Markets

There are 5 causes any dip in Nvidia inventory will likely be short-lived – and buyers ought to use a decline as a shopping for alternative

-

Nvidia inventory nonetheless gives a compelling valuation even after its 170% rally this 12 months, BofA says.

-

The financial institution highlighted Nvidia’s software program choices as a catalyst that would drive the subsequent leg of progress.

-

There are 5 causes buyers ought to view any decline in Nvidia inventory as a shopping for alternative.

has soared 170% year-to-date to , however the inventory nonetheless represents a pretty funding alternative — and any decline within the inventory ought to be used as a possibility to purchase extra.

That is in line with analyst Vivek Arya, who outlined in a observe on Wednesday a handful of causes buyers ought to stay bullish on the chip maker that is powering the synthetic intelligence growth.

“Nvidia inventory’s steep climb, up 50% simply in CQ2 (vs. SPX up 4.4%) might make it susceptible to near-term revenue taking,” Arya mentioned. “However we argue any volatility more likely to be short-lived.”

These are the 5 causes Arya is staying bullish on the inventory.

-

“GenAI {hardware} deployments are nonetheless solely in Yr 2 of what might be a 3-5yr deployment cycle,” Arya mentioned, including that the corporate has a $300 billion alternative to capitalize on, which is about thrice the dimensions of Nvidia’s anticipated income this 12 months.

-

“Advantages of NVDA’s next-gen purpose-built Blackwell AI accelerator programs will begin later this 12 months, with stable demand/visibility throughout cloud clients,” Arya mentioned.

-

“On-premise enterprise/sovereign AI demand plus software program monetization in early levels,” Arya mentioned.

“We imagine recurring software program companies might open the subsequent leg of progress, whereas strengthening its direct relationship over enterprise customers,” Arya mentioned.

Nvidia’s potential to construct a big recurring income stream from its CUDA software program providing is what drove Rosenblatt to boost its

-

“Valuation compelling at 35-40x consensus and solely ~30x PE on bull-case $5/sh earnings situation,” Arya mentioned, including that the inventory is buying and selling at a less expensive valuation at the moment than it was final 12 months.

-

“Not like the ‘dot-com growth’ that was funded by dangerous debt-taking, genAI deployment is a mission-critical race between among the best-funded (cloud) clients,” Arya mentioned.

Arya reiterated his “Purchase” score on Nvidia inventory and $150 worth goal, representing upside of 12% from present ranges.

Learn the unique article on

Lusso’s Information – European inventory markets edged decrease Friday, consolidating after the earlier session’s sharp good points as buyers digested a collection of coverage selections from the world’s main central banks.

At 03:05 ET (07:05 GMT), the in Germany traded 0.6% decrease, the in France fell 0.3% and the within the U.Ok. dropped 0.5%.

Central banks in focus

The principle European indices are on the right track for sturdy weekly good points within the wake of the slicing rates of interest by a hefty 50 foundation factors on Wednesday, beginning a rate-cut cycle to shore up the economic system following a chronic battle in opposition to surging inflation.

The and Norway’s each held charges regular on Thursday, whereas on Friday the left rates of interest unchanged as broadly anticipated, and stated that it continued to count on outsized development within the Japanese economic system amid a gentle uptick in inflation.

The Folks’s additionally stored its benchmark lending price unchanged on Friday regardless of growing requires extra stimulus.

German producer costs fall in August

The minimize its key rates of interest by 25 foundation factors after the same transfer in June, and will speed up these cuts over coming months, governing council member Fabio Panetta stated on Thursday, following the hefty Fed minimize and a sluggish eurozone economic system.

Knowledge launched earlier Friday confirmed that fell 0.8% on the 12 months in August, illustrating that inflation is retreating within the eurozone.

Elsewhere, British rose by a stronger-than-expected 1% in August and development in July was revised up, official figures confirmed on Friday.

Crude on monitor for sturdy weekly good points

Crude costs slipped decrease Friday, however had been on monitor for a second consecutive increased week after the big minimize in US rates of interest helped quell some fears of slowing demand.

By 03:05 ET, the contract dropped 0.2% to $74.77 per barrel, whereas futures (WTI) traded 0.1% decrease at $71.08 per barrel.

