $1,000 on the time of our suggestion, you’d have $743,952!*

Inventory Advisor offers buyers with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 23, 2024

has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Apple, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends T-Cellular US. The Motley Idiot has a .

was initially revealed by The Motley Idiot

35 Strangers Had been Fraudulently Added To Her Card Throughout A Cruise, However One U.S. Postal Service Was Key In Stopping A Doable Catastrophe

You Can Do Higher Than the S&P 500. Purchase This ETF As an alternative.

Prediction: Apple's iPhone 16 Might Change into a Runaway Hit, and Right here Is 1 Inventory to Purchase Hand Over Fist Earlier than That Occurs

Tips on how to put together your portfolio for This autumn

I’ve $2.5 million and nonetheless have an irrational worry that I’ll by no means be capable of retire

Thyssenkrupp metal head prepares workers for 'powerful' cuts

Medicare Benefit purchasing season arrives with a dose of confusion and a few political implications

UniCredit CEO Orcel attended digital assembly with Commerzbank, supply says

Home-rich shoppers are utilizing their properties to assist them get out of debt

In case your AI appears smarter, it's because of smarter human trainers

3 Monster Shares That Can Crush the S&P 500 Over the Subsequent 5 Years

On-line sellers on Walmart's Flipkart sue India watchdog over antitrust probe

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoADP Stories Decrease-Than-Anticipated Personal Payroll Progress for June

-

Markets3 months ago

Markets3 months agoSorry, however retiring ‘comfortably’ on $100K is a fantasy for most individuals. Right here’s why.

-

Markets3 months ago

Markets3 months agoAbove Food Corp. (NASDAQ: ABVE) and Chewy Inc. (NYSE: CHWY) Making Headlines This Week

-

Markets3 months ago

Markets3 months agoSouthwest Air adopts 'poison tablet' as activist investor Elliott takes important stake in firm

-

Markets3 months ago

Markets3 months agoCore Scientific so as to add 15 EH/s by means of Block’s 3nm Bitcoin mining ASICs

-

Markets3 months ago

Markets3 months agoWarren Buffett is popping 94 subsequent month. Ought to Berkshire traders begin to fear?

-

Markets3 months ago

Markets3 months agoWhy Rivian Inventory Roared Forward 10% on Friday

-

Markets3 months ago

Markets3 months agoArgentina to Promote {Dollars} In Parallel FX Market, Caputo Says

-

Markets3 months ago

Markets3 months agoWhy Intel Inventory Popped on Friday

-

Markets3 months ago

Markets3 months agoMicrosoft in $22 million deal to settle cloud grievance, keep off regulators

-

Markets3 months ago

Markets3 months agoMorgan Stanley raises worth targets on score companies on constructive outlook