The benchmarks have been recovering after they fell to close three year-lows on Sept. 10, and have registered good points in 5 of the seven classes since then, together with good points of over 4% this week.

Crude inventories within the U.S., the world’s prime producer, fell to a one-year low final week, in accordance with official authorities knowledge earlier this week, however larger good points had been held again by persistent issues over slowing demand, particularly in prime importer China.

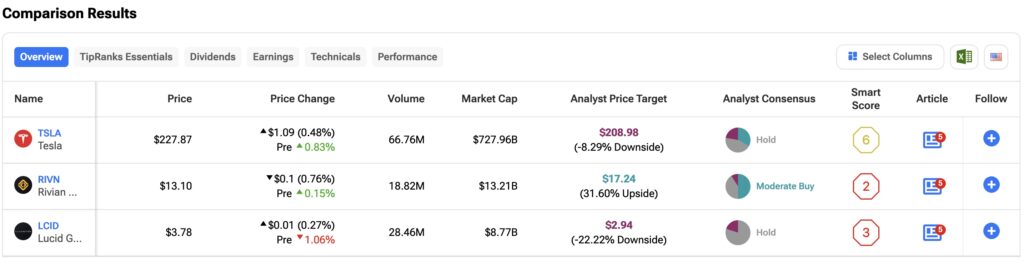

Within the extremely aggressive electrical car (EV) market, main gamers equivalent to Tesla , Rivian Automotive , and Lucid Group have encountered vital headwinds, with demand not assembly expectations. On this article, I’ll use the to clarify why I’m bullish on TSLA and RIVN, and bearish on LCID. I’ll additionally define why I take into account Tesla to be your best option among the many three automakers.

Regardless of a stretched valuation, I’m bullish on Tesla. The corporate’s shares at present commerce at a ahead P/E ratio of 97 instances future earnings estimates, which is about 15% under its five-year common. That is largely resulting from a considerable decline of over 40% within the share worth because it peaked in 2021, pushed by weaker-than-expected EV demand and elevated competitors. Nonetheless, Tesla stays the top-selling EV maker globally.

Tesla had aimed for 50% progress in car gross sales and manufacturing this 12 months however as an alternative has seen its income decline. In Q2, complete automotive income was $19.8 billion, down 7% from a 12 months in the past. Tesla’s quarterly manufacturing and supply figures in July confirmed 443,956 car deliveries, which was about 5% decrease than the earlier 12 months.

On the optimistic facet, Q2 noticed sturdy operational efficiency, with money from operations up 18% 12 months over 12 months to $3.61 billion, and free money circulation of $1.34 billion. This marks a rebound from Q1 of this 12 months when money from operations fell 90% to $242 million, and free money circulation declined to unfavourable $2.5 billion.

Is TSLA A Purchase, Maintain or Promote?

My bullish stance on Tesla isn’t primarily based on current outcomes however reasonably on its formidable progress forecasts. Tesla’s future is more and more tied to synthetic intelligence (AI), Robotaxis, and robotics. The corporate is ready to unveil its extremely anticipated Robotaxi on October 10, which might function a serious catalyst for the inventory.

Whereas some traders might not view Tesla as a serious AI participant, its massive put in base and vital involvement in AI are noteworthy. Dan Ives, a tech analyst at Wedbush Securities, argues that Tesla is probably the most undervalued AI firm. He believes Tesla might grow to be a trillion-dollar concern because it stabilizes demand and improves its pricing mannequin.

At present, Wall Avenue’s consensus on TSLA inventory is that it’s a Maintain. That is primarily based on 12 Purchase, 16 Maintain and eight Promote suggestions made within the final three months. of $208.98 implies potential draw back danger of 8.10%.

Rivian Automotive

Like Tesla, I’m additionally bullish on Rivian Automotive. That is primarily due to the corporate’s potential undervaluation vis-à-vis its formidable manufacturing targets. After dropping almost 90% of its worth since its 2021 preliminary public providing (IPO), Rivian now trades at a pretty worth primarily based on its money place.

With a market capitalization of $13.04 billion and $7.9 billion in money and short-term investments, greater than half of Rivian’s market worth is tied to its stability sheet. Nonetheless, primarily based on its electrical car gross sales, Rivian trades at a P/S ratio of two.5 instances, which, whereas decrease than Tesla, stays nearly 3 instances above the common for the automotive business.

That mentioned, the primary problem dealing with Rivian is reaching profitability and rising the manufacturing of its electrical car fashions. The corporate goals to provide as much as 215,000 autos yearly by 2026, up from 57,232 autos produced in 2023.

Is RIVN Inventory a Purchase?

Whereas I’m bullish on Rivian, it’s necessary to level out the dangers with this inventory. Rivian’s unprofitability is a priority. In Q2 of this 12 months, the corporate posted a internet lack of $1.45 billion, up from a $300 million loss a 12 months earlier. The corporate’s year-to-date loss now totals $2.9 billion. Nonetheless, as Wedbush analyst Dan Ives notes, Rivian’s main concern is its quarterly money burn of $800 million to $1 billion. This stays a priority as the corporate requires capital to scale manufacturing and meet demand. Extra not too long ago, a has eased dilution fears.

Wall Avenue is usually optimistic on RIVN, with 22 analysts score the inventory a Reasonable Purchase. That is primarily based on 11 Purchase, 9 Maintain and two Promote suggestions made up to now three months. The suggests 31.10% upside potential.

Relating to luxurious electrical car producer Lucid, I maintain a bearish place. That is due to the intense decline seen within the firm’s funds and market worth. The corporate’s market capitalization has declined to $8.34 billion from greater than $90 billion in 2021 when it went held its IPO. Regardless of the corporate’s decline, the valuation multiples nonetheless stay tough to justify.

Lucid trades at a 13 instances P/S ratio, almost double Tesla’s a number of and greater than six instances larger than Rivian’s. Moreover, the corporate reported a Q2 2024 internet lack of $643.3 million, translating to roughly $268,000 in losses per car bought, primarily based on the supply of two,394 autos through the quarter.

The state of affairs at Lucid could be extra dire if it weren’t for funding from Saudi Arabia’s Public Funding Fund (PIF). Due to that funding, Lucid holds $3.21 billion in money and short-term investments. This 12 months, the corporate raised a further $1 billion for the manufacturing of its new SUV referred to as “the Gravity.” Scheduled to launch in December this 12 months, the Gravity is predicted to be priced beneath $80,000, and will function a catalyst for LCID inventory.

Is LCID Inventory A Purchase, Maintain, or Promote?

My bearish view of Lucid is essentially resulting from its give attention to the slender and area of interest luxurious car market. Shoppers are clamoring for extra inexpensive EVs within the U.S. and elsewhere. Morgan Stanley analyst Adam Jonas my bearish outlook, noting Lucid’s issue in maintaining manufacturing prices under the promoting worth of its autos. This concern is additional exacerbated by the excessive value of its luxurious mannequin, the Lucid Air, which has a beginning worth of $69,900.

A complete of 10 Wall Avenue analysts have a consensus Maintain score on LCID inventory. That is primarily based on eight Maintain and two Promote suggestions made within the final three months. There aren’t any Purchase scores on the inventory. The implies draw back danger of 20.97% from the place the shares at present commerce.

Conclusion

I view Tesla as a high choose amongst this trio of main electrical car producers. The corporate has loads of progress potential with its Robotaxis, AI and robotics. Rivian Automotive can be a Purchase resulting from its upside potential and cheap valuation. I’m bearish on Lucid as a result of its valuation is simply too excessive and profitability stays a problem on the firm.

Lusso’s Information – Japan shares had been larger after the shut on Friday, as beneficial properties within the , and sectors led shares larger.

On the shut in Tokyo, the added 1.67%.

The perfect performers of the session on the had been Resonac Holdings Corp (TYO:), which rose 9.41% or 309.00 factors to commerce at 3,594.00 on the shut. In the meantime, Tokai Carbon Co., Ltd. (TYO:) added 7.02% or 61.10 factors to finish at 930.90 and Kawasaki Heavy Industries, Ltd. (TYO:) was up 6.26% or 319.00 factors to five,411.00 in late commerce.

The worst performers of the session had been Keisei Electrical Railway Co., Ltd. (TYO:), which fell 2.73% or 124.00 factors to commerce at 4,415.00 on the shut. NTT Knowledge Corp. (TYO:) declined 2.48% or 61.50 factors to finish at 2,418.50 and Kansai Electrical Energy Co Inc (TYO:) was down 2.37% or 57.00 factors to 2,349.00.

Rising shares outnumbered declining ones on the Tokyo Inventory Trade by 2389 to 1206 and 272 ended unchanged.

The , which measures the implied volatility of Nikkei 225 choices, was down 2.41% to 27.14.

Crude oil for November supply was down 0.10% or 0.07 to $71.09 a barrel. Elsewhere in commodities buying and selling, Brent oil for supply in November fell 0.13% or 0.10 to hit $74.78 a barrel, whereas the December Gold Futures contract rose 0.39% or 10.10 to commerce at $2,624.70 a troy ounce.

USD/JPY was down 0.50% to 141.91, whereas EUR/JPY fell 0.36% to 158.62.

The US Greenback Index Futures was down 0.17% at 100.15.

European shares consolidate after sharp good points; central banks in focus

TSLA, RIVN, or LCID: Which U.S. EV Inventory Is the Prime Choose?

Japan shares larger at shut of commerce; Nikkei 225 up 1.67%

Trump Media inventory drops as lockup expiration set to provide the previous president clearance to promote shares

Huawei's $2,800 cellphone launch disappoints amid provide considerations

Shares Lengthen Rally, Yen Positive factors as BOJ Holds Price: Markets Wrap

Nike's subsequent CEO Hill brings a bootstraps mentality

Traders must be hesitant to dive into shares after the speed reduce, with election uncertainty looming, Fundstrat's Tom Lee says

Nike veteran Hill to exchange Donahoe as CEO; shares soar

Why Intuitive Machines Inventory Rocketed 24% Skyward on Thursday

SpaceX 'forcefully rejects' FAA conclusion it violated launch necessities

Skechers Inventory Tumbles as CFO Offers Warning on China Outlook

Netflix (NFLX) Trading Back Above The 50 Day Moving Average

Exclusive: Is The Stock Market Going To Crash…Soon?

Ocugen (OCGN) Trades Over 700Million Shares , Finishes The Day +200%

3 Trading Tips That Have Changed Traders Lives

Sorrento Therapeutics (SRNE) Receives FDA Clearance

Consumer Price Index, Jobless Claims; What To Know For Tomorrow

These Stocks Under $3 Traded Massive Volume Today

Is NIO the Hottest Stock On Wall Street ?

Cathie Wood Buys More Shares of Palantir Technologies (PLTR)

Sundial Growers (SNDL) Trades Massive Volume, What You Should Know…

Is The Stock Market In A “Bubble” ?

This Stock Under $10 Has Wall Streets Full Attention

-

Markets3 months ago

Markets3 months agoInventory market in the present day: US futures slip as Micron slides, with information on deck

-

Markets3 months ago

Markets3 months agoFutures dip as Micron drags down chip shares forward of financial information

-

Markets3 months ago

Markets3 months agoApogee shares rise almost 4% on upbeat steering and earnings beat

-

Markets3 months ago

Markets3 months agoWhy Nvidia inventory is now in treacherous waters: Morning Transient

-

Markets3 months ago

Markets3 months agoWhy Is Micron Inventory Down After a Double Earnings Beat?

-

Markets3 months ago

Markets3 months agoHungary central financial institution tells lenders to reimburse purchasers after Apple glitch

-

Markets3 months ago

Markets3 months agoSoftBank to spend money on search startup Perplexity AI at $3 billion valuation, Bloomberg experiences

-

Markets3 months ago

Markets3 months agoInventory market at present: Asian shares decrease after Wall Avenue closes one other profitable week

-

Markets3 months ago

Markets3 months agoThe AI market alternative: UBS provides a bottom-up perspective

-

Markets3 months ago

Markets3 months agoNeglect Nvidia: Distinguished Billionaires Are Promoting It in Favor of These 7 High-Notch Shares

-

Markets3 months ago

Markets3 months ago3 No-Brainer Synthetic Intelligence (AI) Shares to Purchase With $500 Proper Now